Money Like Water

The power of herd psychology to compel conformity and capitulation is nearly irresistible, making it essential that investors resist them.

– Howard Marks, Co-Founder of Oaktree Capital Management

Q4, 2022 MARKET REVIEW

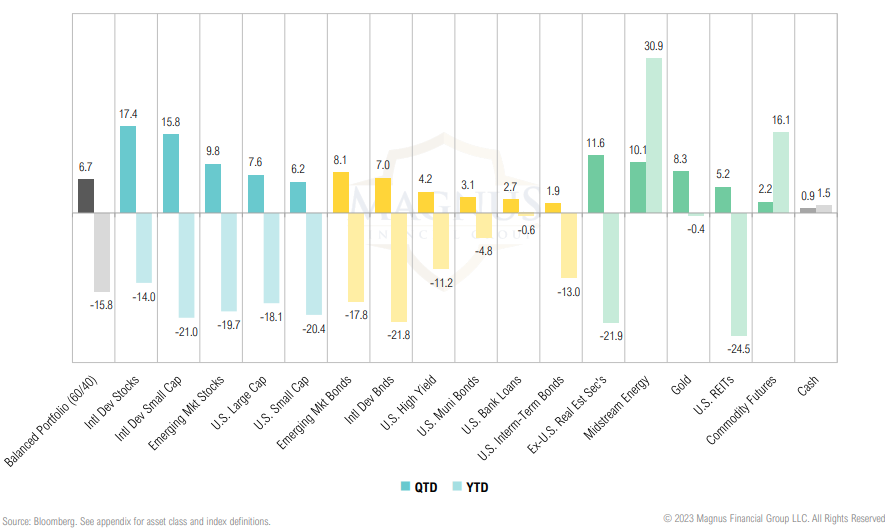

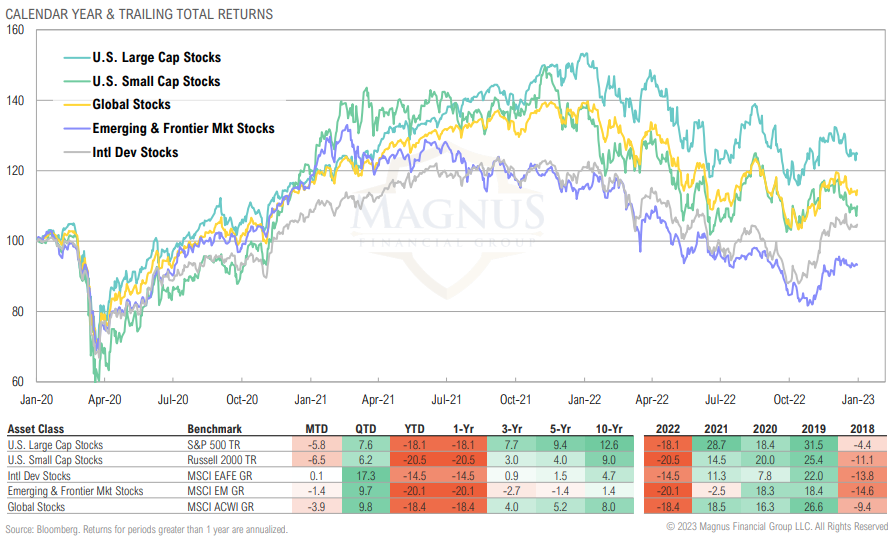

U.S. investors saw most investments rebound in the fourth quarter as both U.S. large cap stocks (+7.6%) and bonds (+1.9%) recovered together

Key themes for 2023

Era of tighter monetary policy – higher, but more volatile inflation underpinned by structurally constrained labor, housing and commodity markets; increased volatility due to stop-and-start policy. The economy and markets will be caught between a timid Fed fearful of a 1970s “Burns” error and fiscal stimulus that could goose growth.

Structurally lower real growth, with potential stagflation – inflation erodes real growth; high debt levels, poor demographics and sustained deficits will continue to impede growth in Europe, Japan. Based on the shape of the yield curve and recession models, a recession in 2023 is the base case, but the outlook could be better or worse.

Consumers spending themselves into a wall – real incomes lagging inflation; U.S. consumer is incrementally exhausting COVID stimulus, increasingly relying on credit to maintain spending; combined hit from slowing economy and rising interest rates spells trouble for 2023/2024.

Policy will be stop-and-start but mostly restrictive – mostly constrained but potentially also quite contradictory as rolling ad hoc fiscal (and monetary) bailouts frustrates attempts to rein in inflation.

Be patient, wait for pricing to improve or central banks to pivot – bear markets don’t usually bottom until equity valuations get cheap and/or central banks pivot (pause ≠ pivot); market has never bottomed ahead of official start of recession and recession unlikely to start until labor market cracks. This time may be different, but the macro backdrop is challenging enough to err on the side of caution.

Tilt to quality and cash flow – the lesson from prior bubble unwinds is patience. While we are excited about the potential opportunity set in equities, we don’t think we are there yet; prefer to “hide out” in areas with strong balance sheets and highest cash flow yields (quality, dividends).

Moving to neutral for U.S./non-U.S. – Foreign stocks have been a value trap for many years, but the valuation spread reached an actionable extreme last quarter; it is time to consider going to neutral, potentially overweighting.

Paid to wait – finally getting paid to wait; better yields on short-term invest. grade bonds reduces the risk of a wait-and-see approach to the rapidly evolving macro, policy and market backdrop, if paired with policy hedges.

Keep duration low – fighting the temptation to increase bond duration because of concerns around path of inflation, Fed’s resolve once labor market breaks or U.S. credit event but maintaining modest duration barbell and gold allocation as a hedge against a premature pivot.

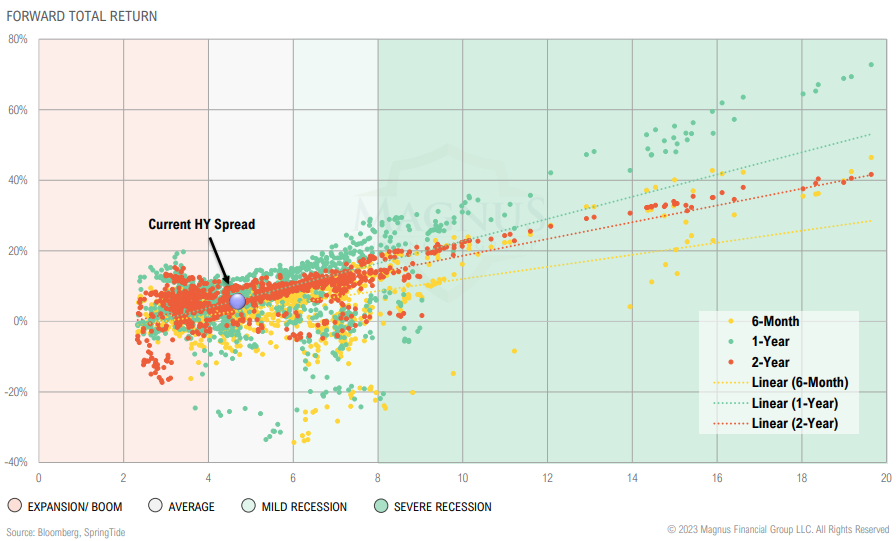

Budding opportunity in high yield bonds, other credit – high yield bonds near compelling level on an absolute & relative basis, except in the tails (right tail = early pivot, inflation; left tail = no pivot, severe recession).

Positive-carry policy hedge – midstream energy, gold miners and commodity futures now have positive carry and may provide a hedge if the Fed pivots early. Conversely, these hedges may underperform in a severe recession.

Opportunities emerging in real estate – maintain underweight (held since pandemic demand shock), waiting for dust to settle on higher rates, migration/ demographic, social and now recession-related disruption; expect to deploy in 2023/2024.

Volatility = opportunity – recession, if we enter one, usually see structural increases in vol; this = improved opportunity set for value-biased active managers, higher cost of capital rewards nimble fundamental managers.

Opportunity for dynamic asset allocation and active management – a period of stop-and-start growth, inflation, policy and trends in asset markets should benefit value-biased dynamic over static asset allocations.

GROWTH, INFLATION & POLICY

The timing of moderating rate increases is far less significant than the questions of how much further we will need to raise rates to control inflation, and the length of time it will be necessary to hold policy at a restrictive level. It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy.

– Jerome Powell, Federal Reserve Chairman

GDP & INFLATION

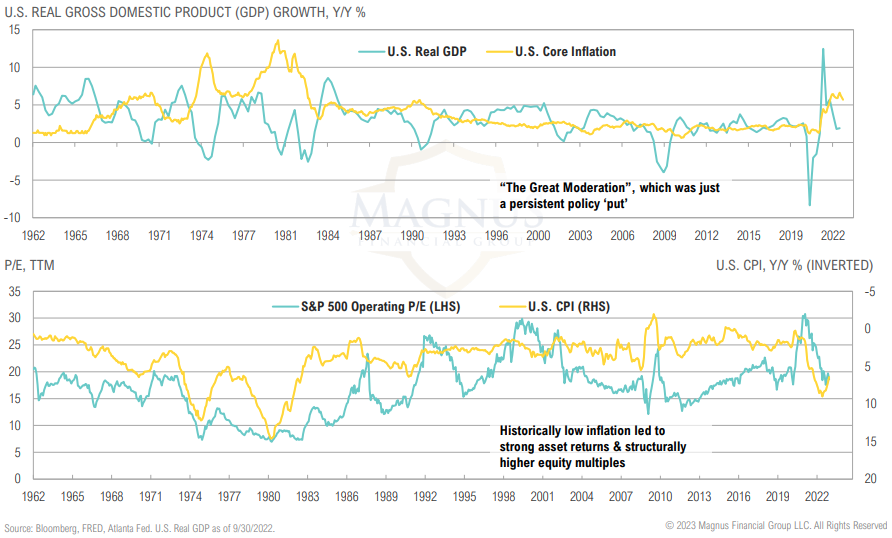

With the benefit of hindsight, the “Great Moderation” was just a persistent policy put resulting from historically low inflation

GDP

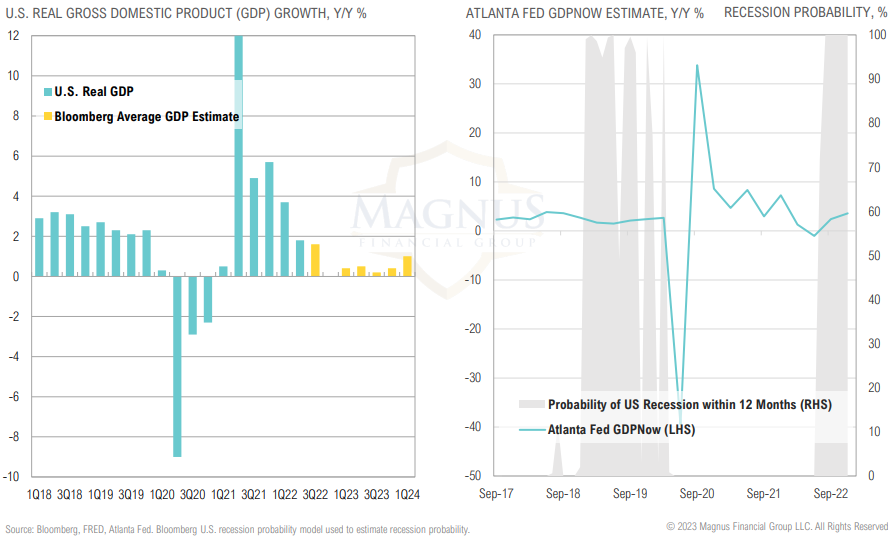

Most economic models suggest the potential for recession in next 12 months is high, arguably assured

MANUFACTURING & INVENTORIES

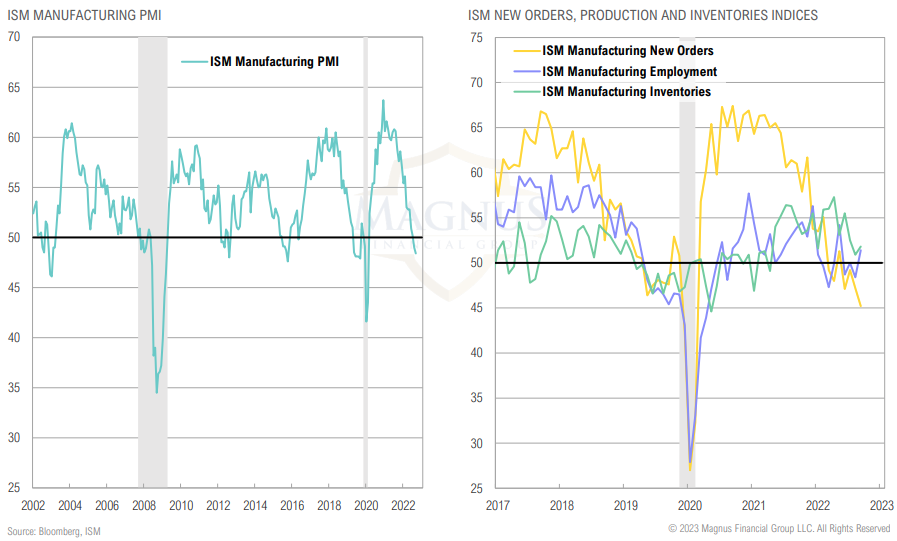

ISM Manufacturing PMI is in contraction; increases in inventories have slowed, while employment has been oscillating between contraction and expansion

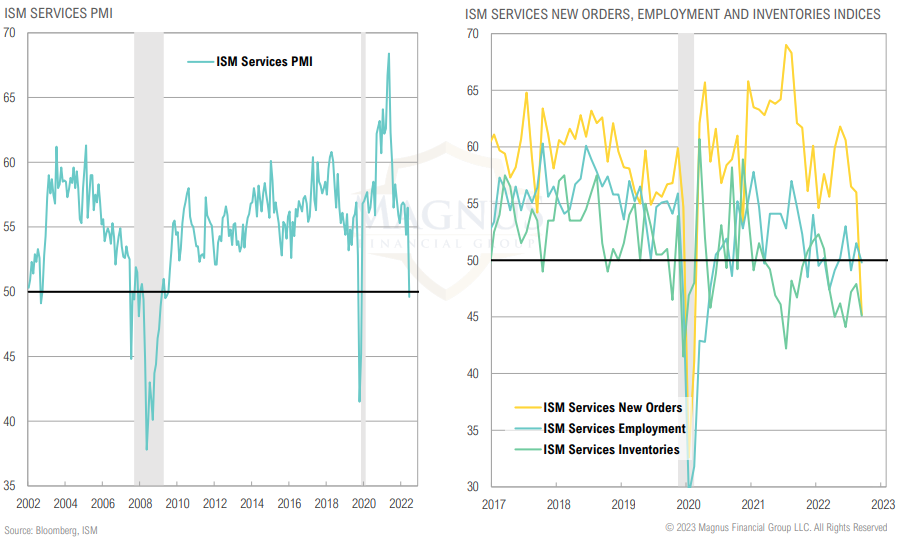

SERVICES & INVENTORIES

ISM Services now also in contraction but perhaps in healthier shape as consumer spending shifts from goods to services; services new orders have plummeted

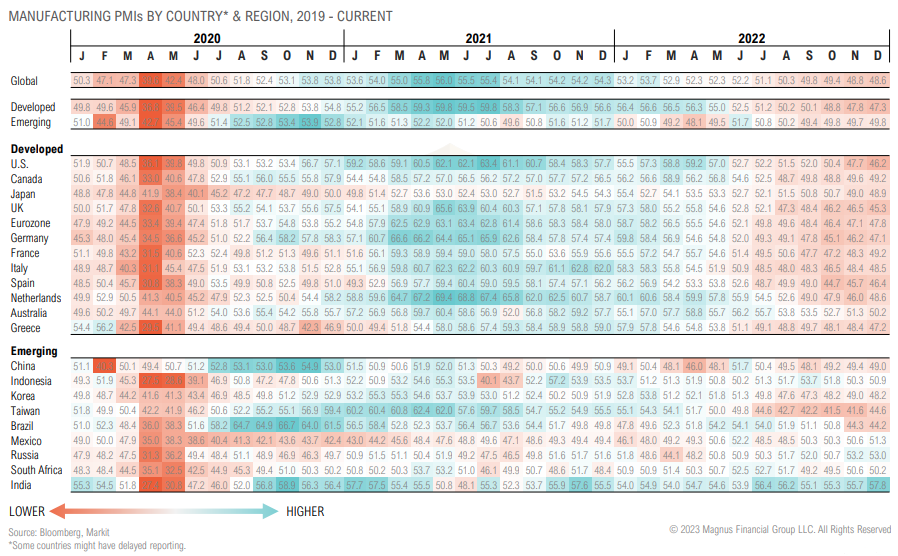

GLOBAL GROWTH

Global manufacturing activity slipped lower in December as developed market and emerging market activity continue to contract

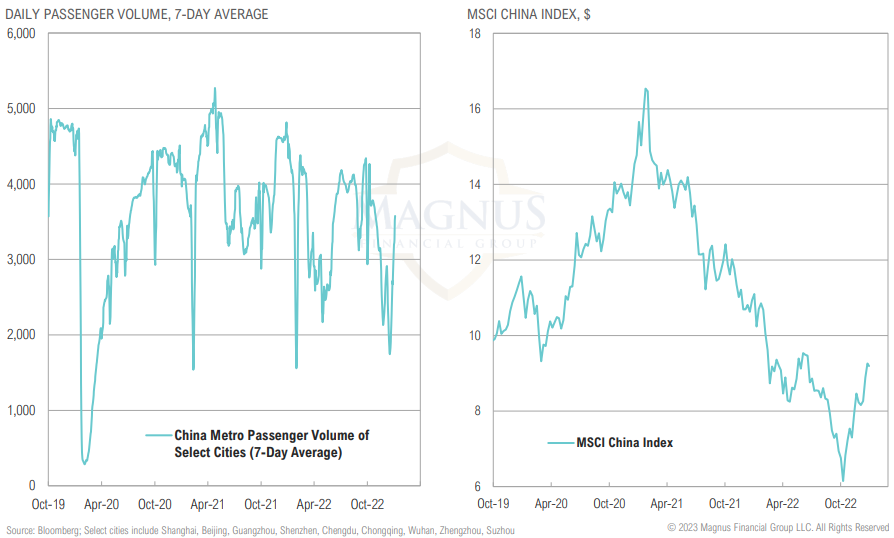

Following civilian protests, it appears mobility in China is increasing rapidly, potentially signaling an end to zero-COVID policy

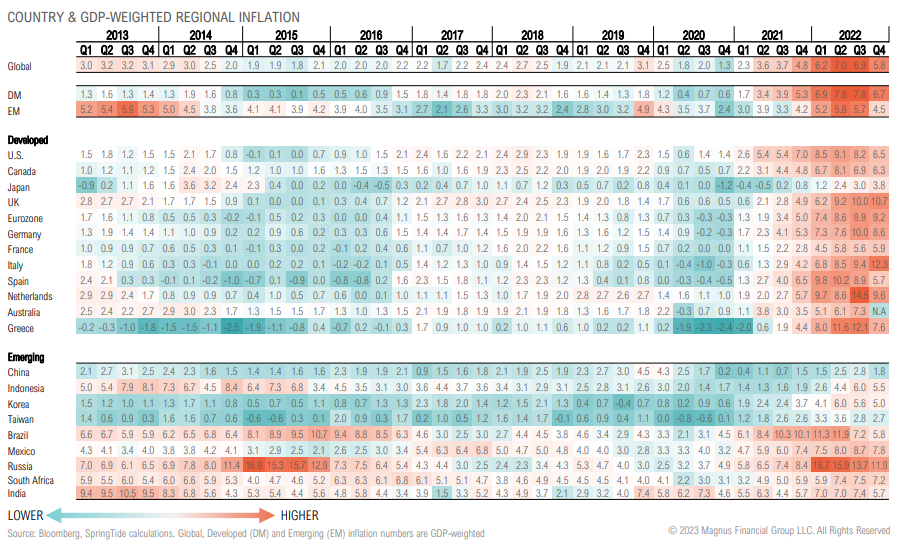

GLOBAL INFLATION

Pre-Russian invasion, global inflation was already at a decade high due to lack of investment in commodity supply, labor tightness, rising housing prices, supply chain bottlenecks, etc.

