SUMMARY

In the normal recession, unemployment goes up, delinquencies go up, charge-offs go up, home prices go down, none of that’s true here…Savings are up, incomes are up, home prices are up…So it’s just very peculiar times.

– Jamie Dimon, JPMorgan Chase CEO, July 2020

Q2, 2020 Market Review

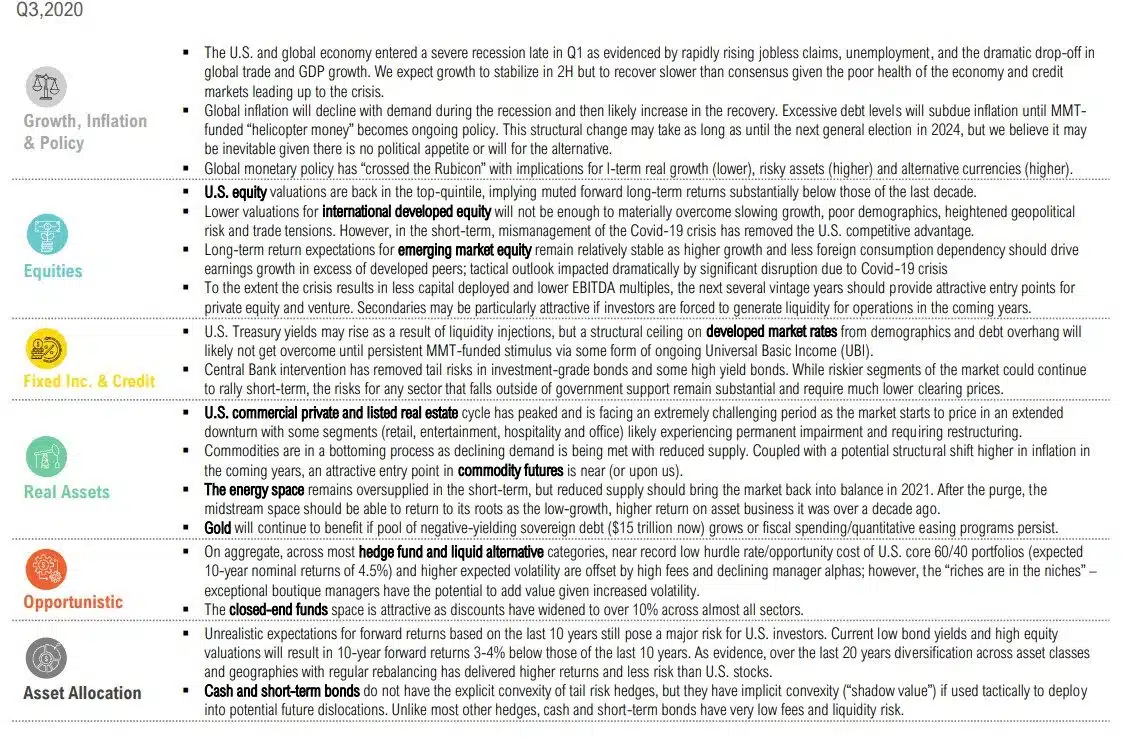

Market Outlook Summary

GROWTH, INFLATION & POLICY

It is very likely that this year the global economy will experience its worst recession since the Great Depression, surpassing that seen during the global financial crisis a decade ago… I think it makes a difference that there are lenders of last resort, that monetary policy is proactively able to come in and ensure enough liquidity in markets, that fiscal policy is able to play a major role in supporting firms and households.

