Even the best-run businesses aren’t fully immune to the impacts of market and economic conditions. These widespread downturns tend to stem from factors largely outside of individual organizations’ control, having industry-wide, national or even global impacts.

However, there are things leaders can do to better protect their company’s finances during tough times. Below, 15 members of Forbes Finance Council share their best tips for weathering a recession—and coming through stronger on the other side.

1. Be Conservative In Downturns

At the current stage of the cycle, it does make sense for business leaders to be conservative, conserve cash or keep a large cash buffer on their balance sheet while patiently waiting for investment and acquisition opportunities that certainly will emerge. Also, hire globally. COVID-19 has taught us all to do this well. – Jaideep Singh, FlyFin AI, Inc.

2. Keep An Emergency High-Yield Savings Account

I keep an emergency savings account for the business. It is invested in a high-yield money market account. My staff will always review our expenses on a quarterly basis and make sure we are not overspending on business items. But the business is a part of a profit-sharing arrangement, in which it receives a savings bonus. It is accounted for after all employee raises, bonuses, etc. are issued. – Keith Gebert, RightBridge Financial Group

3. Finance New Equipment And Software

Equipment leases are a relatively easy type of financing to get because the equipment you buy collateralizes the loan. So even younger companies can get them with a personal guarantee. I would always finance new equipment and software rather than pay for it in cash. However, don’t use your line of credit for purchases, as that is your backup cash to get you through downtimes. – Joseph DiSanto, Play Louder

4. Monitor Cash Flow And Sources Of Capital

Keep a constant eye on cash flow and the sources of capital available to you at any given time. Today’s finance chiefs need more frequent, more granular cash flow statements and forecasts than ever. Many who used to forecast monthly or quarterly are now doing it weekly, even daily. Strong leadership and business models are key, but only if you can fund the business. – Don Mal, Fluence Technologies

5. Diversify Your Revenue Stream

Diversifying your revenue stream can be a key component to reducing your company’s risk of recession. Our organization started life as a real estate developer. When the 2008 crash hit, development work came to a standstill. Because we had diversified into management and leasing, we survived an economic event that had a devastating impact on some of our undiversified competition. – Katherine Jackson, Bayer Properties, LLC

6. Create Short-Term Micro Metrics

Create short-term micro metrics to keep a good pulse and have the ability to react quickly. We don’t look at this micro level of data all the time, but we have them for when things start to dip. An example is we look weekly at software conversion projects sold. If it dips, we can see the number of plans created, consultations held, leads generated, then dollars spent towards this service. – Marjorie Adams, Fourlane

7. Maintain Your Cash Forecast

We advise a three-pronged approach to protecting business finances. First, maintaining a rolling 13-month cash forecast keeps business owners tuned in to cash availability expectations. Second, routinely updating the forecast for economic expectations and upside and downside scenarios provides more precision. Finally, obtaining a line of credit before the business requires one is very important. – Jennifer Eubanks, CPA Department

8. Secure Debt When The Market Is Easy

Secure debt now when the market is easy and lenders are generous—it should be a covenant-lite loan. Debt comes in all flavors and most likely a company can find the right structure and flavor for its business size, profile and stage. Create a financial forecast or budget and monitor cash burn on a monthly basis. Monitor pipeline and sales traction on a weekly basis. – Jay Jung, Embarc Advisors

9. Develop An Enterprise Risk-Management Program

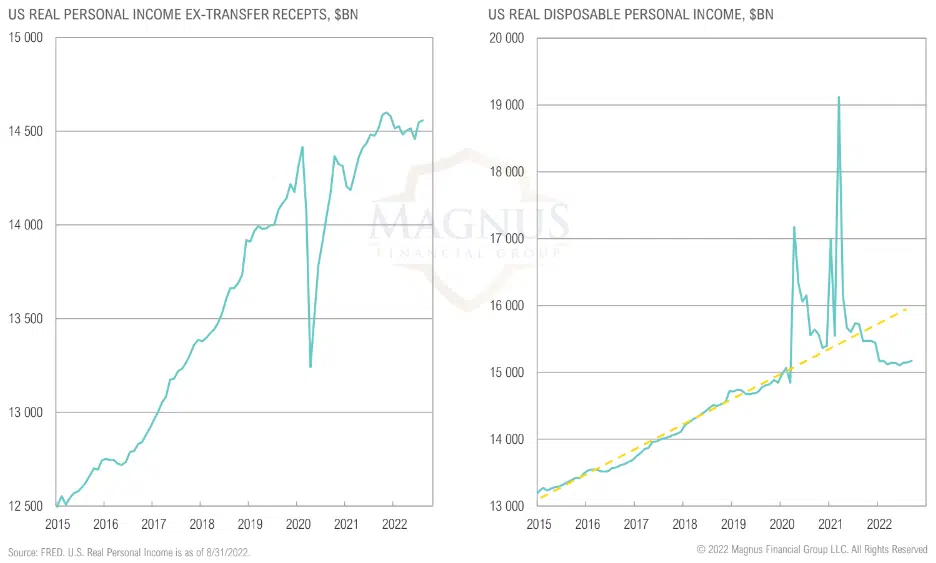

A tactical consideration could be to develop an enterprise risk management program. These alternative risk solutions can be secured through third-party insurance carriers or created as a private insurance subsidiary. As a sub, deductible premiums paid from the enterprise create a claims reserve in the subsidiary that can help offset a variety of qualified risks which may arise in a recession. – Michael S. Schwartz, Magnus Financial Group LLC

10. Shift Your Focus To The Balance Sheet

It can be difficult to know the changing tides of the economy and make plans before a recession is upon you. However, the most critical aspect that business leaders need to take to weather the storm is to shift focus and stay flexible. What that means specifically is that the financial and operational focus of the company needs to shift from a P&L perspective to a balance sheet perspective. – Patrick Rood, Rood Financial Services

11. Keep Strong Cash Reserve

The key to prospering when market conditions are challenging is to maintain strong cash reserves. A robust balance sheet positions the business to not only have sufficient finances when conditions require greater resources but also to invest in unique growth opportunities that surface by virtue of the economically-stressed environment. This turns an otherwise tough time into an abounding win. – Greg Bassuk, AXS Investments

12. Review Numbers Regularly

Company leaders, regardless of the success of their business, cannot accurately forecast the ebbs and flows of the economy. That is why it is crucial that they continually review staffing, variable expenses and cash flow to make sure that these areas have not gotten bloated in good times. – Mark Palmerino, CCR Wealth Management

13. Rate Yourself Against The Competition

Always rate yourselves against your competition, making sure you have clear advantages. If you know who is weak and likely to struggle in a recession, and if you position yourself smartly, you will separate yourself—whether it be recruiting talent, acquiring other companies in the industry or doubling down on marketing or other growth pursuits. – Brian Slipka, True North Equity Partners

14. Monitor Your Customers’ Financial Health

Make sure you never get over your skis in open accounts receivable. Having less money owed you gives you the flexibility to give credit to great customers when they need it. – Aaron Spool, Eventus Advisory Group, LLC