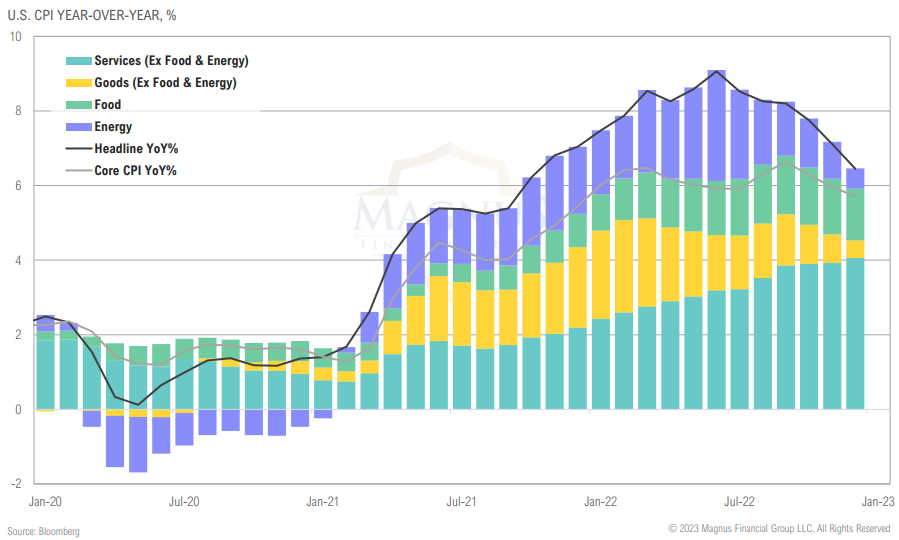

INFLATION

Headline inflation declines largely driven by lower energy and goods prices; core inflation proving more sticky, due to lags in shelter and persistent services inflation

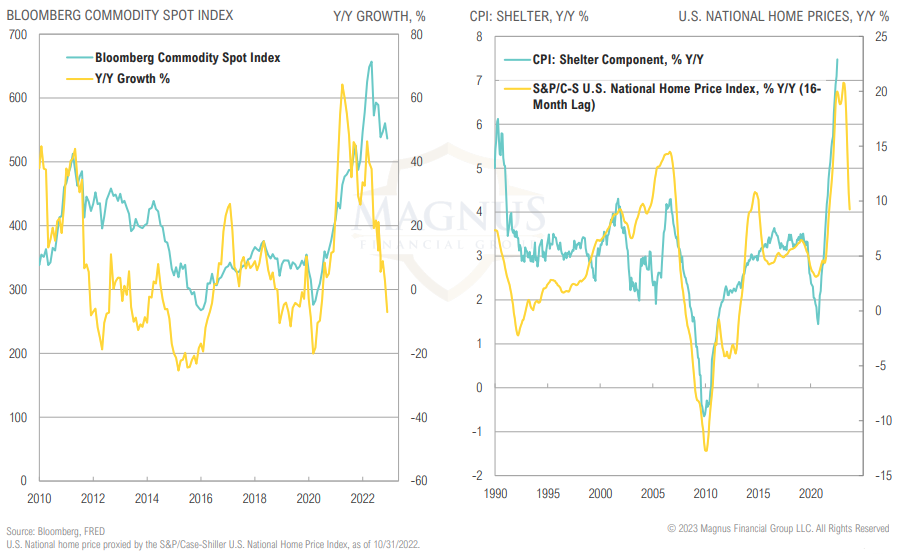

COMMODITIES & SHELTER

While commodity prices rolling over will help contain inflation, house prices impact the shelter component of CPI with a 12- to 18-month lag

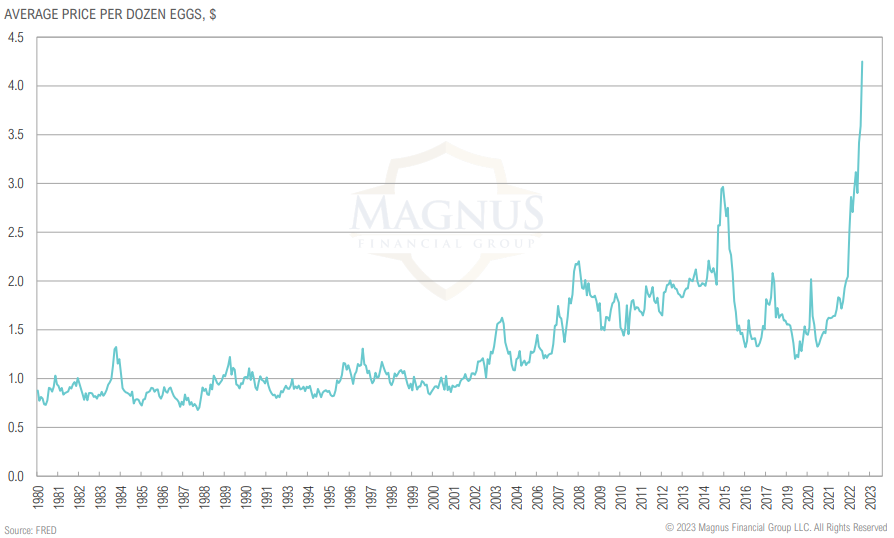

INFLATION

The price of a dozen eggs has more than doubled over the last year

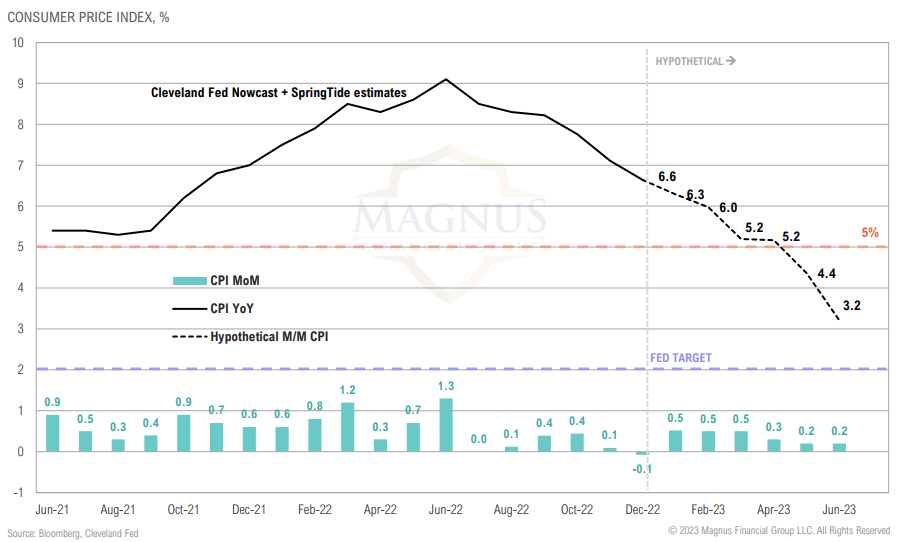

CPI

It is likely that YoY CPI will remain above 5% through Q1 of 2023

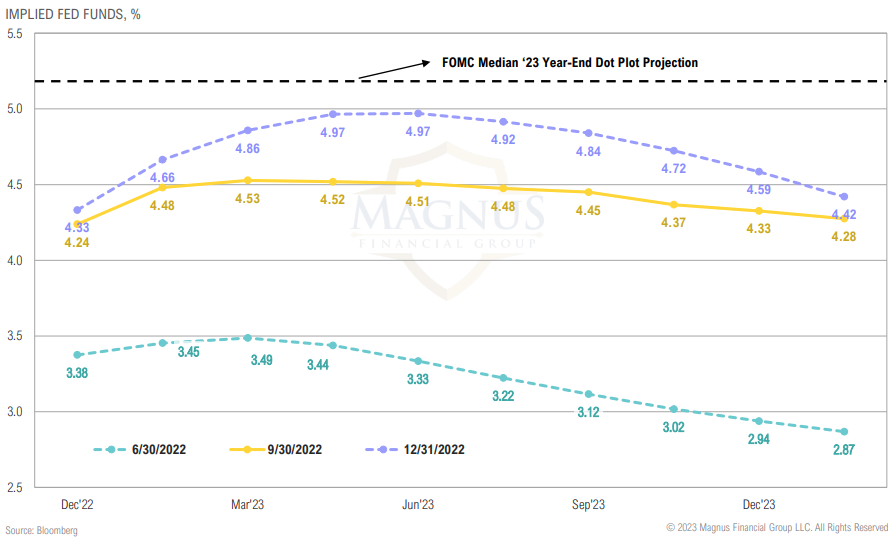

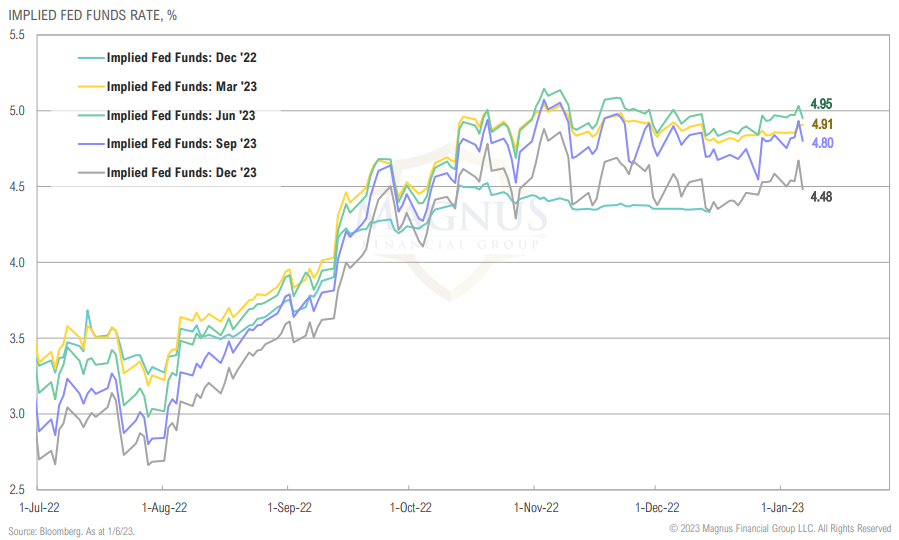

IMPLIED FED FUNDS

While the implied Fed funds rate has moved substantially higher over the year, the market still isn’t buying into the Fed’s “higher for longer” posturing

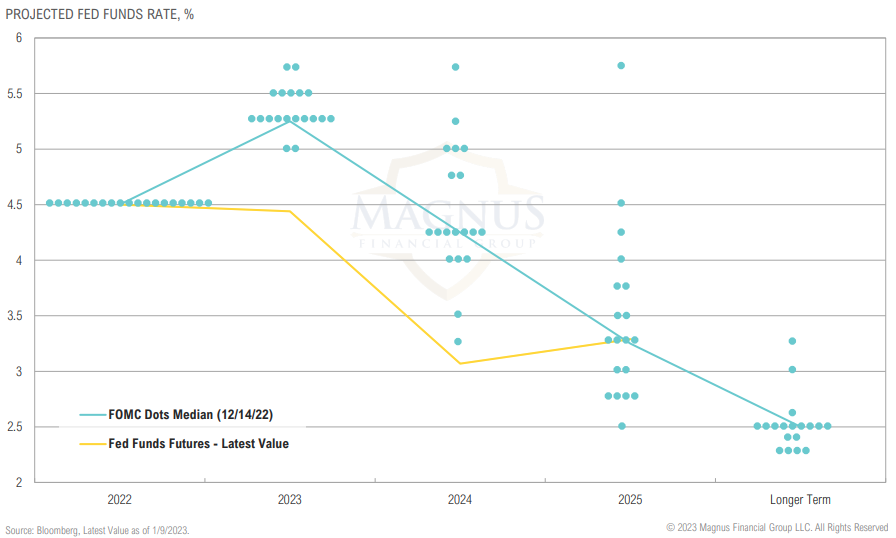

THE FED PIVOT

Market continues to price in a Fed pivot in 2023, despite the Fed signaling otherwise

RATE HIKE EXPECTATIONS

Fed funds futures expecting peak rates in June 2023 and the Fed to start cutting rates in the second half of the year; Fed and market have both been poor in projecting rates 12 months out

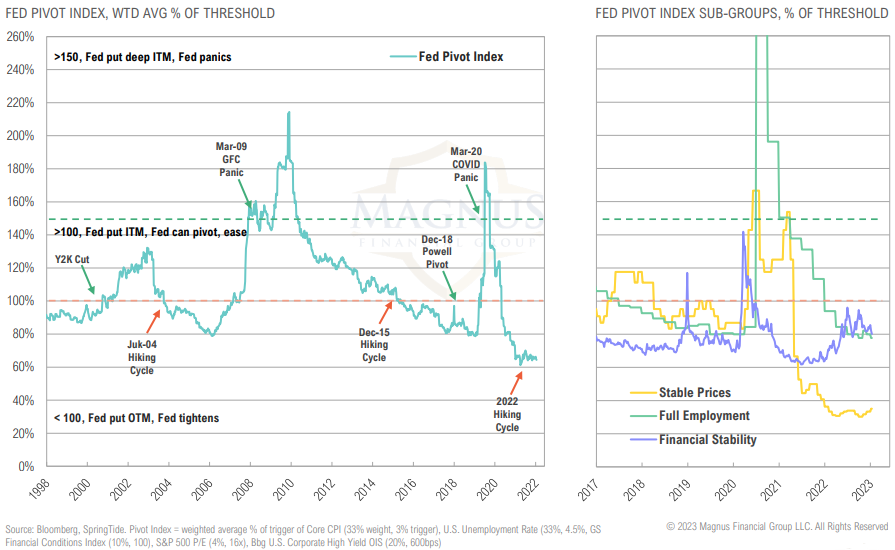

THE FED PIVOT INDEX

A Fed pivot at current levels isn’t justified by the data and would risk extending inflation shock and further eroding Fed’s credibility

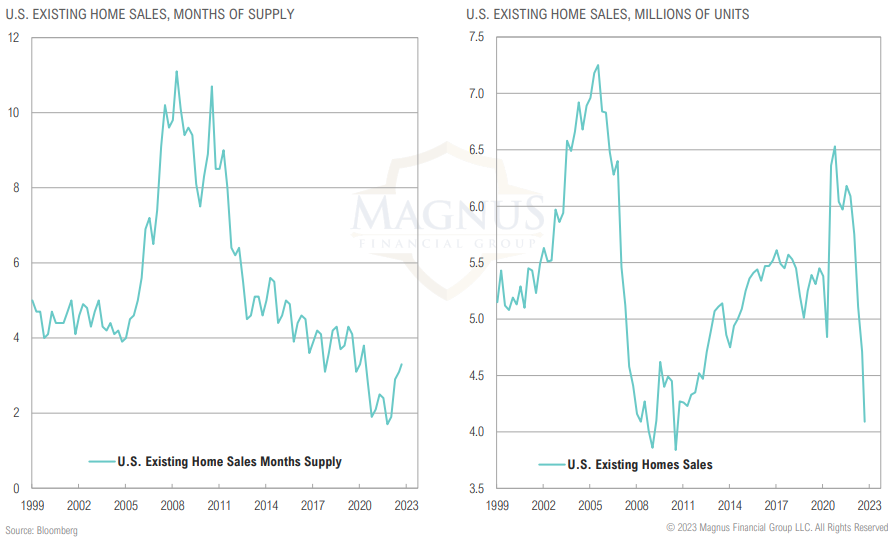

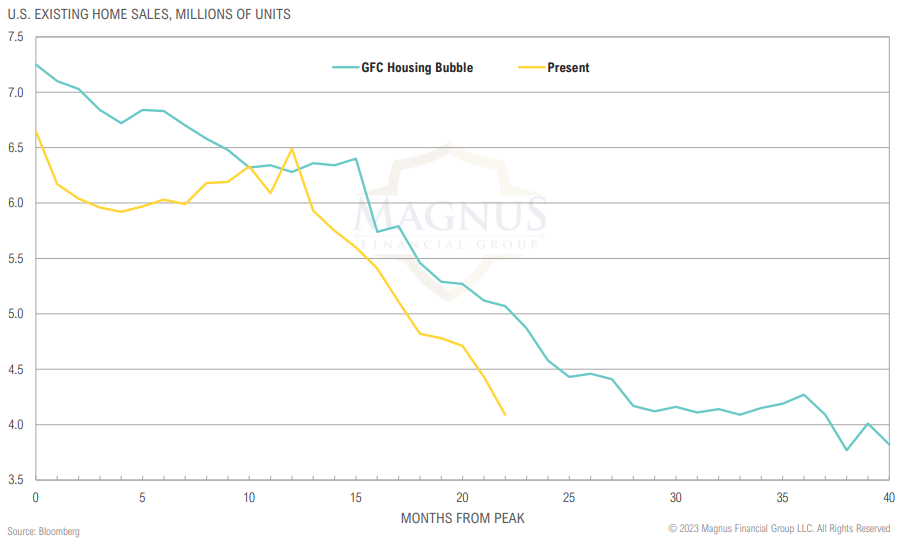

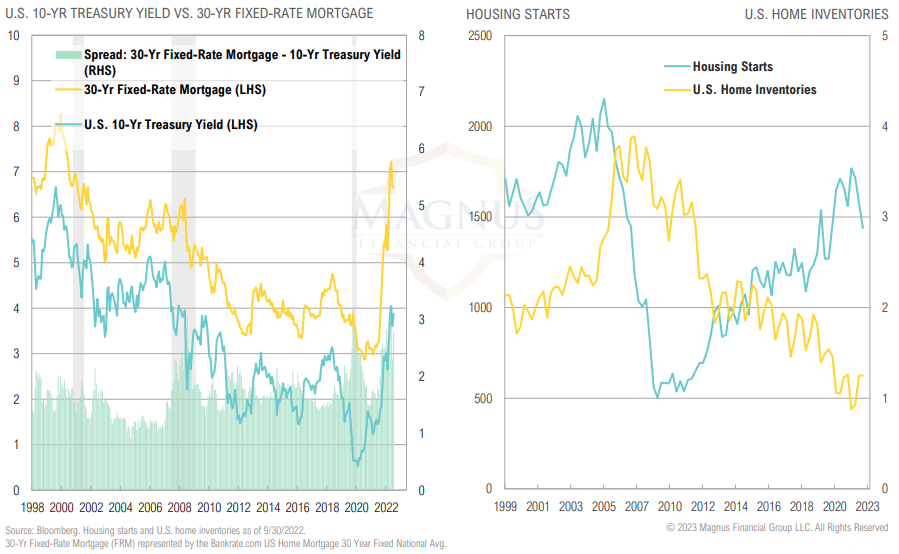

MORTGAGE RATES

Existing home sales have fallen by 2.5m over the past 22 months, which is a faster decline than during GFC; the difference between now and then is that supply of homes remains low

Existing home sales have fallen by 2.5m over the past 22 months, which is a faster decline than during GFC; the difference between now and then is that supply of homes remains low