– Gita Gopinath, IMF Chief Economist, April 2020

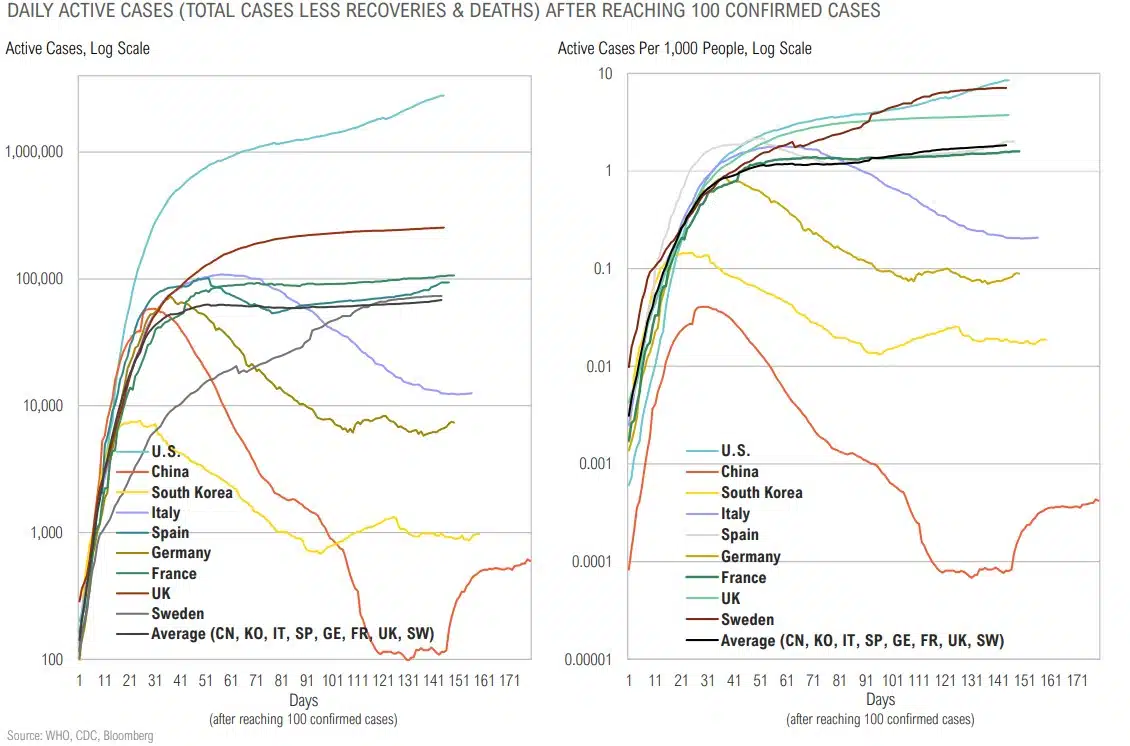

Active Cases Remain Elevated in Many Countries

