We believe the equity market rally we have witnessed since the U.S. 2016 election (S&P 500 Index up 57.2%) has been due in part to capitalist influences. The rally we have seen in Q4 2019, we believe, has been driven, again in part, by a reduction in expectations President Trump will be removed from office and thus will be free to stand in the 2020 election. In our view, markets may have already nodded to a material probability that Trump could win another election. Alternatively, a 180-degree shift in policy (favoring progressivism via a Democratic president), may prompt some giveback in the capitalist premium priced into the market today.

Equity Strategy – Our equity view became more constructive during 2019 as the Federal Reserve surprisingly reversed its monetary tightening cycle (leading to equity gains that were beyond our expectations). The Fed’s apparent tactical support for the economy and the equity market is one reason we address 2020 with the same modestly-bullish view. While we would still overweight equities versus bonds in 2020, we would continually approach stocks with a more defensive mindset. This is in line with our participate and protect investment philosophy. Given how far we have come in equities over this cycle, we believe it is prudent to manage down risk. Thus, an equity focus on total return (capital appreciation and dividends) should become increasingly important as the “growth” equity outperformance fades.

Fixed Income Strategy – While fixed-income may not match equities in terms of return, we believe the asset class will continue to offer stable performance in 2020. Our view is yields could be biased lower during the year and over the intermediate-to-long-term, which should prompt investors to be more generous with their duration exposure. As we have espoused in the past, investors should no longer cling to short-duration exposure with the expectation of some sustainable interest rate increase. While most fixed-income portfolios should be focused on good core bond exposure, the market’s search for yield should maintain demand in noncore areas of the market (high-yield, emerging market debt, non-agency mortgages, bank loans). However, investors should again step carefully here. Lenders and fixed-income managers have become more careful with their risky market exposure in recent quarters and we believe most investors should as well.

Market Commentary

Politics Matter

Fundamentals do still matter, but U.S. politics should have a material influence on global markets in 2020.

Since 1950, the S&P 500 Index has averaged a 16.4% gain in the third year of a U.S. presidential term, but only 6.6% in an election year.

We are anticipating equity markets to post modest gains in 2020, driven by monetary policy support and slight earnings gains. Valuations are not as compelling as they were a year ago

Lions and Tigers and Politicians...Oh My

Not that the job of capital market forecasting and portfolio management is easy by any stretch, but 2020 sets up as an environment that is the most difficult to call of any in recent memory. In a typical year, the necessary forecasting recipe should be economic fundamentals, earnings, monetary policy, and a dose of market sentiment. The new year requires all of that and perhaps a political prediction acumen that frankly few possess. Coupling the normal political prognostication difficulty with the unprecedented, bifurcated nature of the U.S. election landscape and you get a jungle of varied, potential outcomes. Despite the additional complexity, we have the job of guiding investors on what we believe is the best way to think about capital allocation in 2020. That indeed is what we will do.

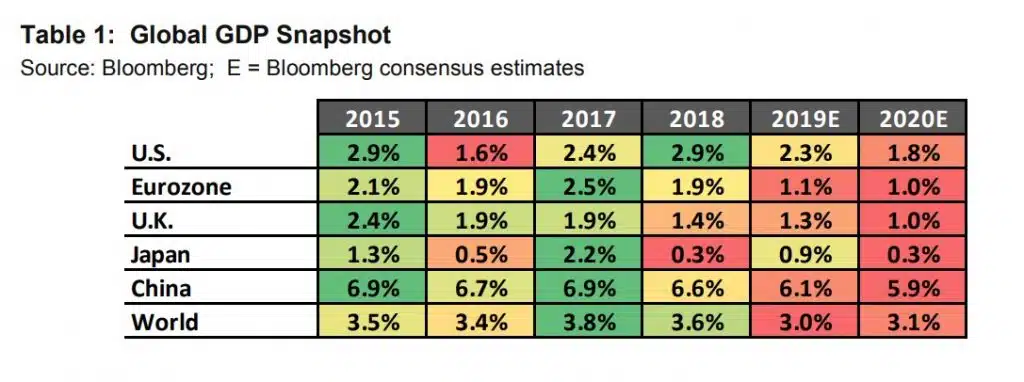

Global economic growth should continue to decelerate, although the support of central banks and an opportunity for a modest manufacturing recovery should offset recession risk.

Economy/Earnings – Fundamentally, we believe 2020 has relatively little excitement to offer. Economic forecasters have taken down GDP forecasts in many corners of the world, although recession probabilities remain contained. The projected weaker economic foundation, however, should raise some questions about the potential impact on corporate earnings. In that regard, we are not quite as sanguine as the consensus; which is calling for 11.5% year-over-year growth in 2020 S&P 500 earnings. We believe some ease of U.S./China trade tensions and a recovery in manufacturing activity could translate into similar 2020 earnings growth to that estimated for 2019 (4%). A decline in corporate profit margins through 2019 has been a concern and further deterioration may occur as rising labor costs could negatively impact the bottom line. Meanwhile, a slowing economy, U.S. political uncertainty, and fewer stock buybacks anticipated for 2020 should, in our view, prevent earnings from reaching lofty, consensus expectations.