30-year fixed mortgage rates were unchanged in December, resulting in tighter mortgage rate spreads vs. 10-year Treasuries; increased rates in ‘22 will have a negative impact on housing and consumers with a lag

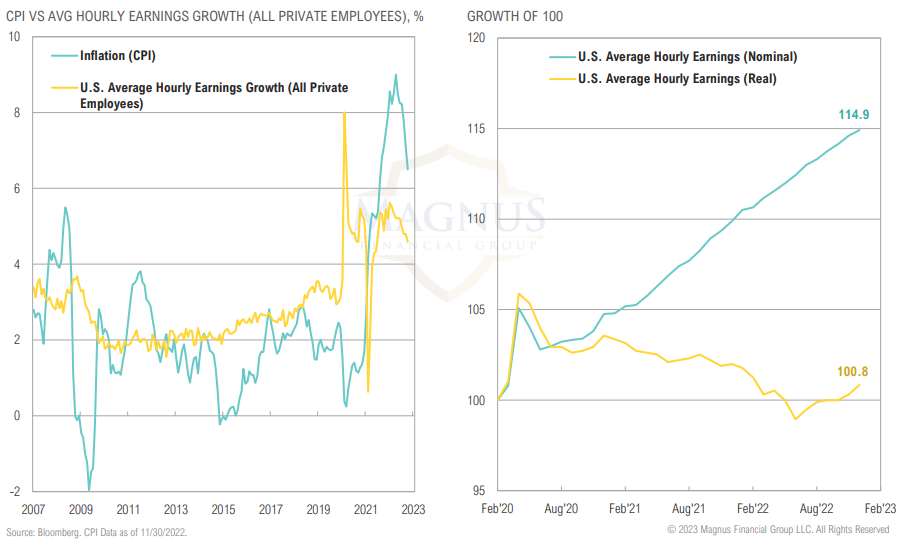

REAL EARNINGS

Since early 2021, inflation has outpaced wage growth, eroding real household disposable income

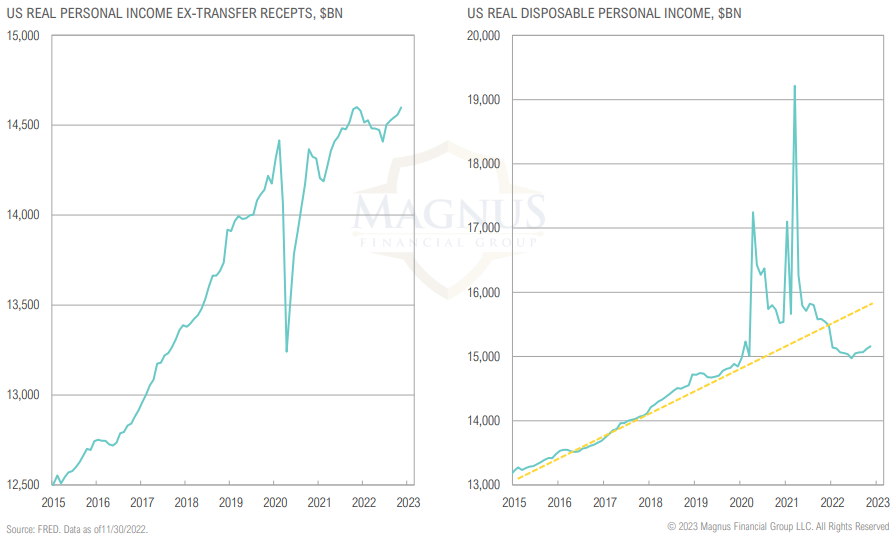

PERSONAL INCOME

Real income, excluding government transfers, is still grinding higher; total disposable income, however, has been treading water in recent months

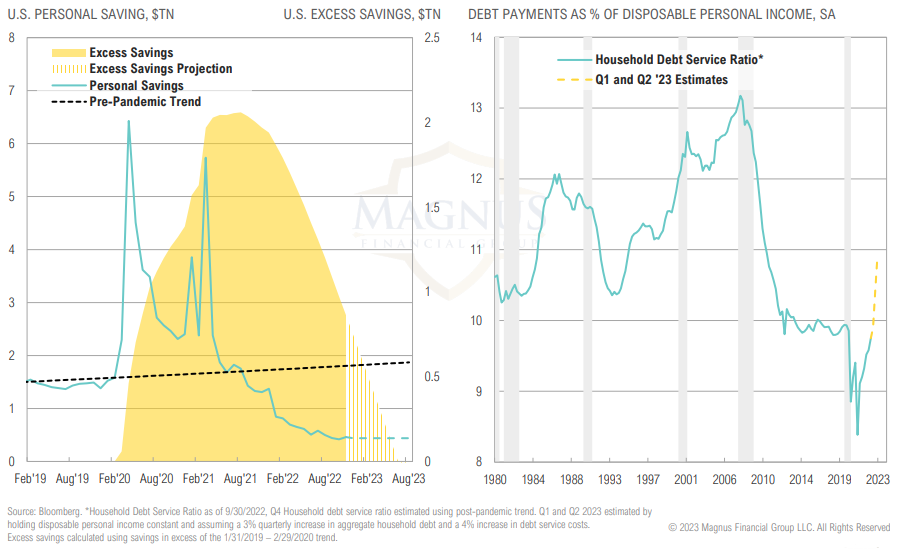

PERSONAL SAVINGS & DEBT PAYMENTS

Personal savings rates have plummeted to 2.4% vs 5-year pre-Covid average of 7.6%; if this savings rate continues, excess savings from Covid will be depleted by June ‘23

OPPORTUNISTIC

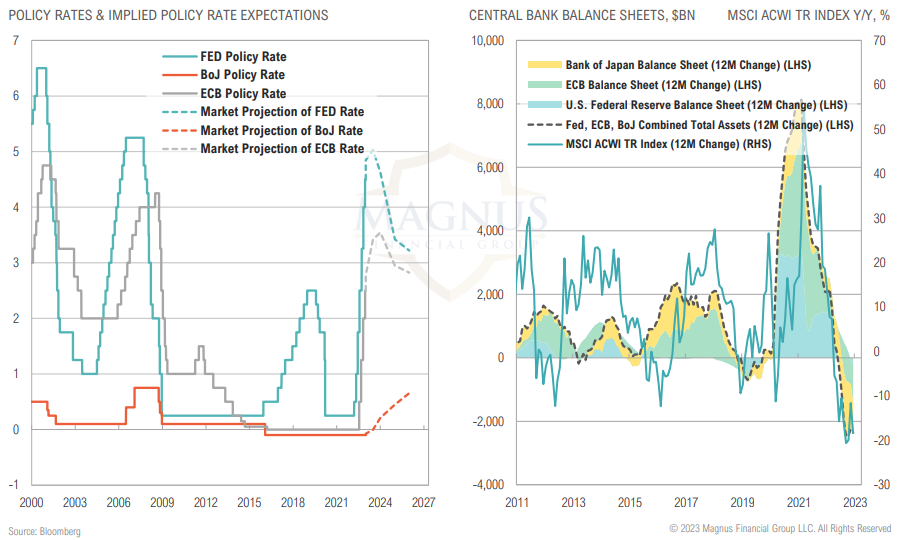

MONETARY POLICY & GLOBAL STOCKS

Global quantitative easing efforts supported the recent gains in global stocks; Fed, ECB and BoJ combined 12M change in assets have been negative since June ‘22

EQUITY

2021 was the most speculative year in markets I’d seen in 40 years. I dubbed it the “Dot Com era on steroids”. I never thought, after 2000, I would see investors do just completely insane things they were doing in 1999 and 2000 again. I was wrong and I was wrong in a big way.

I don’t think we appreciate in 2020 and 2021 the confluence of events that all came together in one witch’s brew of insanity. You had $5 trillion of fiscal stimulus, almost 25% of GDP, was literally pumped into economy in 12 months on top of the Federal Reserve’s zero interest rate policy and QE. So the most fiscal stimulus ever on top liberal monetary policy ever all coming together.

– Jim Chanos, Founder & President of Kynikos Associates

Excesses in one direction will lead to an opposite excess in the other direction.

– Bob Farrell, Merrill Lynch Strategist and Market Historian (Bob Farrell’s 10 Rules)

MARKET RETURNS SUMMARY

U.S. stocks underperformed their international peers over the fourth quarter, largely driven by a weaker dollar; DM stocks held up best over the year, driven by a mammoth Q4 rebound

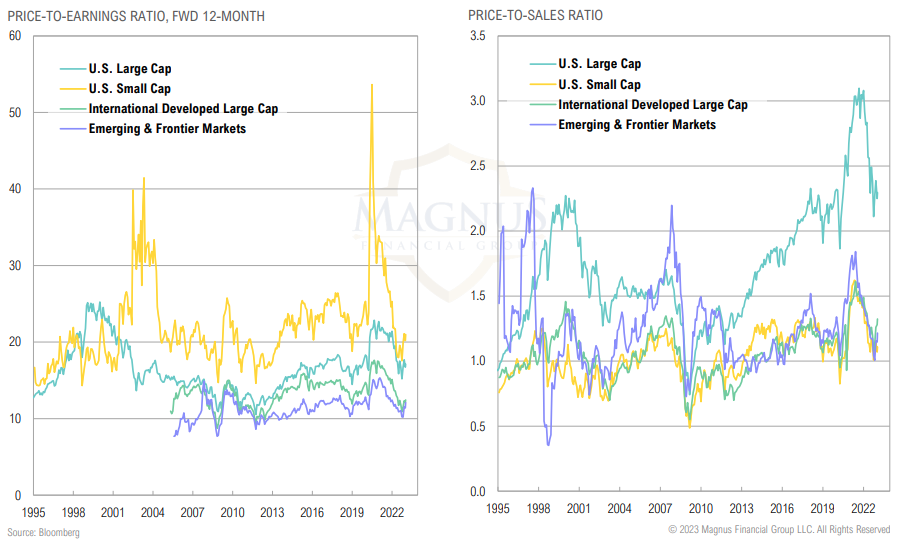

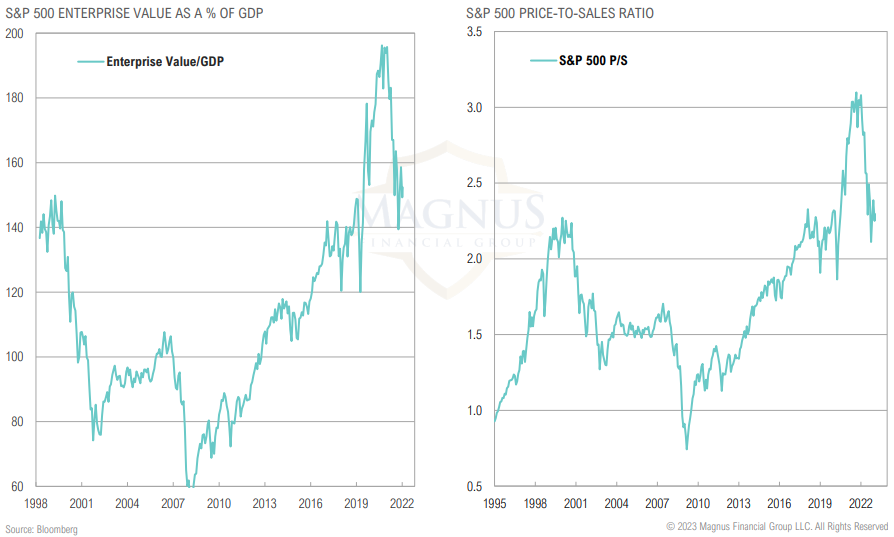

VALUATIONS

Valuations contracted over 2022 as stocks sold off globally

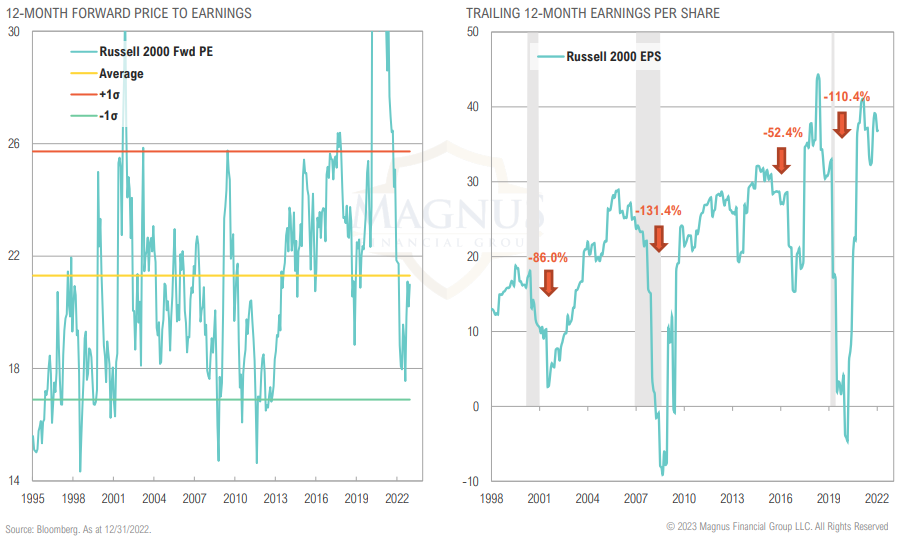

RUSSELL 2000 VALUATIONS

U.S. small cap forward valuations have improved due to bear market, slightly below average relative to history; focus now shifts to earnings decline

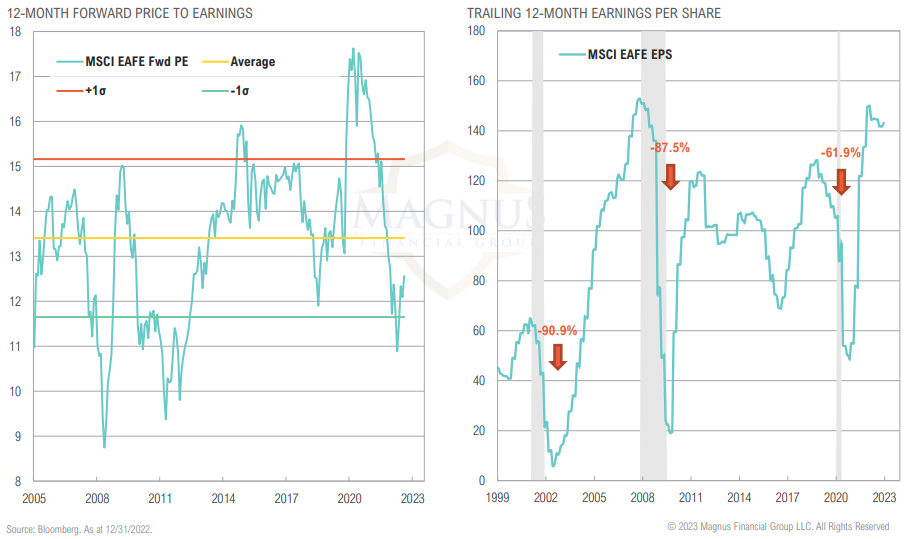

MSCI EAFE VALUATIONS

DM forward valuations have improved due to bear market, well below average relative to history; focus now shifts to earnings decline

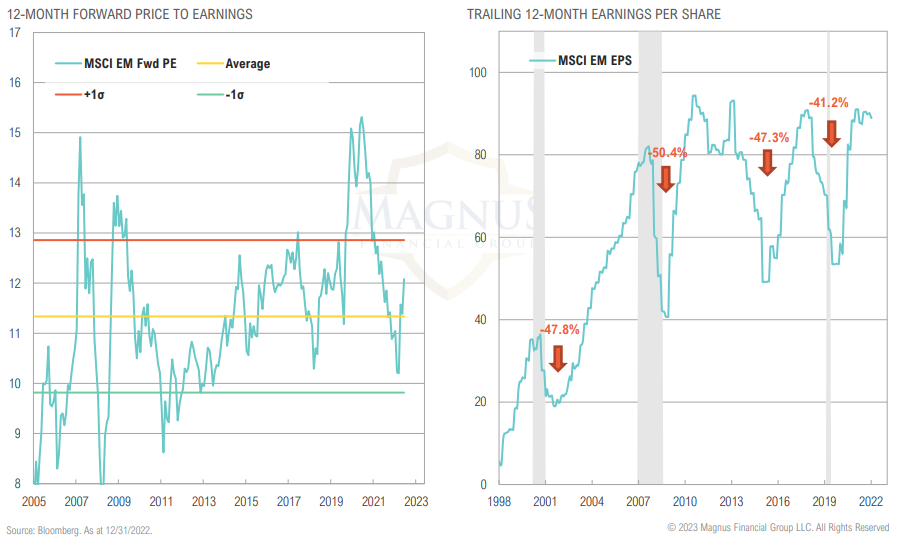

MSCI EM VALUATIONS

EM forward valuations have improved due to bear market, but back above average relative to history; focus now shifts to earnings decline

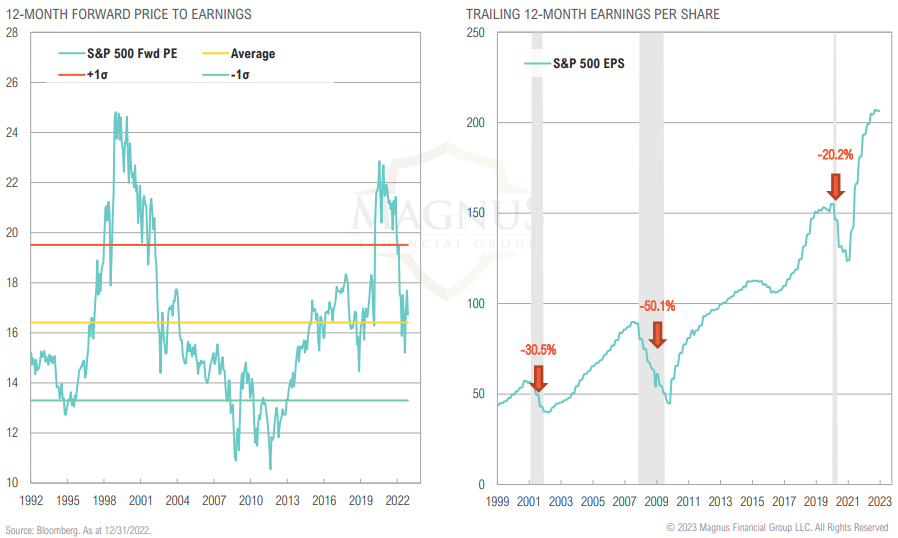

S&P 500 VALUATIONS

U.S. large cap valuations have improved due to bear market, slightly above average relative to history; focus now shifts to earnings decline; history suggests baseline should be at least 20% drop

Adjusting for record-high margins, equity valuations are not compelling

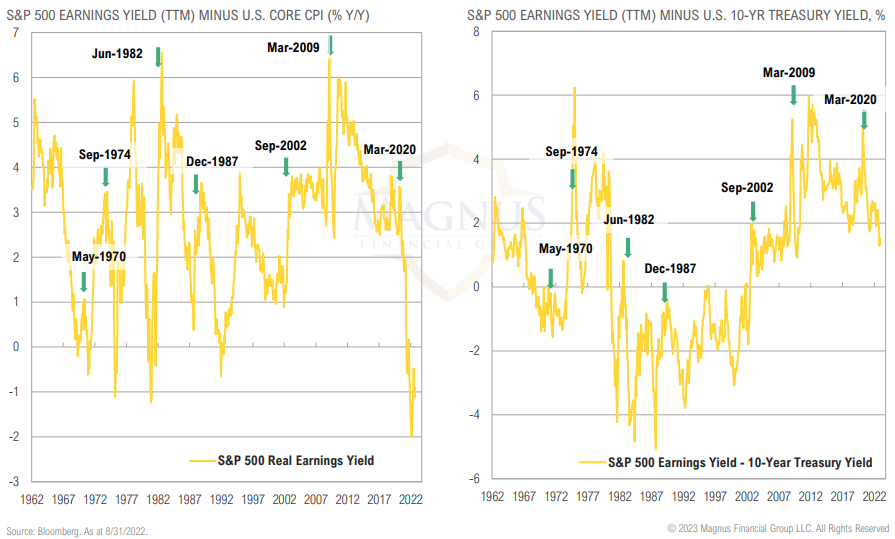

The S&P 500 real earnings yield is still decidedly negative, looks nothing like historical bear market highs (i.e., increases in earnings yield)