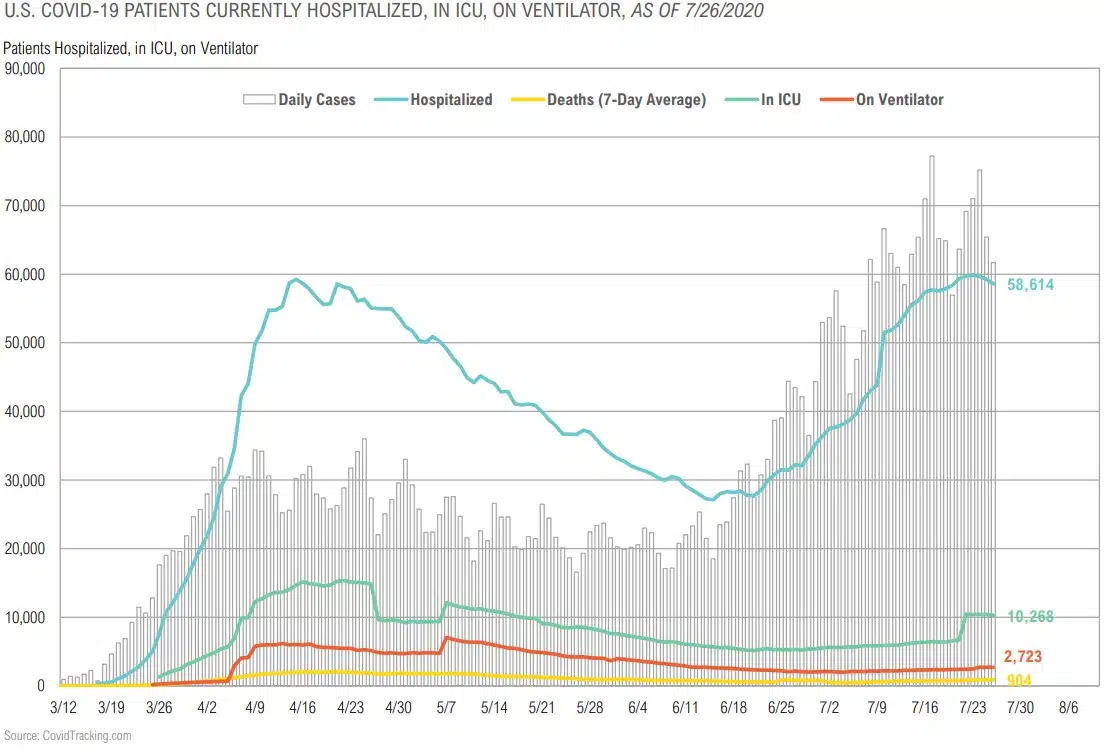

Surge in Cases & Hospitalizations Leading to Rollbacks

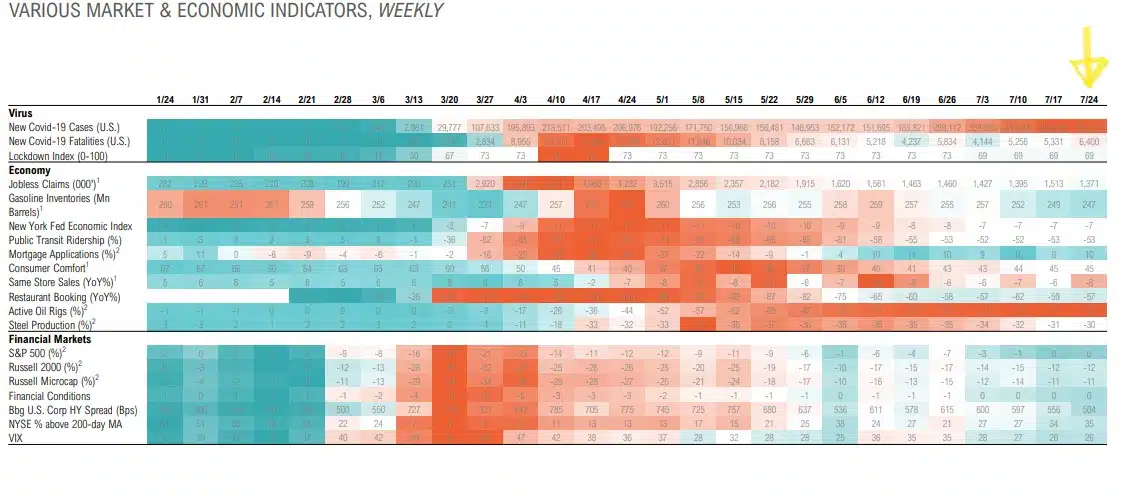

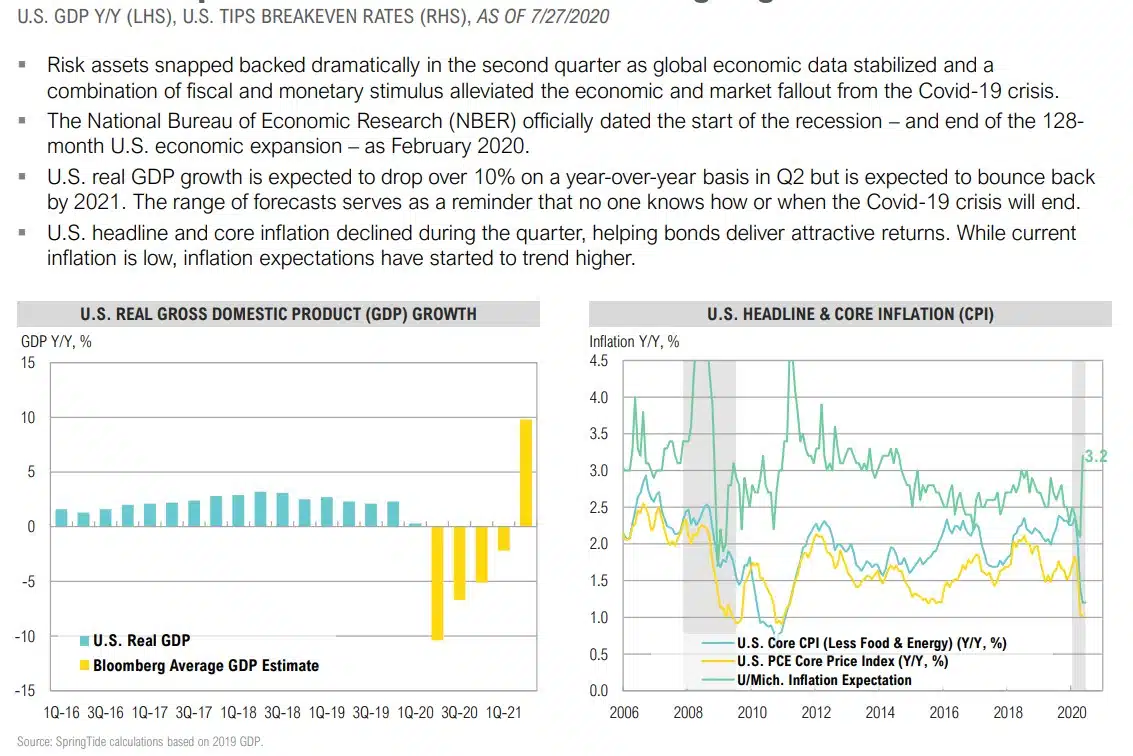