Although profit growth is slowing and margins compressing, earnings trends have been a notable justifier of equity prices since the financial crisis. As Figure 2 shows, prices have moved in near lock-step with earnings growth. We anticipate modest earnings gains, rather than multiple expansion, could account for most of the S&P 500 Index ascension in 2020. We are forecasting a 6% gain for the benchmark index in the new year. Some reversion to the mean should occur following high-flying 2019 gains, and history indicates that U.S. presidential election year is the second worst performing period over the four year cycle. Thus, political tension, slowing economies, and sluggish earnings should prove to be formidable deterrents against more substantial equity gains in 2020.

The correlation between price and earnings trends lends credence to equity gains.

The gray shaded area highlights S&P Dow Jones consensus earnings estimates and a hypothetical index price gain equivalent to a 6% rise (our forecast) for the S&P 500 Index in 2020. Price gain measured as of the index price on 12/17/2019.

More “tactical” monetary policy from global central banks has elongated this business cycle and has aided risky asset prices.

Monetary Policy – A main driver for equities in 2019; central bank liquidity, could again provide a modest tailwind in 2020. Central bank balance sheet growth has been highly correlated to equity prices over the last decade. As central banks became more dovish in early 2019, stocks recovered strongly from their Q4 2018 swoon. We believe the Federal Reserve could keep its policy rate unchanged in 2020, but Chairman Powell has been quietly overseeing renewed growth in the Fed’s balance sheet. We believe this could continue. Further, the ECB, the Bank of Japan, the Peoples Bank of China and other central banks may also engage in additional policy accommodation. In aggregate, accommodative policy rates and central bank asset growth should again be a supporting factor for global equity prices.

Equity valuations are not a compelling factor at the moment.

It should be tougher for equity markets to post gains in 2020.

Valuations – A reason to stop short of inferring 2019 gains will be similarly repeated in 2020 is that valuations are no longer “constructive”; as they were in late 2018 and early 2019. Forward price-to earnings ratios, across the globe’s major indices, are again approaching cyclical highs (see Figure 4 on page 5). Concern that forward earnings estimates may have to be revised down only adds to a note of caution, in our view. Interestingly, price-to-book figures are also at cyclical highs for the S&P 500 Index, but not for MSCI EAFE and MSCI Emerging Markets, implying some relative opportunity in non-domestic indices. While this may help make a case for more favorable foreign equity allocations, recall that superior corporate profit margins and better corporate innovation may be reasons U.S. equities have indeed outperformed in recent years. We still favor U.S. equities, despite some valuation argument for foreign equity exposure. In our view, a catalyst for a foreign stock overweight is not apparent at this time. Finally, while valuations have richened in recent quarters, investors should note that historically high valuations have been better-supported during periods of low inflation and low interest rates.

We believe investors should shelve the notion that interest rates will sustainably rise over the intermediate to long term

Without fiscal reform in the U.S., we believe rates are biased lower over the foreseeable future.

Base Case Global Projections for 2020

Data points above the dotted line equates to a current forward PE that is above the rolling average over the time period shown.

The dichotomy of political options today should compel rational investors to take less risk in 2020.

Capitalism vs. Progressivism has been a time-honored political debate. As it is now, this debate was particularly onerous in the 1930’s.

Politics – We make a point to not delve too deeply into politics and we certainly remain apolitical in our assessment of macro economic conditions. However, the 2020 U.S. election sets up as a unique circumstance with the potential for very divergent policy outcomes, based on presidential and congressional results. We would be lax if we did not weigh-in with how we believe the market could react to the results.

First of all, what we have been witnessing politically is a time-honored battle between capitalism and progressivism, exacerbated by the financial crisis conditions of 10-12 years ago. A similar political battle occurred after the Great Depression. This time, the argument is intensified by discussion over whether a wave of cross-border trade activity (globalism) has been a net positive for national interests. For the record we believe it has, although trade policy has likely not found its equilibrium. The direction of these conversations, and the interim winners and losers politically, are clearly expected to impact capital market dynamics. As a result, it demands our attention.

We approach 2020 favoring equities, but only modestly. The fundamental and political environment, in our view, demands that limited risk should be taken.

We believe the equity market rally we have witnessed since the U.S. 2016 election (S&P 500 Index up 57.2%) has been due in part to capitalist influences. The rally we have seen in Q4 2019, we believe, has been driven, again in part, by a reduction in expectations President Trump will be removed from office and thus will be free to stand in the 2020 election. In our view, markets may have already nodded to a material probability that Trump could win another election. Alternatively, a 180-degree shift in policy (favoring progressivism via a Democratic president), may prompt some giveback in the capitalist premium priced into the market today.

Equity Strategy – Our equity view became more constructive during 2019 as the Federal Reserve surprisingly reversed its monetary tightening cycle (leading to equity gains that were beyond our expectations). The Fed’s apparent tactical support for the economy and the equity market is one reason we address 2020 with the same modestly-bullish view. While we would still overweight equities versus bonds in 2020, we would continually approach stocks with a more defensive mindset. This is in line with our participate and protect investment philosophy. Given how far we have come in equities over this cycle, we believe it is prudent to manage down risk. Thus, an equity focus on total return (capital appreciation and dividends) should become increasingly important as the “growth” equity outperformance fades.