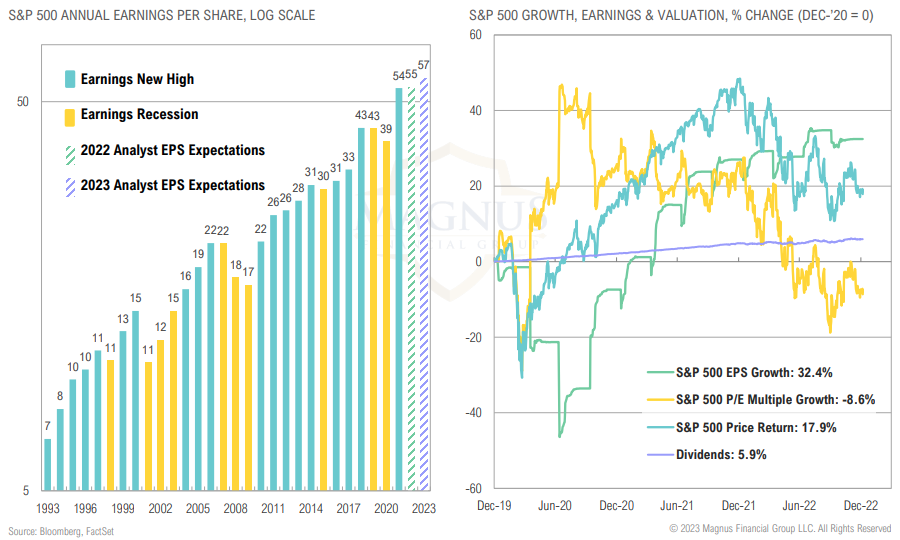

EARNINGS

Current 2023 analyst EPS growth estimates have been reduced to 5.5%

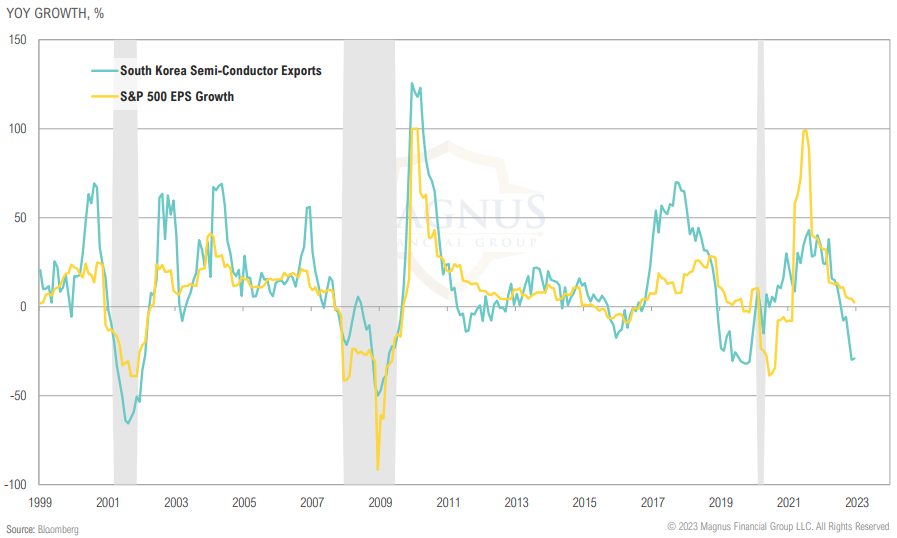

SOUTH KOREA EXPORT ACTIVITY

South Korea semi-conductor exports currently down 29.1% YoY; S&P 500 EPS growth and semi-conductor exports have roughly tracked each other in the past

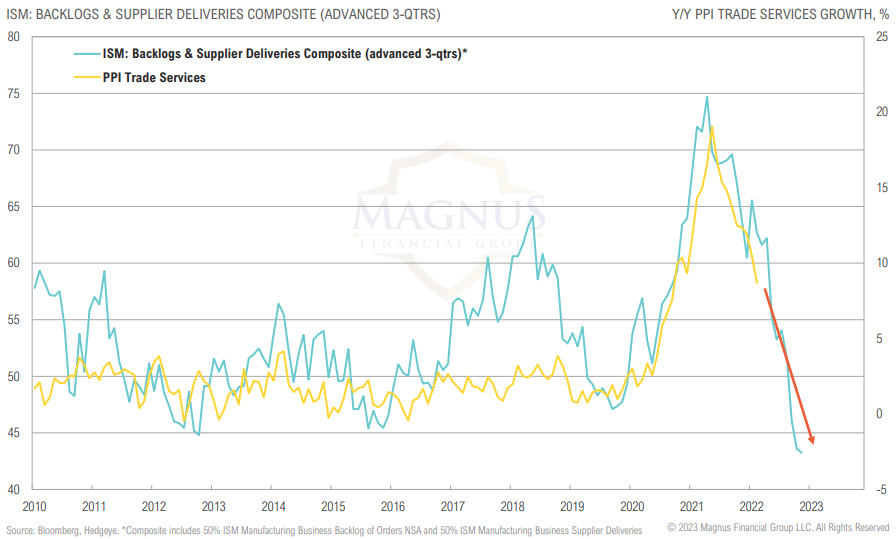

ISM VS CORPORATE MARGINS

Supply chain pressures (proxied by backlogs and delivery times) have led to higher margins (proxied by PPI Trade Services); margins look set to decrease in coming years

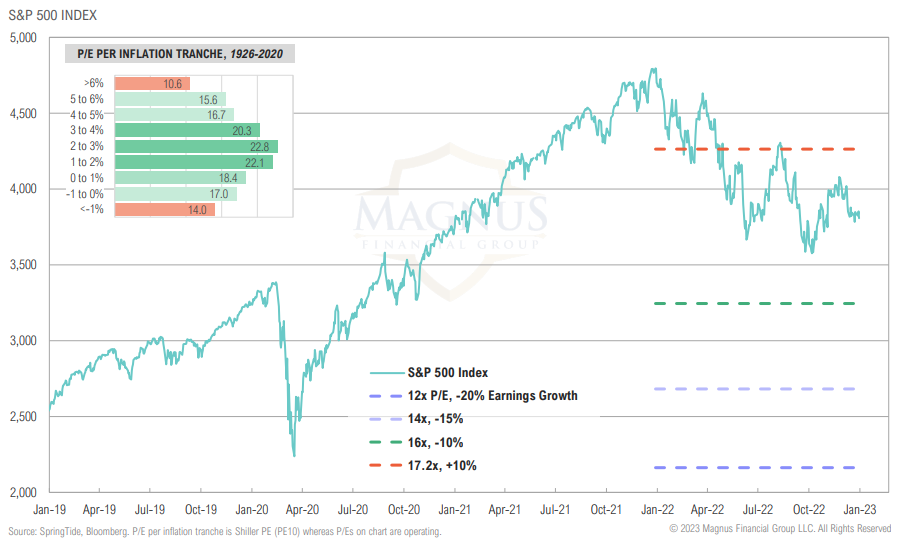

P/E MULTIPLES

What if inflation doesn’t roll and stay lower? How low can we go? P/Es to consider are 16x, 14x, and 12x, applied to various levels of earnings decline

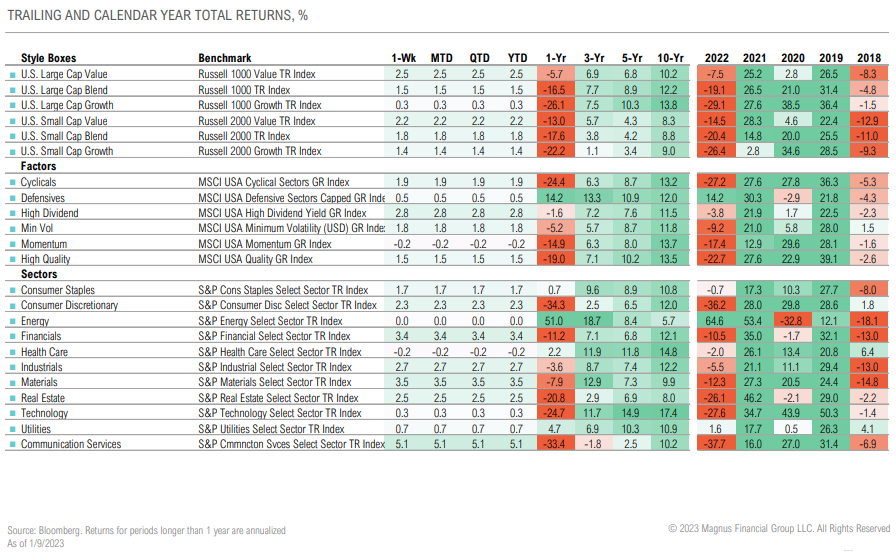

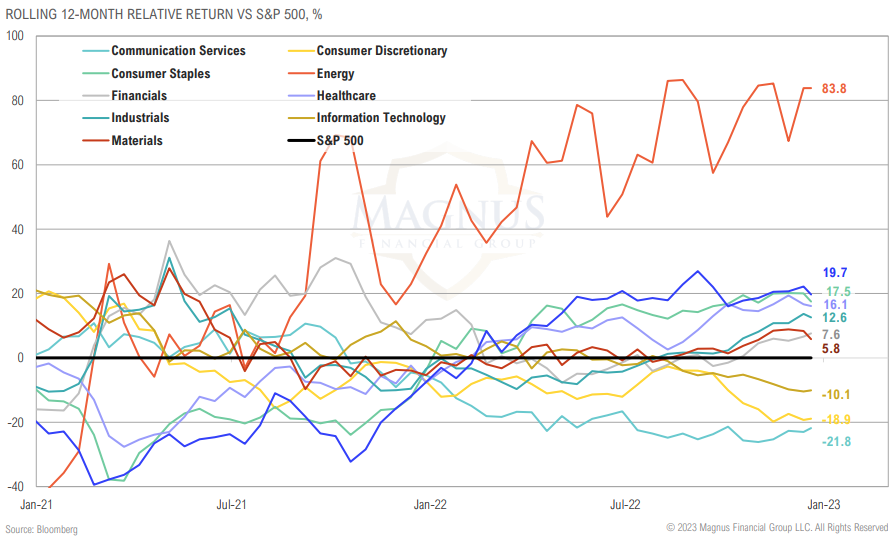

SECTOR RETURNS

Energy outperformed communication services by 105.6% in 2022, the widest sector performance differential since 1991

RELATIVE SECTOR PERFORMANCE

Growth sectors, including consumer discretionary, communication services and technology underperformed in 2022, with no clear indication of trend reversal

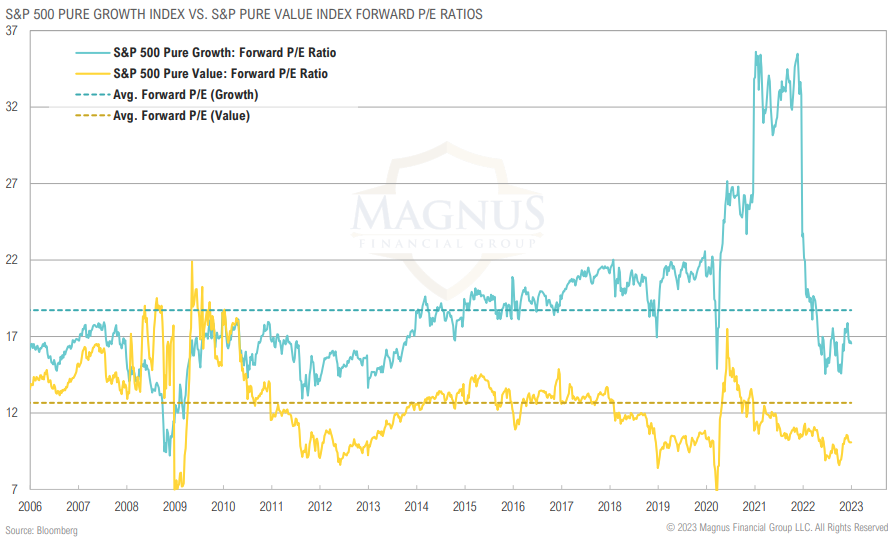

VALUE VS GROWTH

Forward-looking valuations improved dramatically, but earnings estimates will now come into question given potential margin pressure; value still looks relatively cheaper (i.e., this is not 2008-2010)

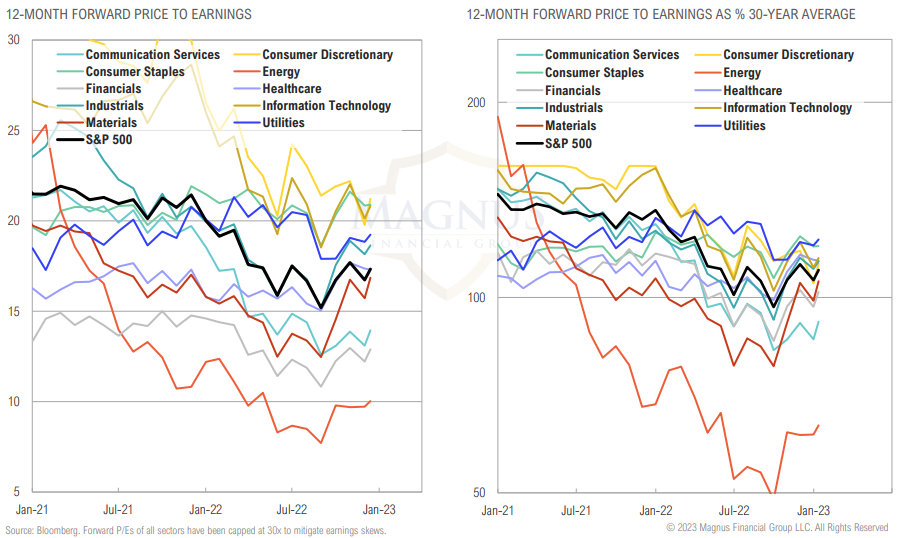

S&P 500 SECTOR VALUATIONS

Energy and Communication Services are currently the only two sectors which are trading below their 30-year average valuations

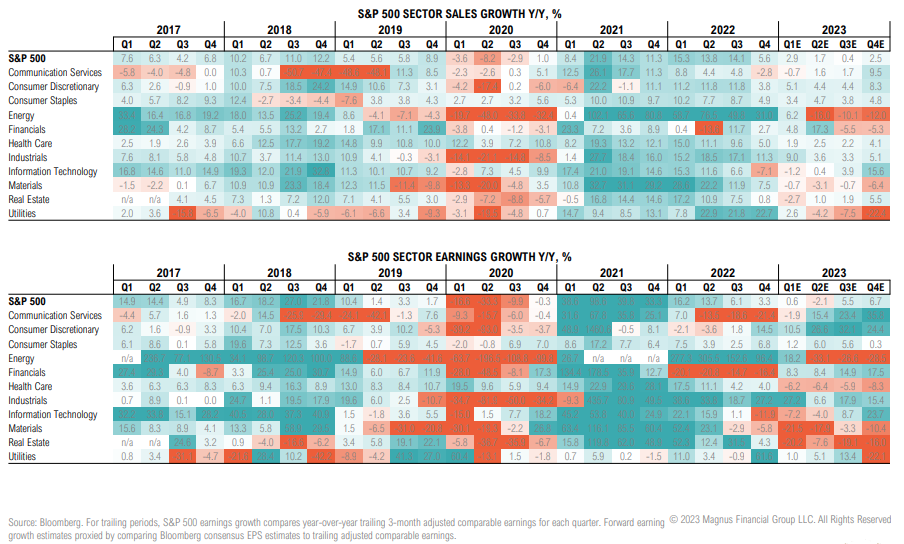

SALES & EARNINGS GROWTH

Nominal sales and earnings growth expected to decelerate but remain positive in 2023; impact of inflation and potential recession remain wild cards

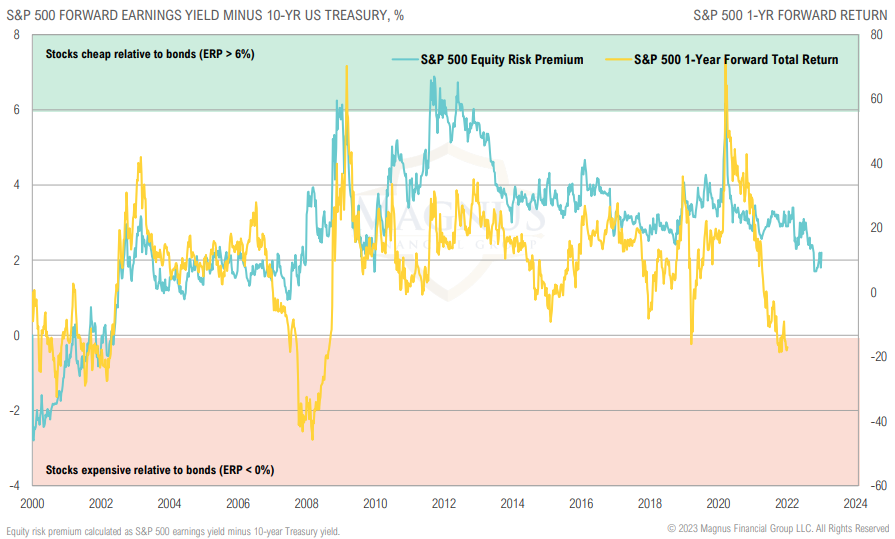

S&P 500 EQUITY RISK PREMIUM

Despite being in a bear market, stocks are arguably less attractively priced vis-à-vis bonds than they were coming into 2022