Tracking the Recovery

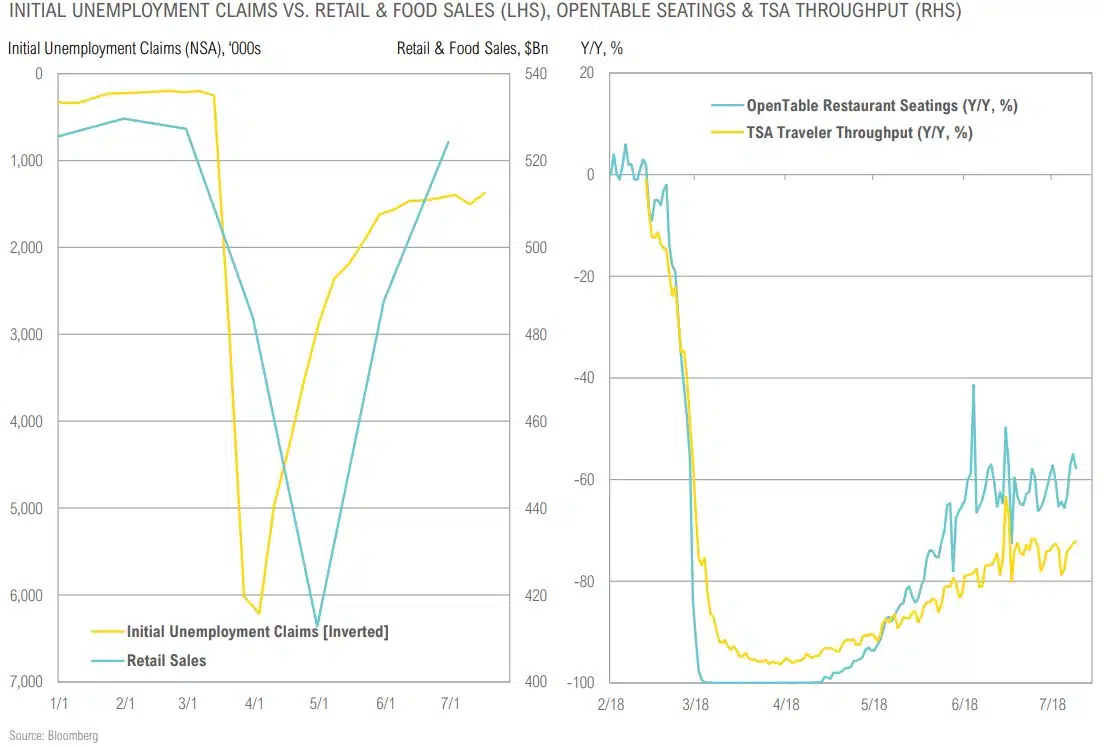

A “V” in Consumption, But Not in Activity

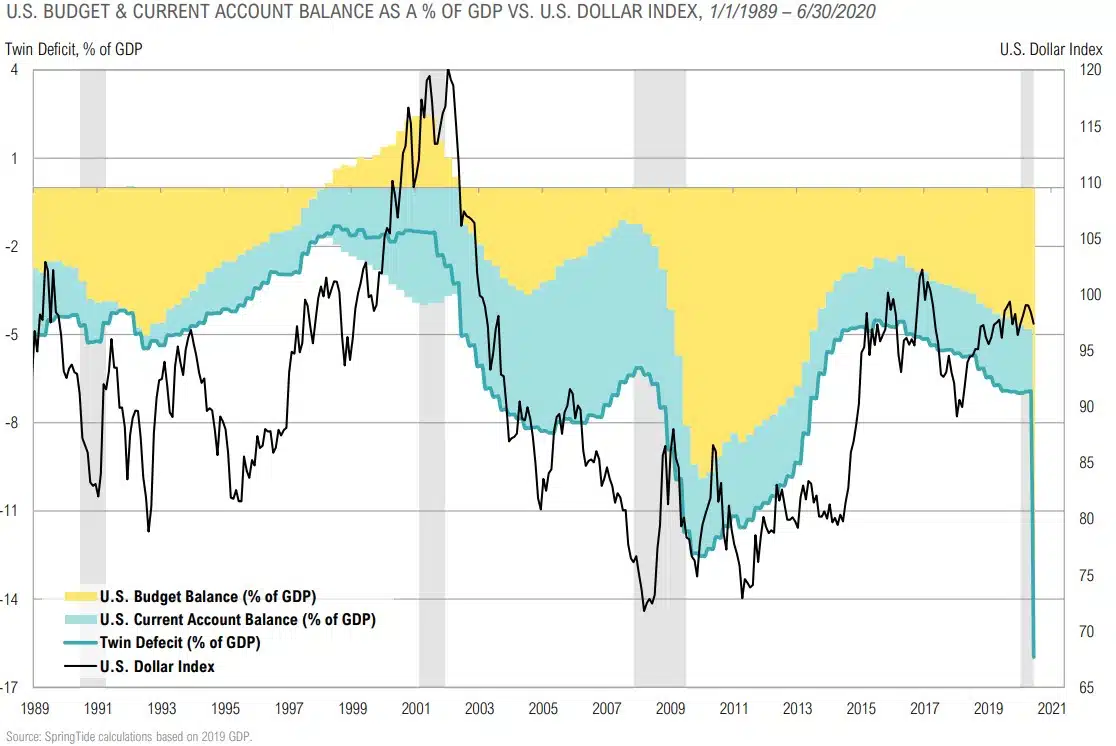