Fixed Income Strategy – While fixed-income may not match equities in terms of return, we believe the asset class will continue to offer stable performance in 2020. Our view is yields could be biased lower during the year and over the intermediate-to-long-term, which should prompt investors to be more generous with their duration exposure. As we have espoused in the past, investors should no longer cling to short-duration exposure with the expectation of some sustainable interest rate increase. While most fixed-income portfolios should be focused on good core bond exposure, the market’s search for yield should maintain demand in noncore areas of the market (high-yield, emerging market debt, non-agency mortgages, bank loans). However, investors should again step carefully here. Lenders and fixed-income managers have become more careful with their risky market exposure in recent quarters and we believe most investors should as well.

In our view, the 10yr yield could stay largely within established ranges. The shaded range (1.35% - 2%) may be the most significant. While we could see the yield float above 2% for a period, we believe there is a substantive probability that new lows are attained over the longer term.

Risks

Investors should be aware of the risks associated with all portfolio strategies, and variable market conditions. Monetary policy changes, military activity abroad, the level and change in market interest rates, corporate earnings, domestic and foreign governmental policies, global economic data, and other geopolitical events can have a substantial effect on portfolio performance, our macroeconomic theories, and the effectiveness of strategic and tactical portfolio approaches.

Share it :

Disclaimer

Magnus Financial Group LLC (“Magnus”) did not produce and bears no responsibility for any part of this report whatsoever, including but not limited to any microeconomic views, inaccuracies or any errors or omissions. Research and data used in the presentation have come from third-party sources that Magnus has not independently verified presentation and the opinions expressed are not by Magnus or its employees and are current only as of the time made and are subject to change without notice.

This report may include estimates, projections or other forward-looking statements, however, due to numerous factors, actual events may differ substantially from those presented. The graphs and tables making up this report have been based on unaudited, third-party data and performance information provided to us by one or more commercial databases. Except for the historical information contained in this report, certain matters are forward looking statements or projections that are dependent upon risks and uncertainties, including but not limited to factors and considerations such as general market volatility, global economic risk, geopolitical risk, currency risk and other country-specific factors, fiscal and monetary policy, the level of interest rates, security-specific risks, and historical market segment or sector performance relationships as they relate to the business and economic cycle.

Additionally, please be aware that past performance is not a guide to the future performance of any manager or strategy, and that the performance results and historical information provided displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Therefore, it should not be inferred that these results are indicative of the future performance of any strategy, index, fund, manager or group of managers. Index benchmarks contained in this report are provided so that performance can be compared with the performance of well-known and widely recognized indices. Index results assume the re-investment of all dividends and interest and do not reflect any management fees, transaction costs or expenses.

The information provided is not intended to be, and should not be construed as, investment, legal or tax advice nor should such information contained herein be construed as a recommendation or advice to purchase or sell any security, investment, or portfolio allocation. An investor should consult with their financial advisor to determine the appropriate investment strategies and investment vehicles. Investment decisions should be made based on the investor’s specific financial needs and objectives, goals, time horizon and risk tolerance. This presentation makes no implied or express recommendations concerning the way any client’s accounts should or would be handled, as appropriate investment decisions depend upon the client’s specific investment objectives.

Investment advisory services offered through Magnus; securities offered through third party custodial relationships. More information about Magnus can be found on its Form ADV at www.adviserinfo.sec.gov.

Terms of Use

Definitions

Asset class performance was measured using the following benchmarks: U.S. Large Cap Stocks: S&P 500 TR Index; U.S. Small & Micro Cap: Russell 2000 TR Index; Intl Dev Large Cap Stocks: MSCI EAFE GR Index; Emerging & Frontier Market Stocks: MSCI Emerging Markets GR Index; U.S. Intermediate-Term Muni Bonds: Bloomberg Barclays 1-10 (1-12 Yr) Muni Bond TR Index; U.S. Intermediate-Term Bonds: Bloomberg Barclays U.S. Aggregate Bond TR Index; U.S. High Yield Bonds: Bloomberg Barclays U.S. Corporate High Yield TR Index; U.S. Bank Loans: S&P/LSTA U.S. Leveraged Loan Index; Intl Developed Bonds: Bloomberg Barclays Global Aggregate ex-U.S. Index; Emerging & Frontier Market Bonds: JPMorgan EMBI Global Diversified TR Index; U.S. REITs: MSCI U.S. REIT GR Index, Ex U.S. Real Estate Securities: S&P Global Ex-U.S. Property TR Index; Commodity Futures: Bloomberg Commodity TR Index; Midstream Energy: Alerian MLP TR Index; Gold: LBMA Gold Price, U.S. 60/40: 60% S&P 500 TR Index; 40% Bloomberg Barclays U.S. Aggregate Bond TR Index; Global 60/40: 60% MSCI ACWI GR Index; 40% Bloomberg Barclays Global Aggregate Bond TR Index.