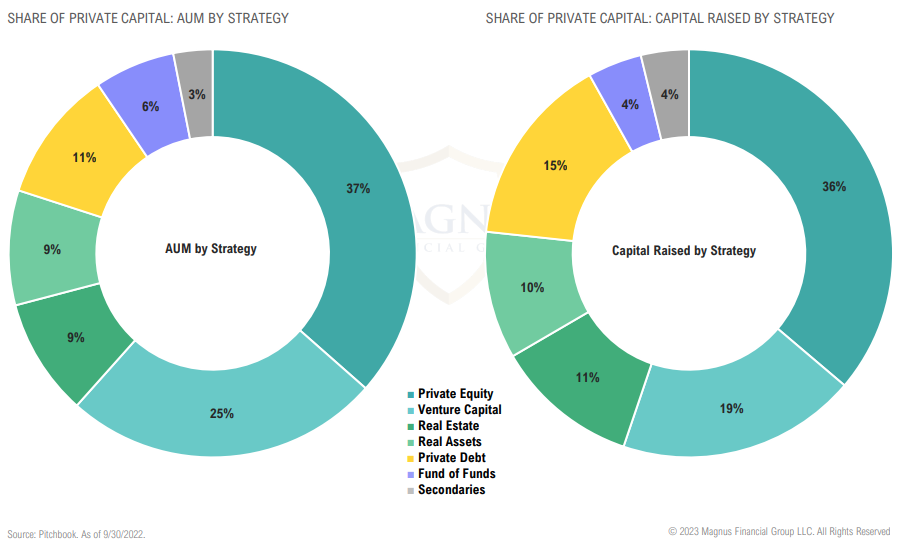

PRIVATE MARKET SHARE

Private markets dominated by private equity and venture capital

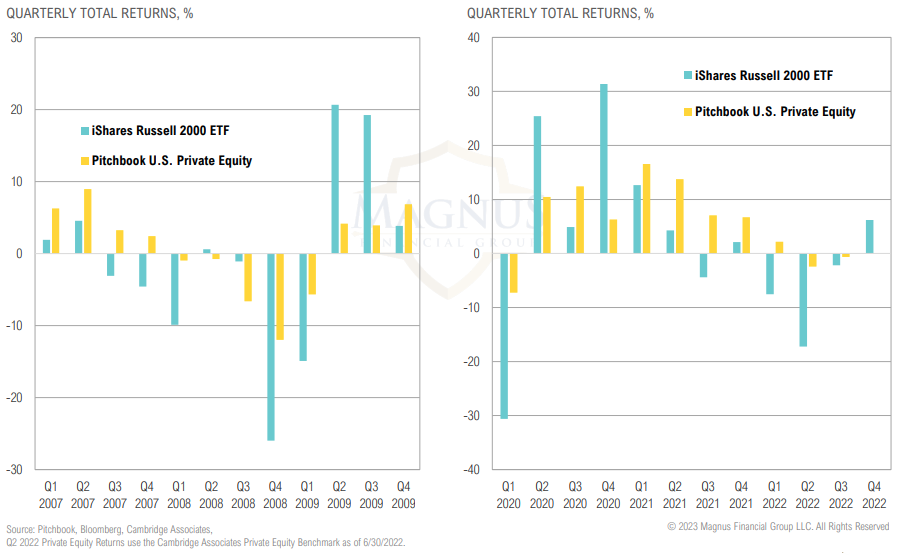

PRIVATE EQUITY

Private equity funds have not marked down their portfolios like they did in the GFC

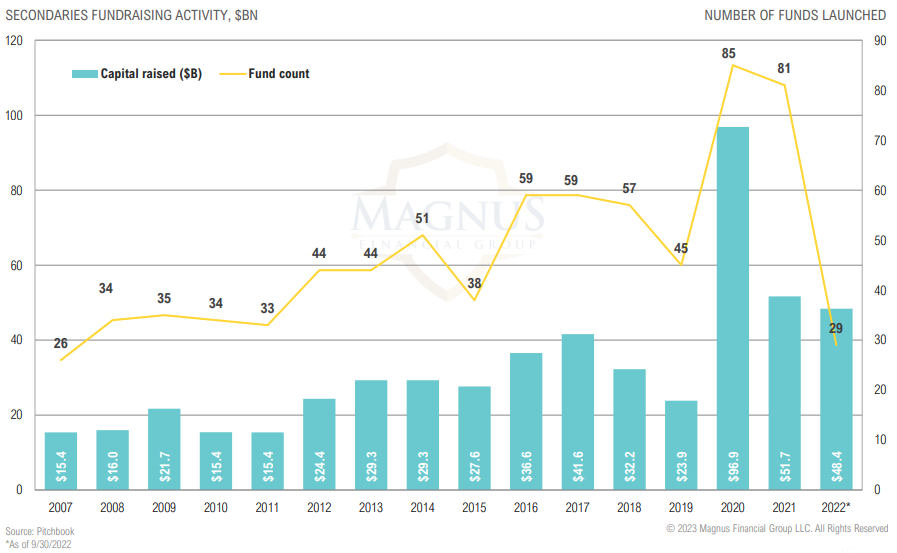

PRIVATE EQUITY SECONDARIES

Secondaries fundraising activity sees large increase in Q3

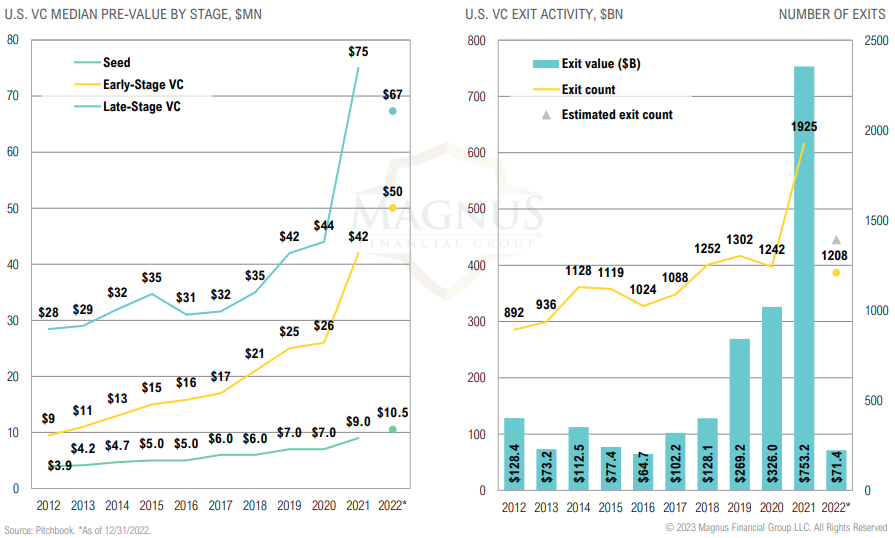

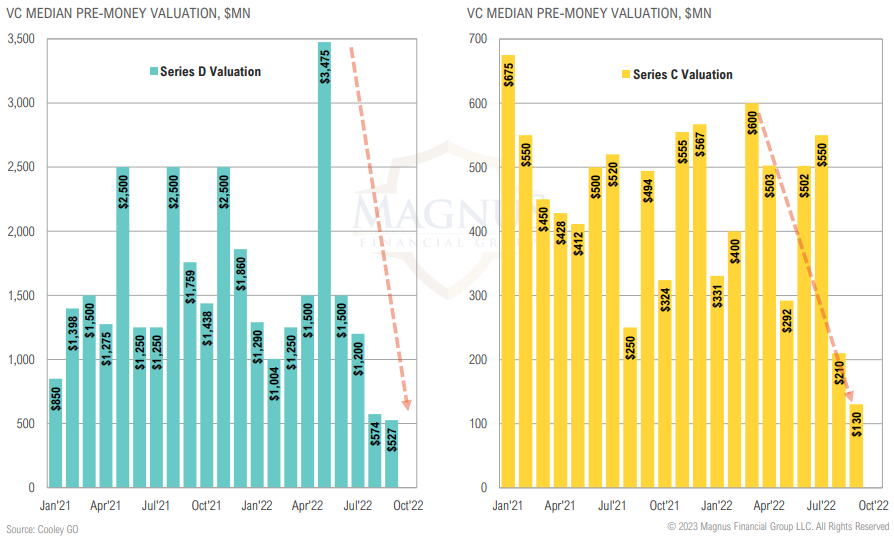

VENTURE CAPITAL

Overall, venture valuations remain high while exits are on pace for lowest year since 2016

However, significant cracks are emerging; later-stage venture capital valuations cratered during Q3 of 2022

FIXED INCOME & CREDIT

Inflation is eroding everything I just said, and that $1.5 trillion will run out sometime mid-year [this] year. When you are looking that forward, those things very well may derail the economy and cause this mild to severe recession that people are worried about.

– Jamie Dimon, JPMorgan CEO

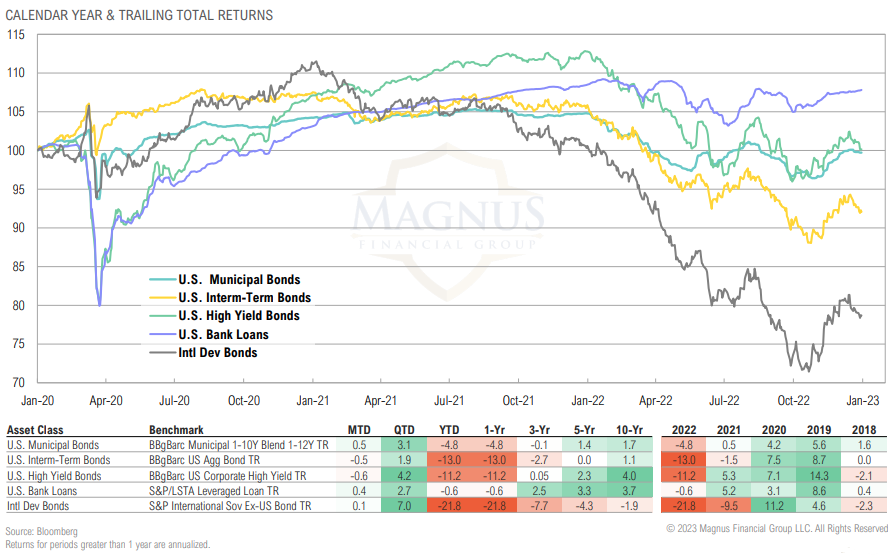

MARKET RETURNS SUMMARY

All U.S. and international fixed income & credit asset classes were up over the quarter; while international developed bonds performed best in Q4, they were the worst 2022 performer

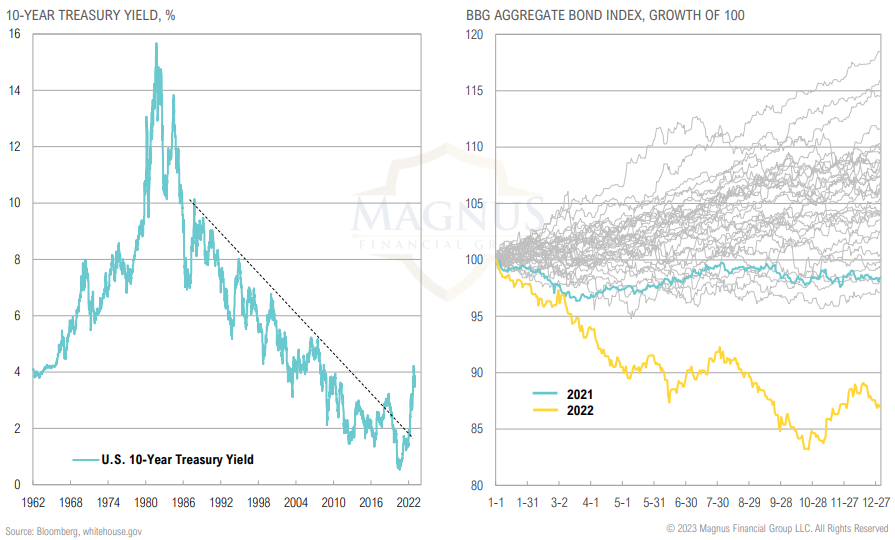

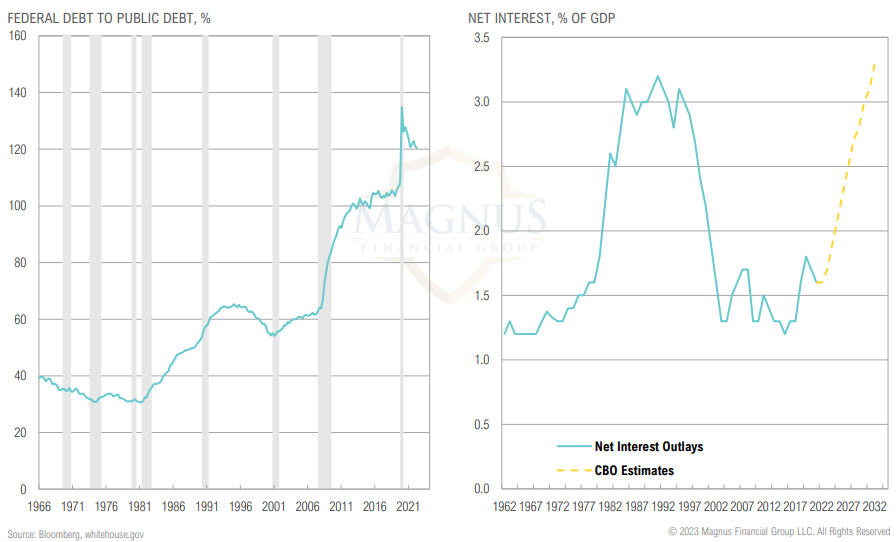

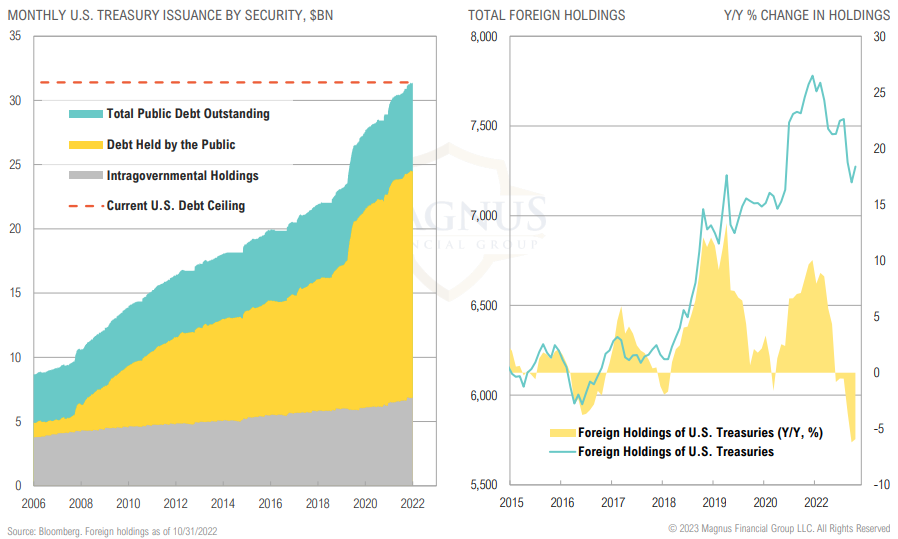

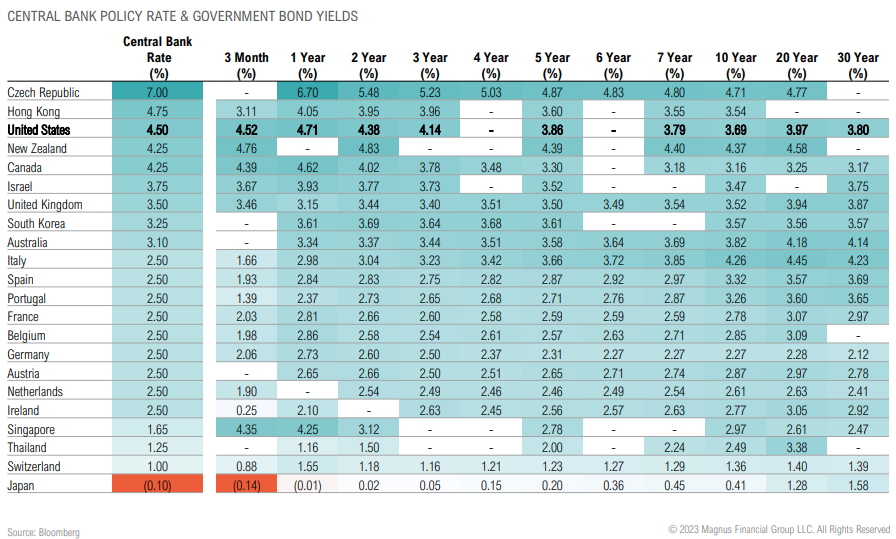

TREASURY MARKET

Context is important for Treasury markets

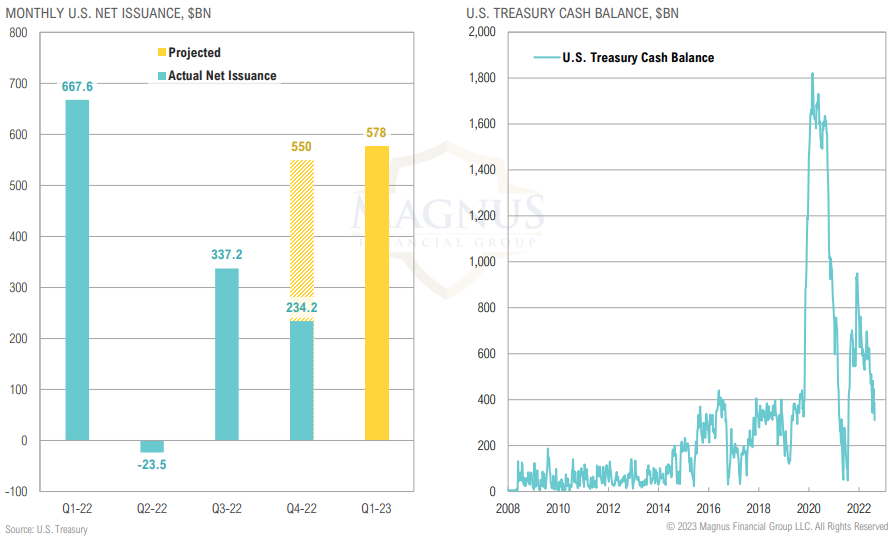

TREASURY ISSUANCE

Q1 2023 net issuance was expected to be $578Bn; Treasury cash balance now at $310Bn

Q1 2023 net issuance expected to be $578Bn; Treasury cash balance now at $310Bn

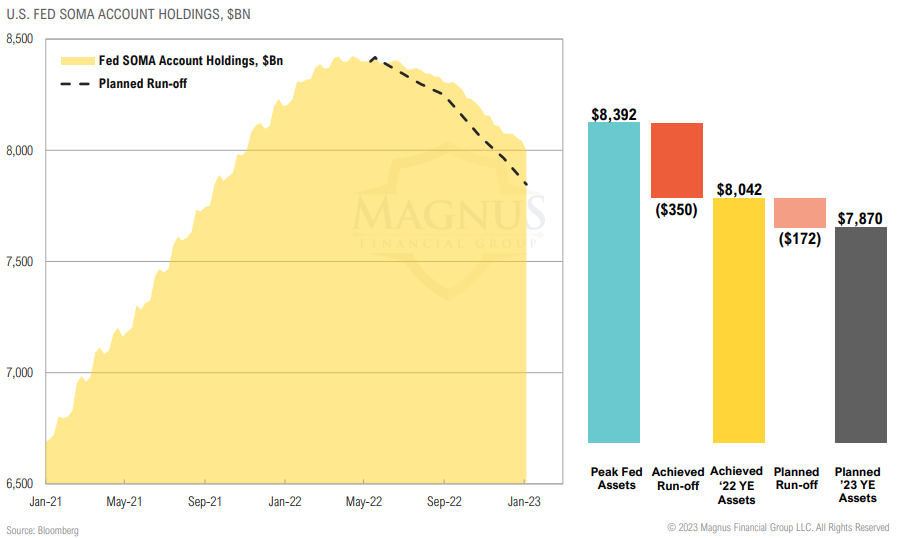

FED ASSETS

Fed’s planned balance sheet reduction ($47.5 bn/month from Jun-Aug ‘22 and $95bn from Sep ‘22) has started to take shape, even if massively lagging planned pace