Growing Twin Deficit Will Be a Headwind for the Dollar

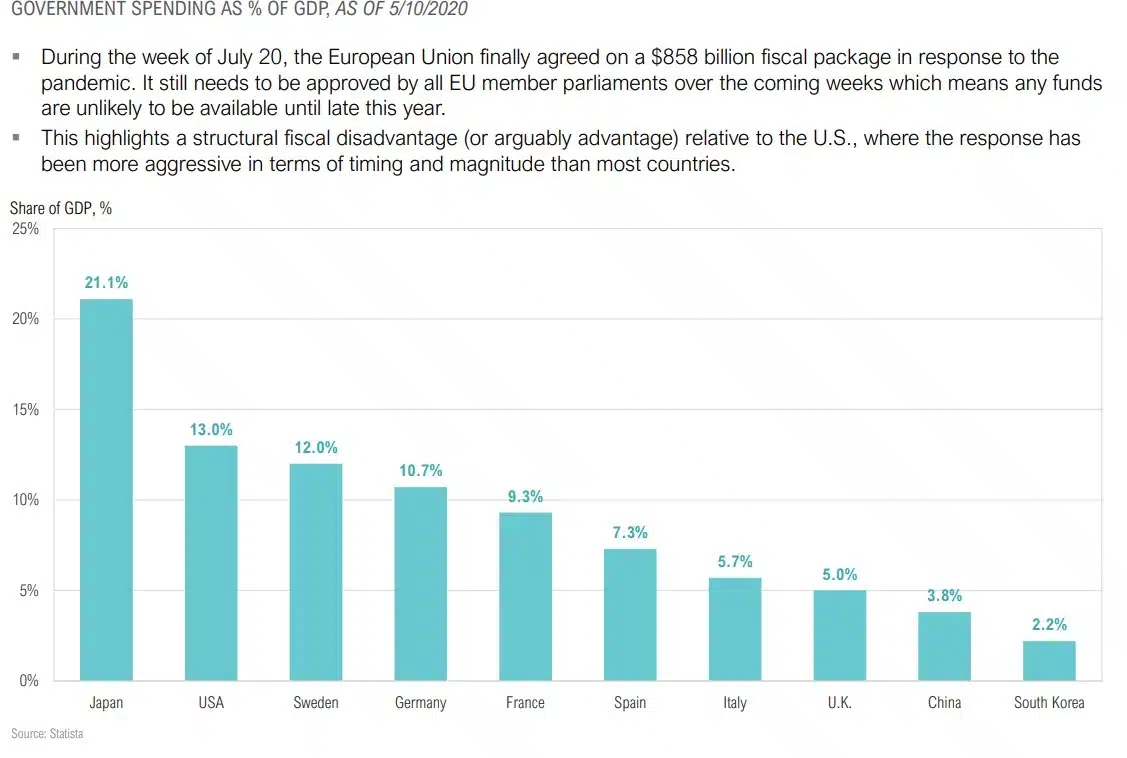

Global Fiscal Policy Response to COVID-19