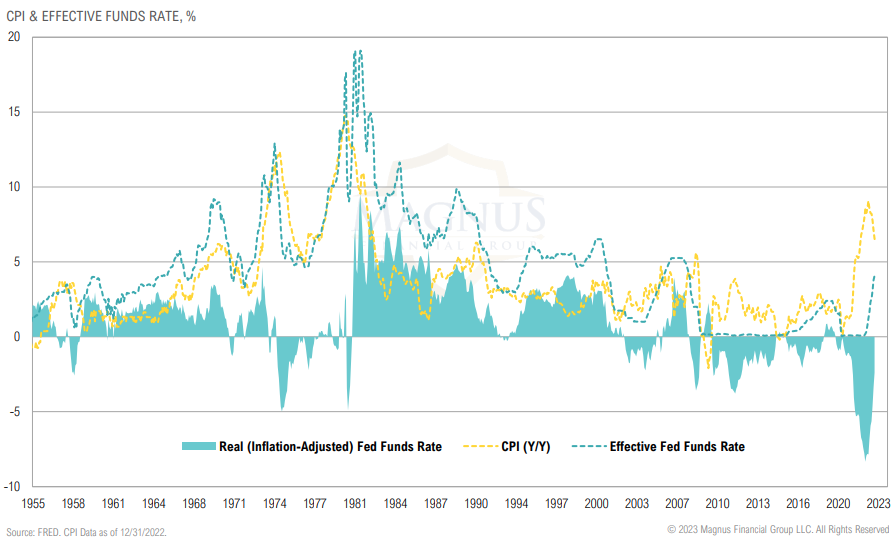

REAL INTEREST RATES

While CPI has rolled over from peak, the effective Fed funds rate is still negative

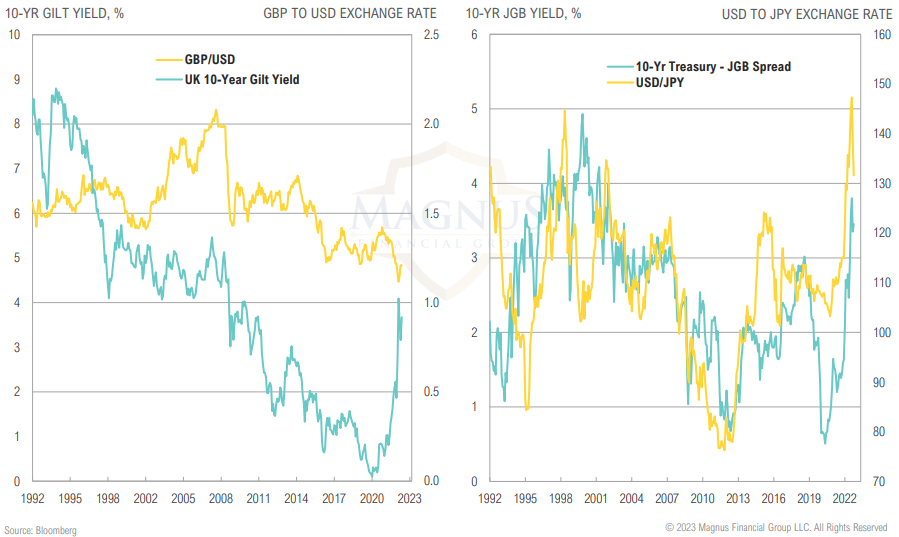

GLOBAL YIELDS & DOLLAR

Market increasingly punishing policy mistakes, especially when you’re not the global reserve currency

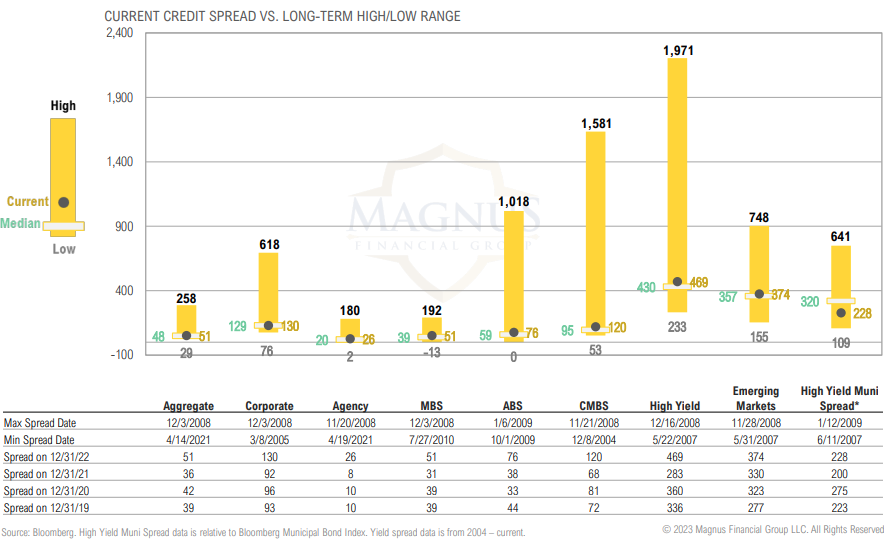

SPREADS BY SECTOR

Credit spreads at or modestly above average across most sectors; starting to shift up slightly as recession fears start to become more entrenched

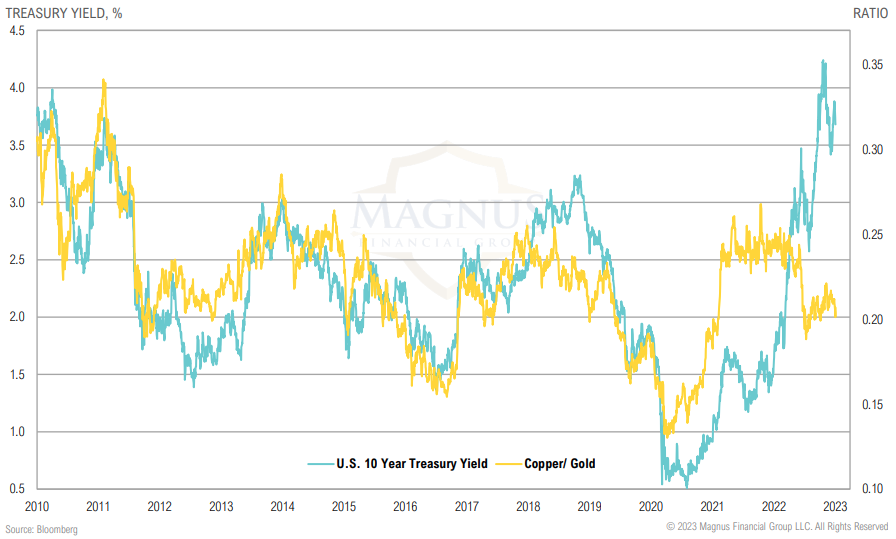

COMMODITIES & THE YIELD CURVE

Collapse in copper/gold ratio—a proxy for the real economy vis-à-vis financial assets—suggests Treasury yields may head lower

GLOBAL RATES

The U.S. bond market remains relatively higher yield, which could help keep U.S. rates somewhat contained

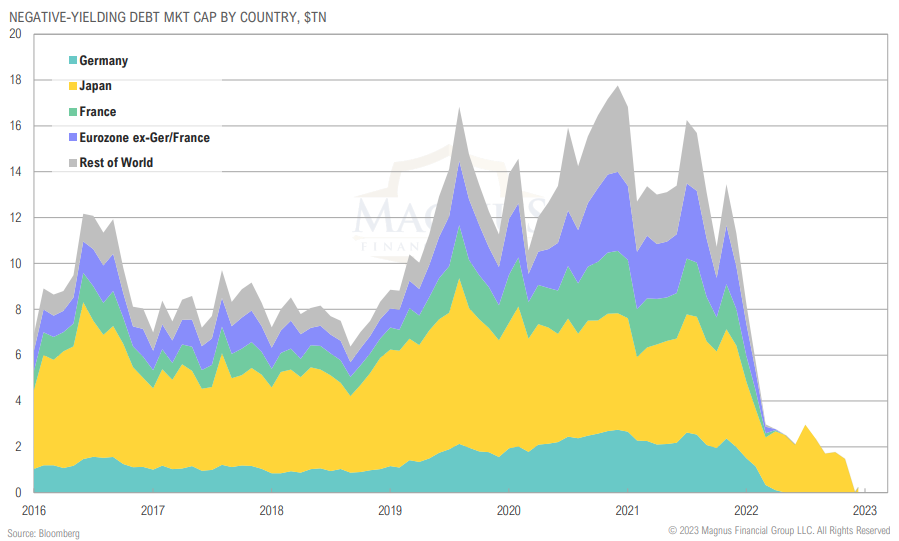

NEGATIVE-YIELDING DEBT

The end of an era? We hope so…

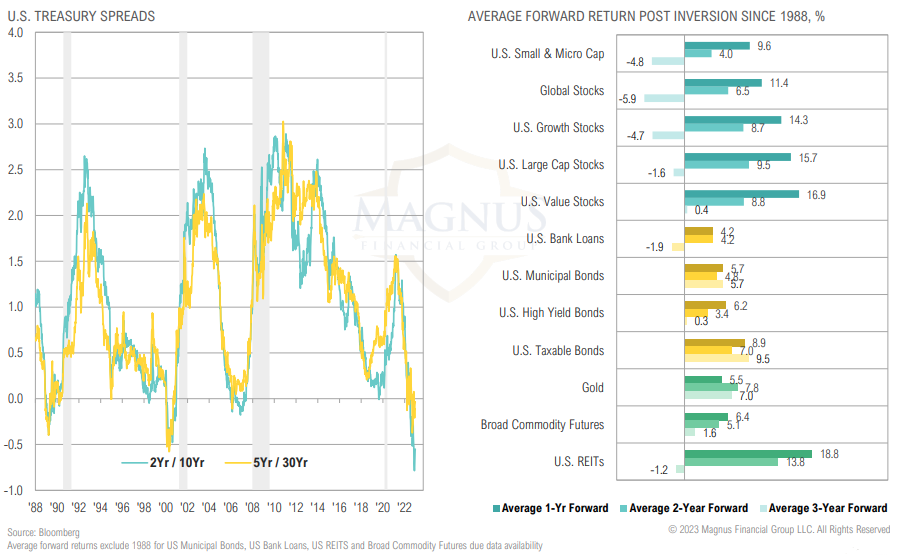

TREASURY SPREADS

Yield curve inversion signaling slowing growth; risky assets can generate strong short-term returns post inversion, but we don’t like “pennies in front of steam roller” trades

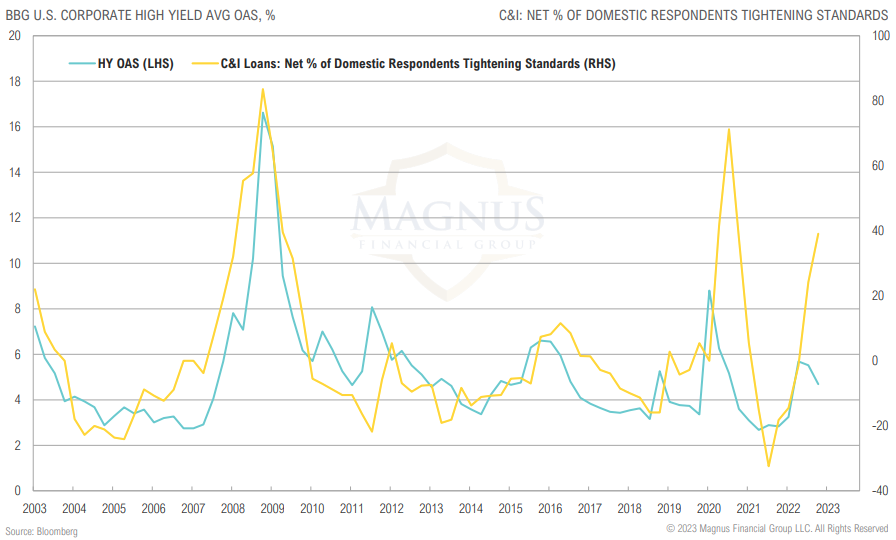

HY OAS VS LOANS

Domestic banks have tightened lending standards sharply over recent months, an event which has generally been associated with wider credit spreads

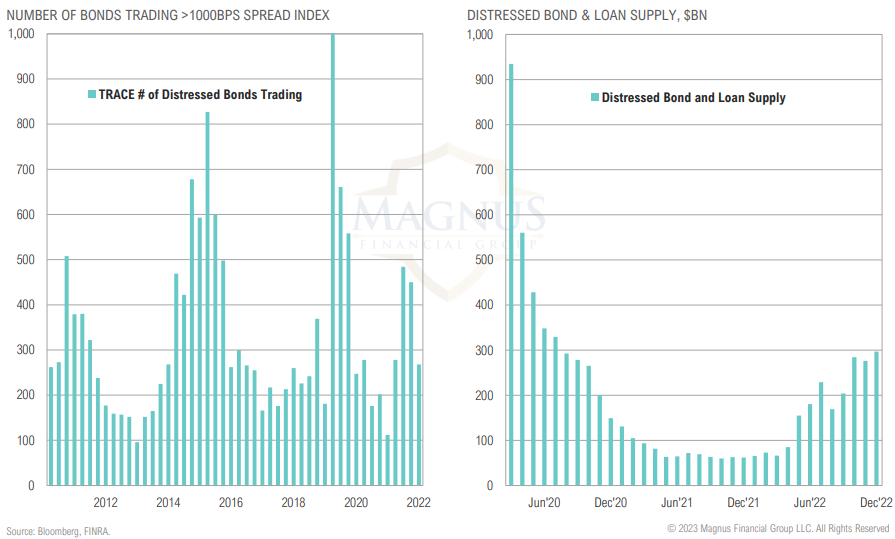

DISTRESSED DEBT

Supply of distressed debt has been on the rise over recent quarters

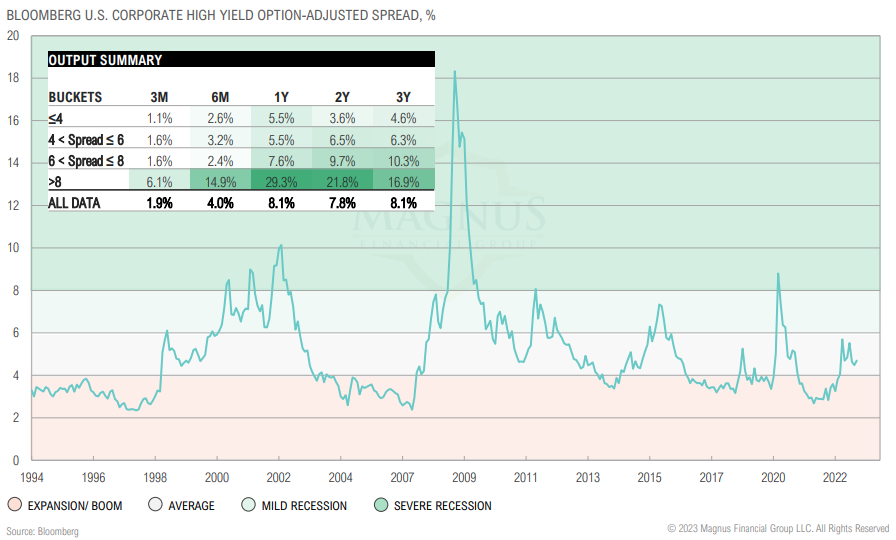

HIGH YIELD SPREADS

Historically, high yield spreads above 6% have resulted in above-average forward returns; high yield spread currently trading at a middling 4.7%

Historically, high yield spreads above 6% have resulted in above average forward returns; high yield spread currently trading at a middling 4.7%

REAL ASSETS

…we’re spending over a trillion dollars less than what I’ll call the previous cycle. That’s 2010 to 2014. So since 2015, the industry worldwide is spending over a trillion dollars less in investment.

– Scott Sheffield, Pioneer Natural Resources CEO

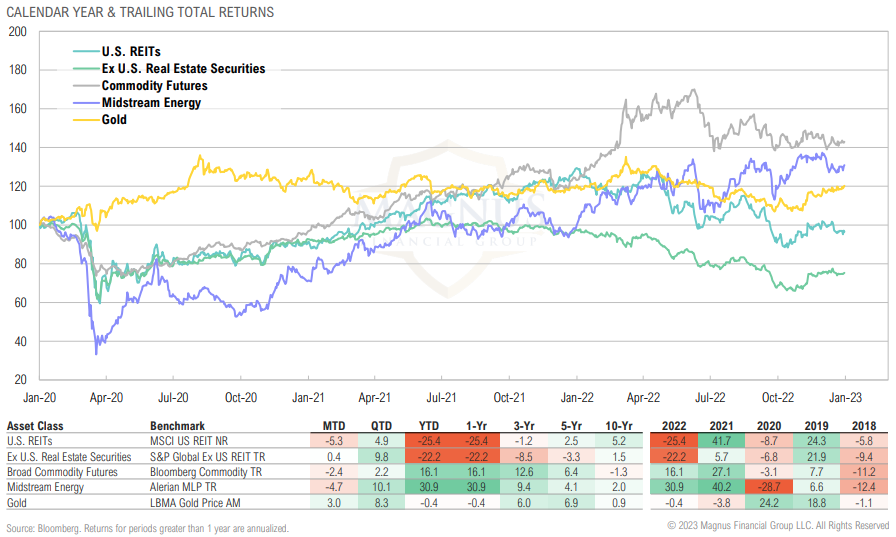

MARKET RETURNS SUMMARY

Broad commodity futures and midstream energy were among the top performing real assets over 2022, while both U.S. and global REITs ended the year in bear market territory

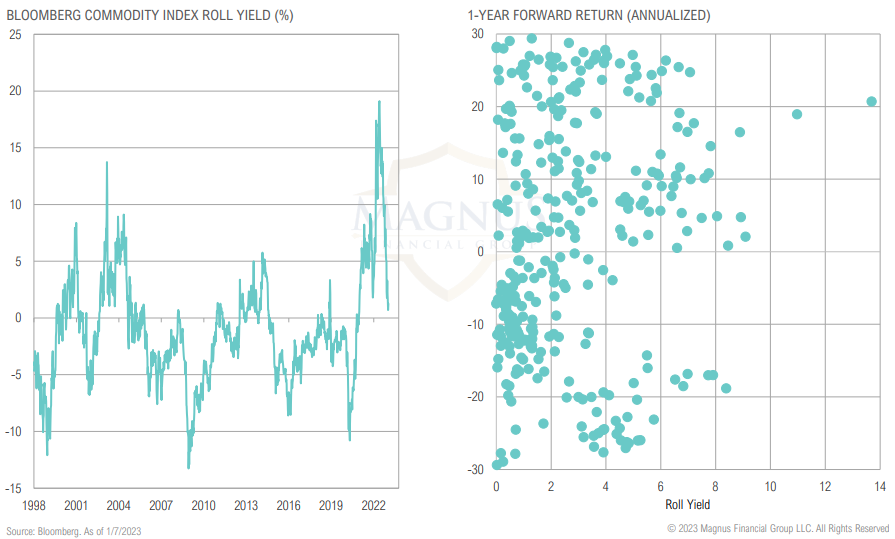

COMMODITIES

Commodity roll yields have dropped sharply, largely due to natural gas futures shifting back to contango, suggesting global commodity markets have loosened

OIL & NATURAL GAS

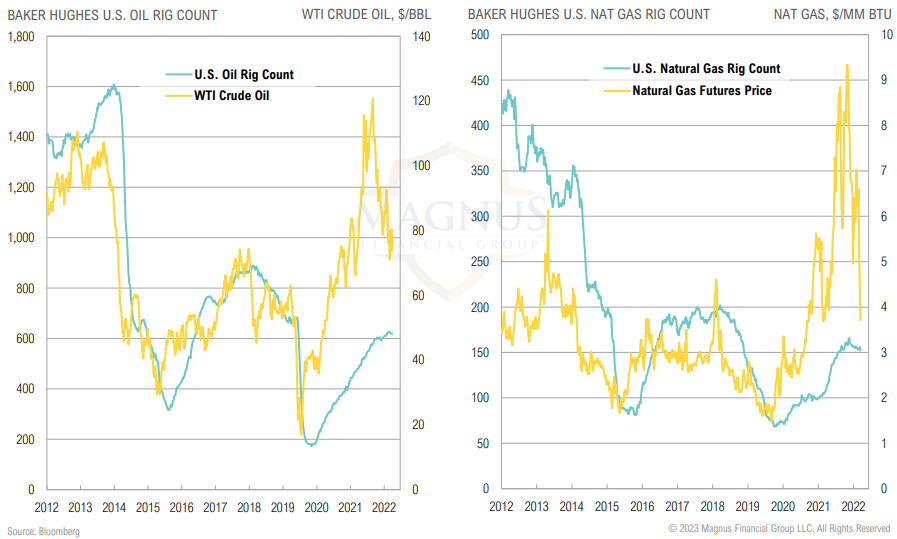

Oil and natural gas producers have slowed increases in rig counts as prices have rolled over

OIL PRODUCTION/CONSUMPTION

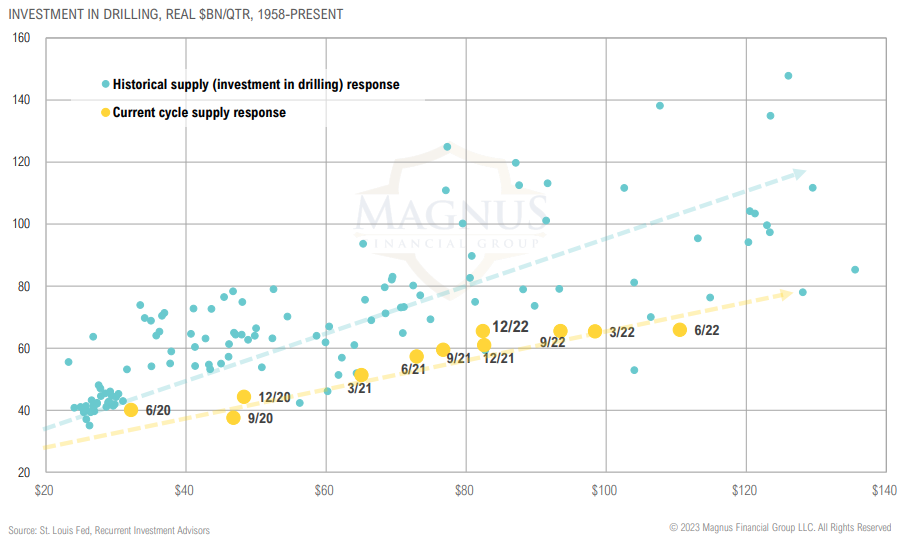

Since COVID, drilling capex levels have been near the bottom of a 65-year range

OIL PRODUCTION/CONSUMPTION

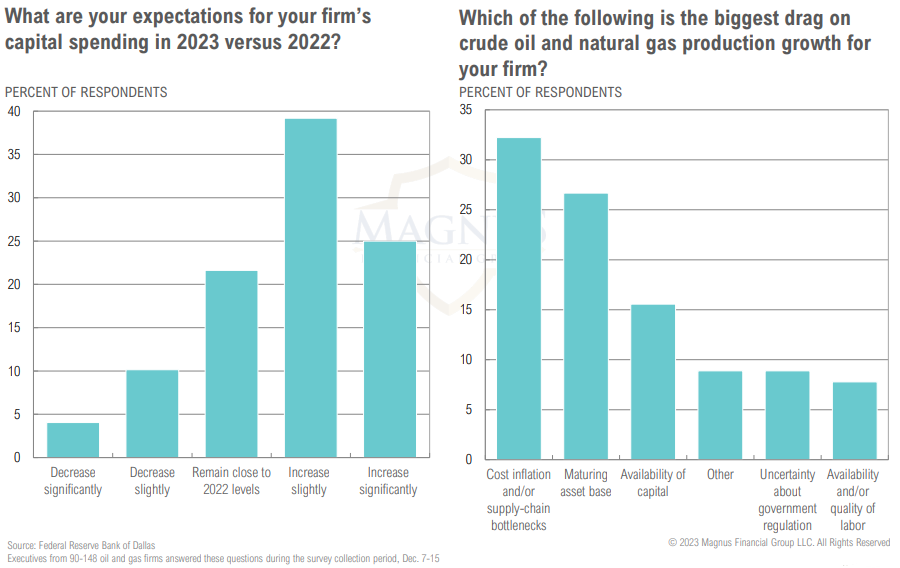

Oil executives expect to start ramping up capex in 2023

ENERGY PRICES

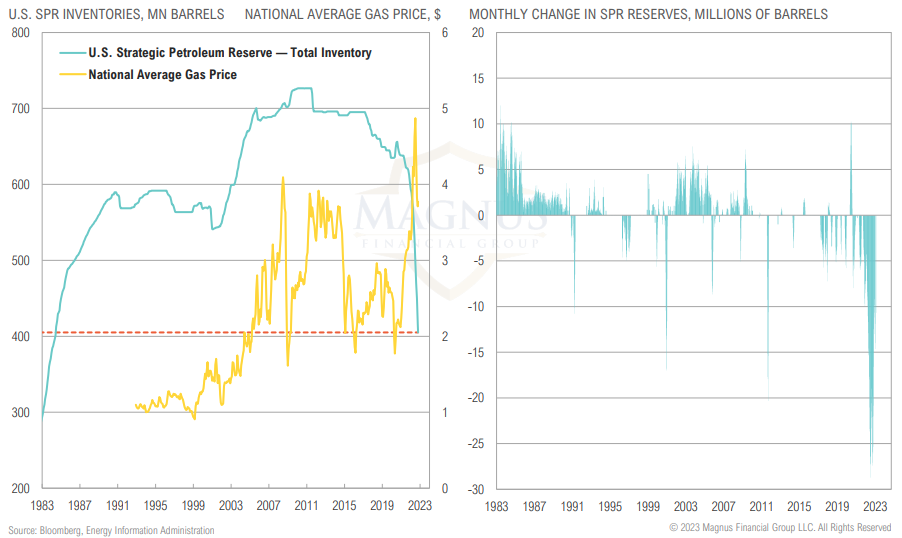

SPR dump helped ease gas prices & inflation pressures, but is not expected to continue in 2023, eliminating a key headwind for gas prices

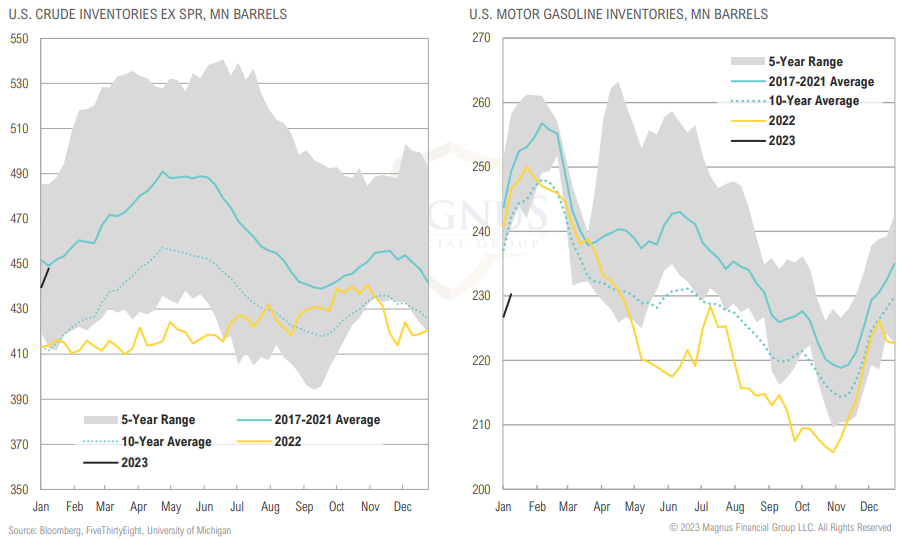

Crude inventories have built to start the year while gasoline inventories remain tight relative to the past five years

OIL & NATURAL GAS

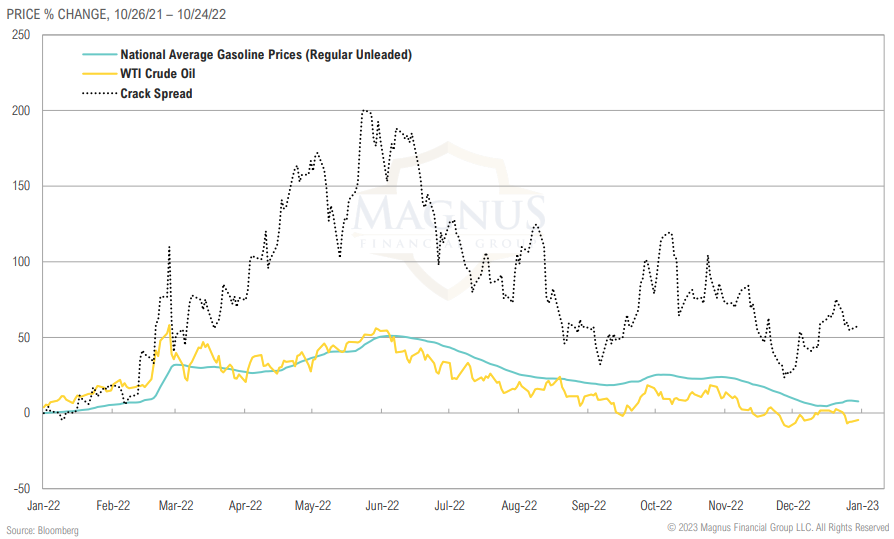

Crack spreads remain elevated despite the decline in oil prices, signaling continued constrained refinery capacity

YIELDS

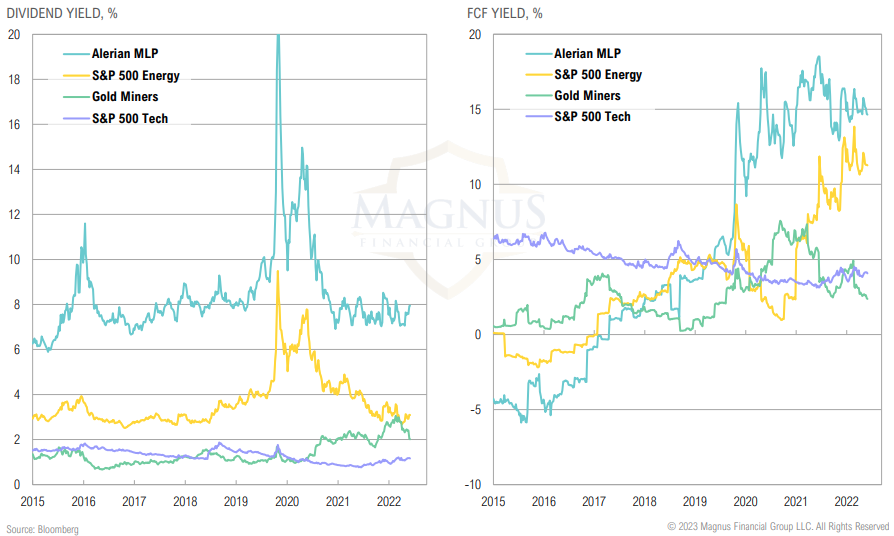

Midstream distribution yields trending lower as sector breaks out to upside but remain relatively attractive, free cash flow yields of energy sector remain attractive

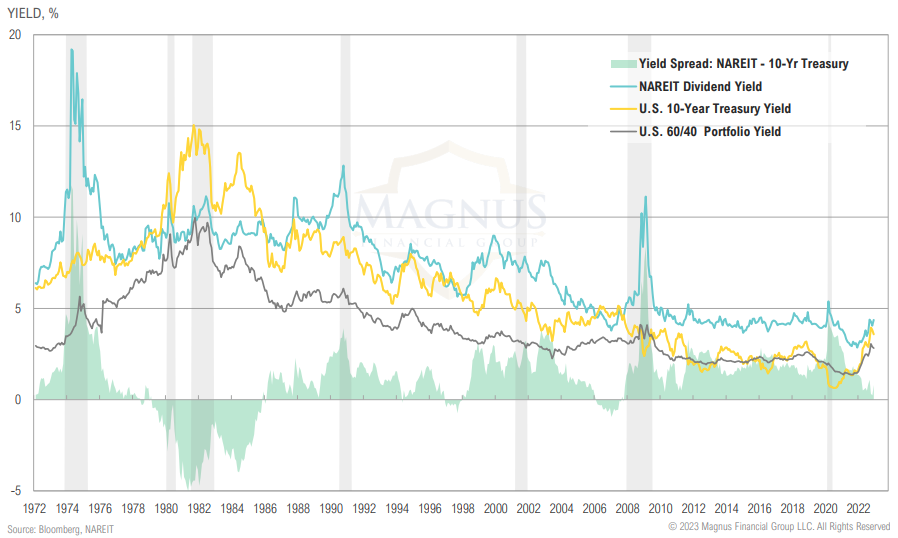

REITS

Even after ending 2022 down 24.5%, REIT yields are wholly unattractive on a relative basis and near lowest levels in history on an absolute basis

PRIVATE MARKETS

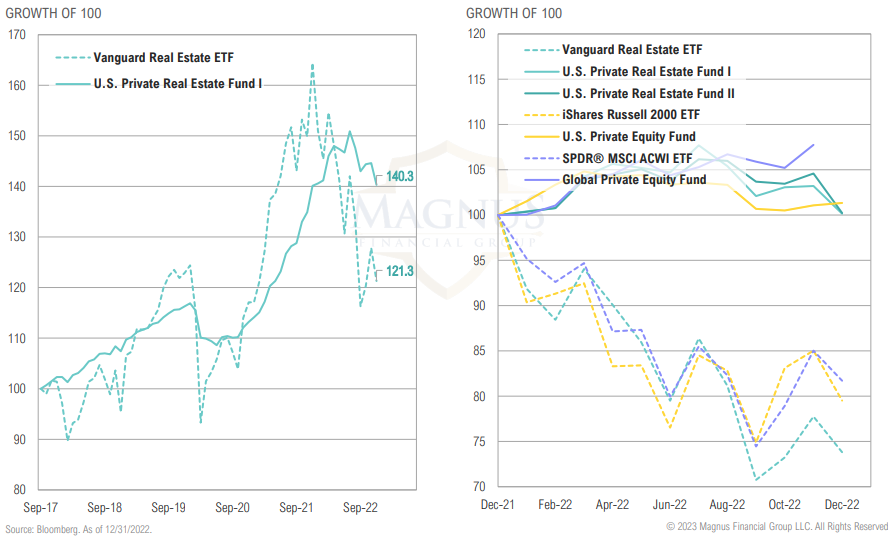

Private market interval funds have significantly outperformed their passive investable benchmarks YTD as net asset values have yet to catch down to reality

PRIVATE REAL ESTATE

Private real estate funds have not marked down properties like they did in the GFC

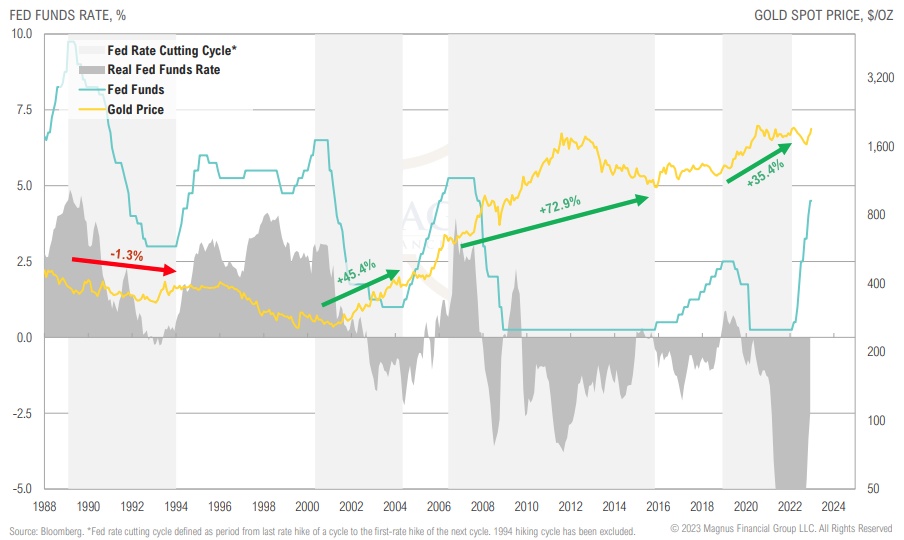

GOLD VS FED FUNDS

Since the turn of the century, the end of hiking cycles have been positive for gold; this may be due to lower opportunity costs (falling real rates)

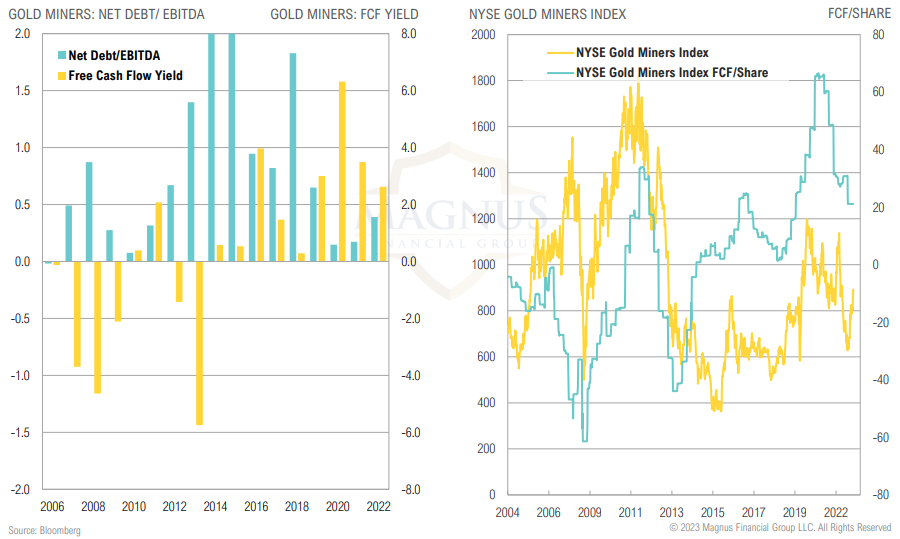

GOLD MINER FUNDAMENTALS

Gold miners have rallied >40% from Sept ‘22 lows, as spot gold prices catch a bid, but the rising of operating costs remains a key risk for miners

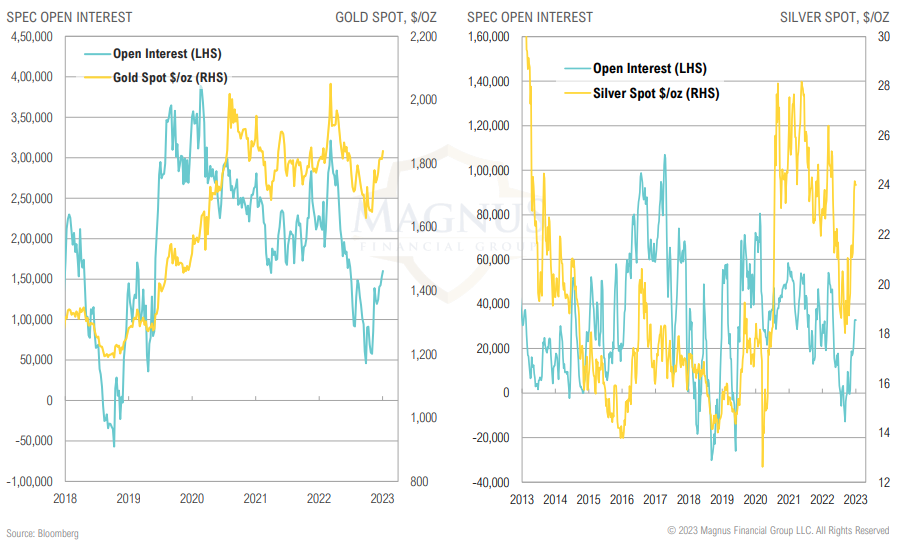

GOLD FUTURES POSITIONING

Spec positioning in gold futures increased modestly over the December, but nowhere near stretched, suggesting recent rally may have legs

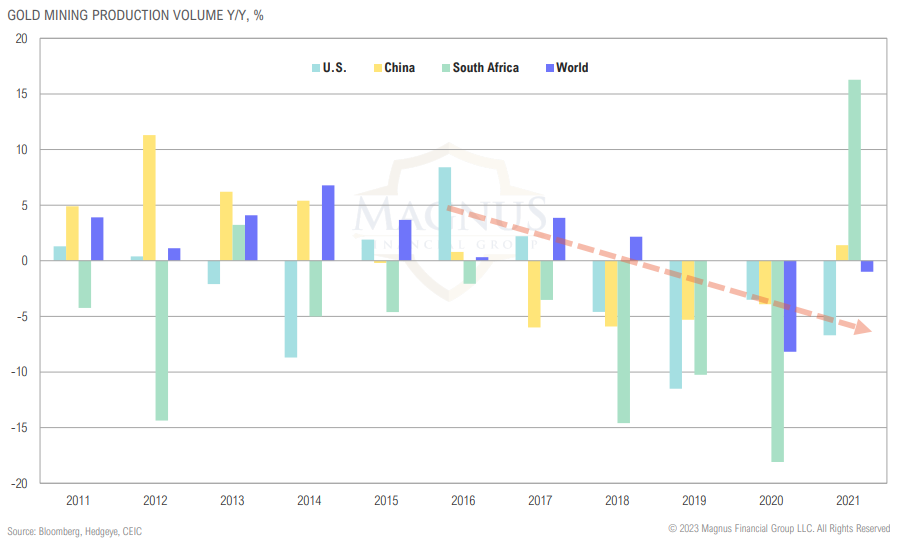

GOLD PRODUCTION

Global gold production volumes have been tracking lower in recent years

OPPORTUNISTIC

We also had the China lockdown situation, which now appears to be resolved. So the China market, it’s a big market, and we expect that to resume growth. And we are going to take a couple quarters, as we said, for the inventory to clear up before we get normal demand.

– Cristiano Amon, Qualcomm CEO

MARKET RETURNS SUMMARY

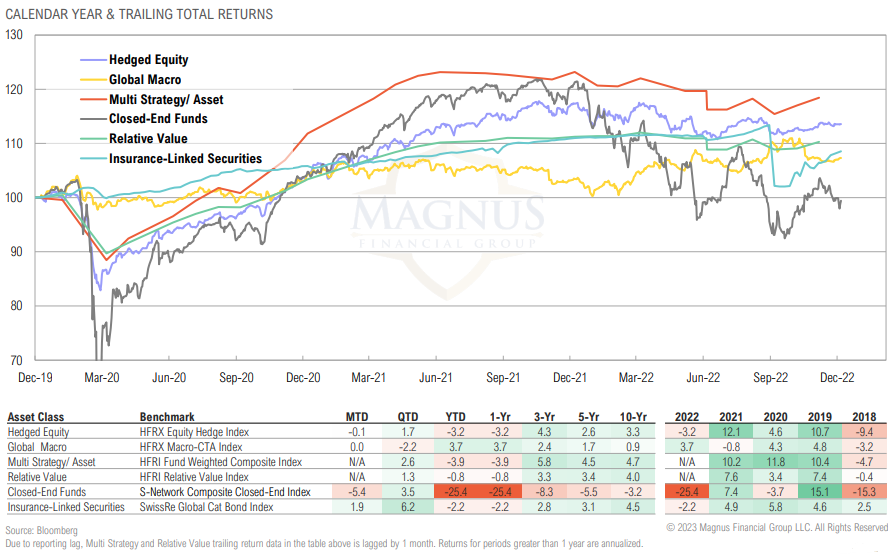

While global macro was the only opportunistic asset class with negative Q4 returns, contrarily it was also the only strategy to produce positive returns over 2022

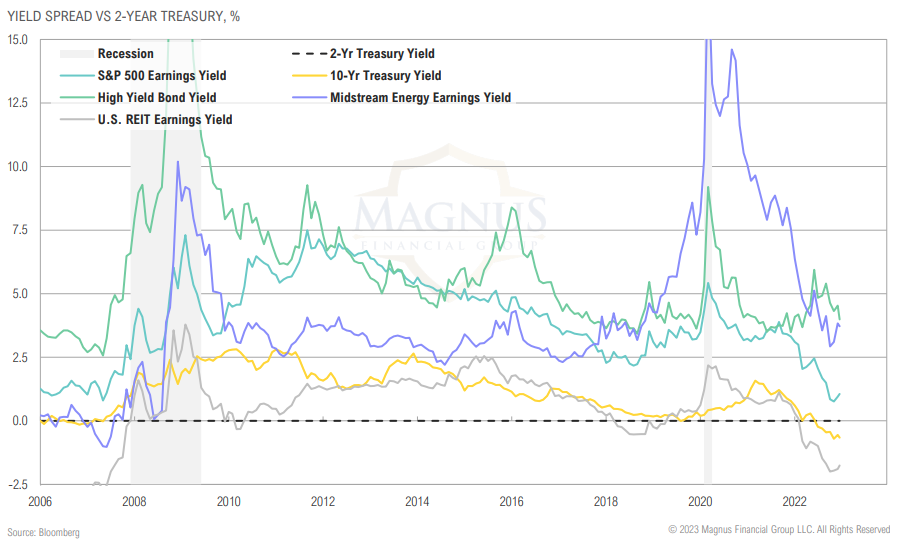

YIELD SPREADS

Most asset classes don’t look attractive relative to the 2-year Treasury yield; spreads have some way to go if past recessions are at all indicative

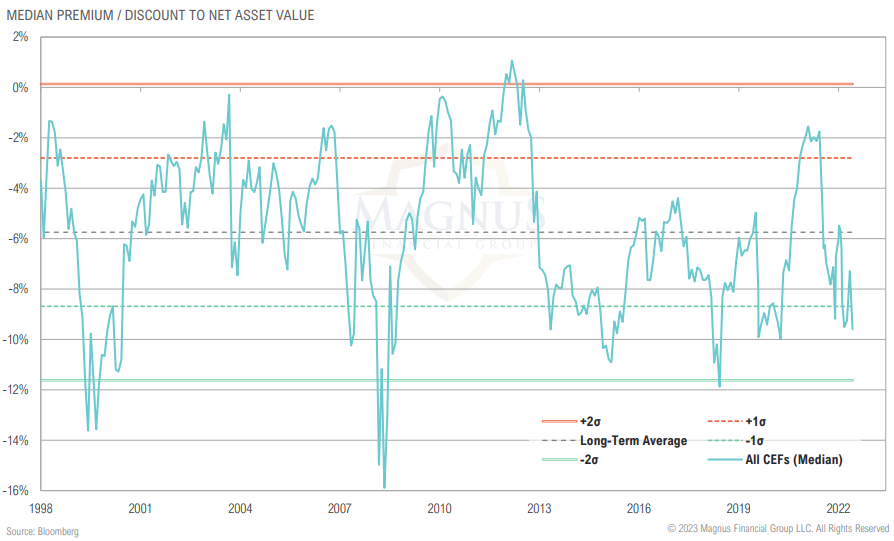

CEF DISCOUNTS

CEF discounts widened to -9.6% in December; U.S. taxable bond discounts widened in December back above 6.0% after narrowing to 3.7% in November

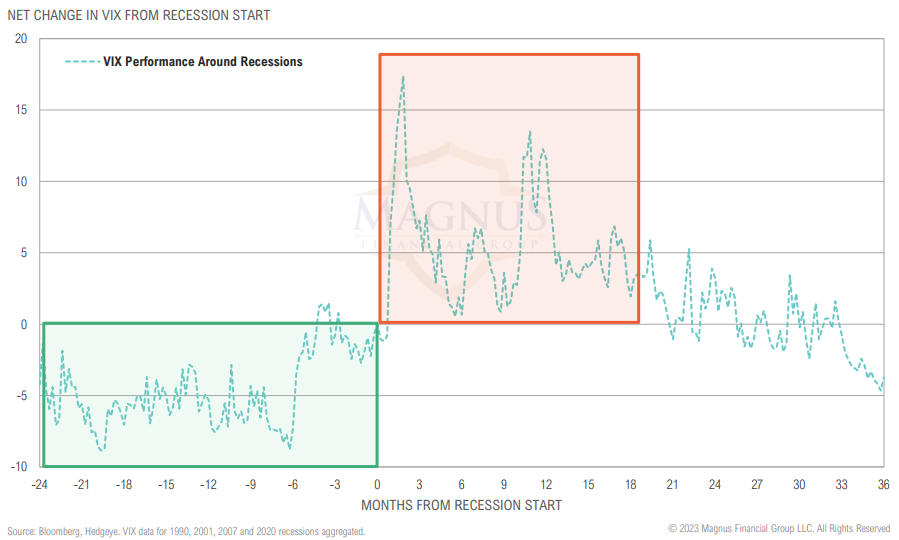

VIX VS RECESSIONS

Historically, the VIX has spiked and remained elevated for extended periods after the start of a recession — but remember, volatility brings opportunity!

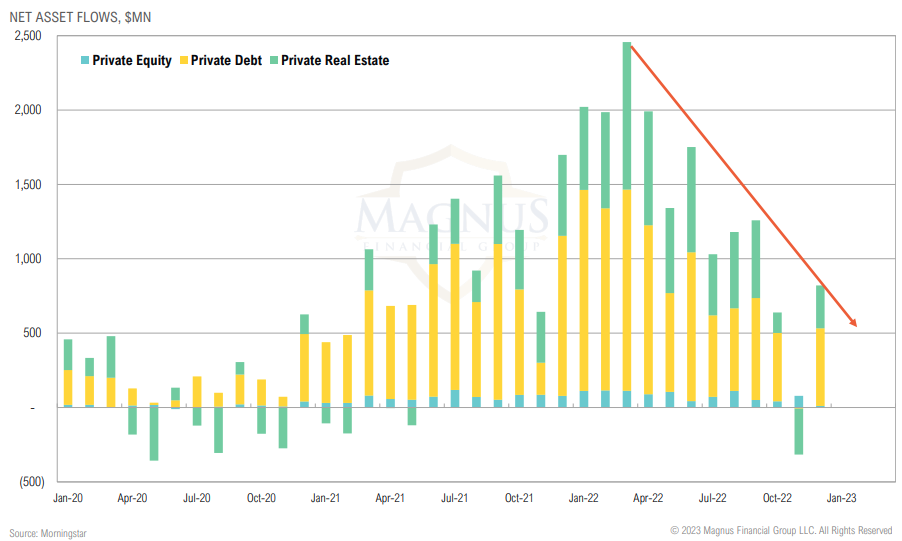

INTERVAL FUND FLOWS

Interval funds saw massive inflows in 2021 and 1H 2022, but these may be starting to reverse

ASSET ALLOCATION

Regardless of industry, as the macro uncertainty has increased, right, they’re being a little bit more cautious. So we’re seeing some delays in decision-making. We see changes in the pace of spending, and we’re seeing some pausing of the smaller deals. And all of this impacts the smaller deals more

– Julie Sweet, Accenture CEO

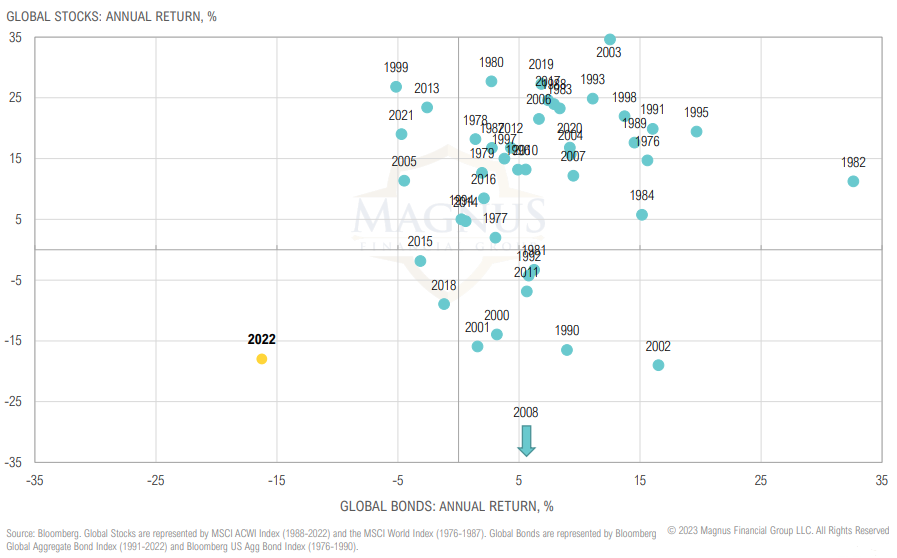

STOCKS & BONDS

2021 was an unusual year for global stocks and bonds, 2022 even more so; again, highlighting the unusual predicament the Fed is in

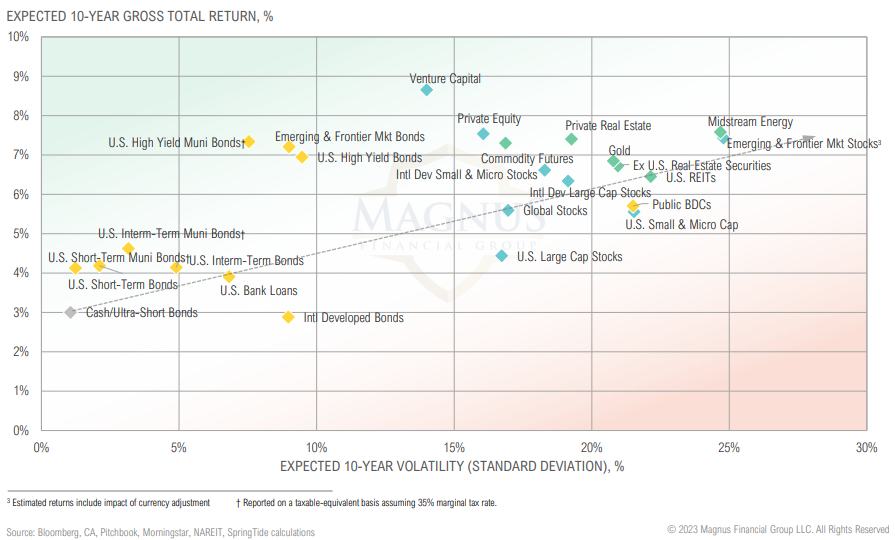

CMEs (AS OF 12/31/2022)

Expected 10-year returns for most assets fell marginally as yields fell and equity valuations rose throughout the quarter

CMEs (AS OF 12/31/2022)

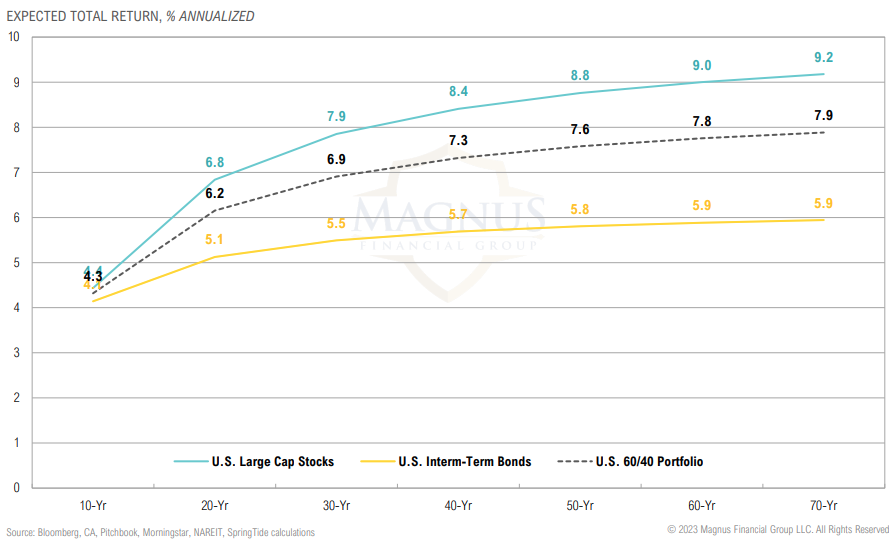

Fixed income returns continue to offer similar returns to U.S. large cap stocks over 10 years (pre-inflation, which is big unknown)

APPENDIX 1

ASSET CLASS DEFINITIONS

ASSET CLASS BENCHMARKS

Asset class performance was measured using the following benchmarks:

U.S. Large Cap Stocks: S&P 500 TR Index

U.S. Small & Micro Cap Stocks: Russell 2000 TR Index

Intl Dev Large Cap Stocks: MSCI EAFE GR Index

Intl Dev Small & Micro Stocks: MSCI EAFE GR Index

Emerging & Frontier Market Stocks: MSCI Emerging Markets GR Index

Global Stocks: MSCI ACWI GR Index

Private Equity: Cambridge Associates U.S. Private Equity

Venture Capital: Cambridge Associates U.S. Venture Capital

U.S. Interm-Term Muni Bonds: Bloomberg Barclays 1-10 (1-12 Yr) Muni Bond TR Index

U.S. High Yield Muni Bonds: Bloomberg Barclays High Yield Muni TR Index

U.S. Interm-Term Bonds: Bloomberg Barclays U.S. Aggregate Bond TR Index

U.S. High Yield Bonds: Bloomberg Barclays U.S. Corporate High Yield TR Index

U.S. Bank Loans: S&P/LSTA U.S. Leveraged Loan Index

Intl Developed Bonds: Bloomberg Barclays Global Aggregate ex-U.S. Index

Emerging & Frontier Market Bonds: JPMorgan EMBI Global Diversified TR Index

Public BDCs: S&P BDC Index

U.S. REITs: MSCI U.S. REIT GR Index

Ex U.S. Real Estate Securities: S&P Global Ex-U.S. Property TR Index

Private Real Estate: Cambridge Associates Real Estate

Commodity Futures: Bloomberg Commodity TR Index

Midstream Energy: Alerian MLP TR Index

Gold: LBMA Gold Price

Long-Short Equity: HFRI Equity Hedge Index

Global Macro: HFRI Macro-CTA Index

Relative Value: HFRI Relative Value Index

Closed-End Funds: S-Network Composite Closed-End TR Index

Insurance-Linked Securities: Swiss Re Global Cat Bond TR Index

Digital Assets: MVIS Crypto Compare Digital Assets 25 Index

Cash & Cash Equivalents: Bloomberg Barclays U.S. T-Bill 1-3 Month TR Index

U.S. Short-Term Muni Bonds: Bloomberg Barclays Municipal 1-3 Yr TR Index

U.S. Short-Term Bonds: Bloomberg Barclays U.S. Agg 1-3 Yr TR Index

U.S. 60/40: 60% S&P 500 TR Index 40% Bloomberg Barclays U.S. Aggregate Bond TR Index

Global 60/40: 60% MSCI ACWI GR Index 40% Bloomberg Barclays Global Aggregate Bond TR Index