Inflation Expectations are Low but Trending Higher

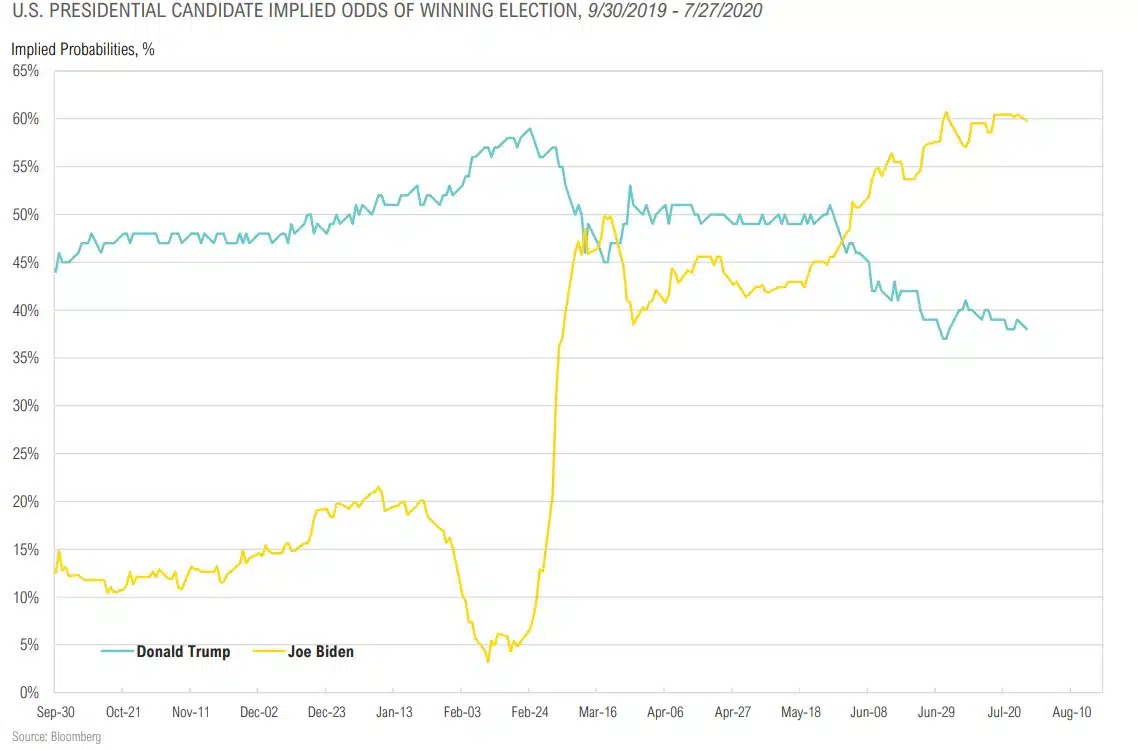

Who Will Win the 2020 U.S. Presidential Election

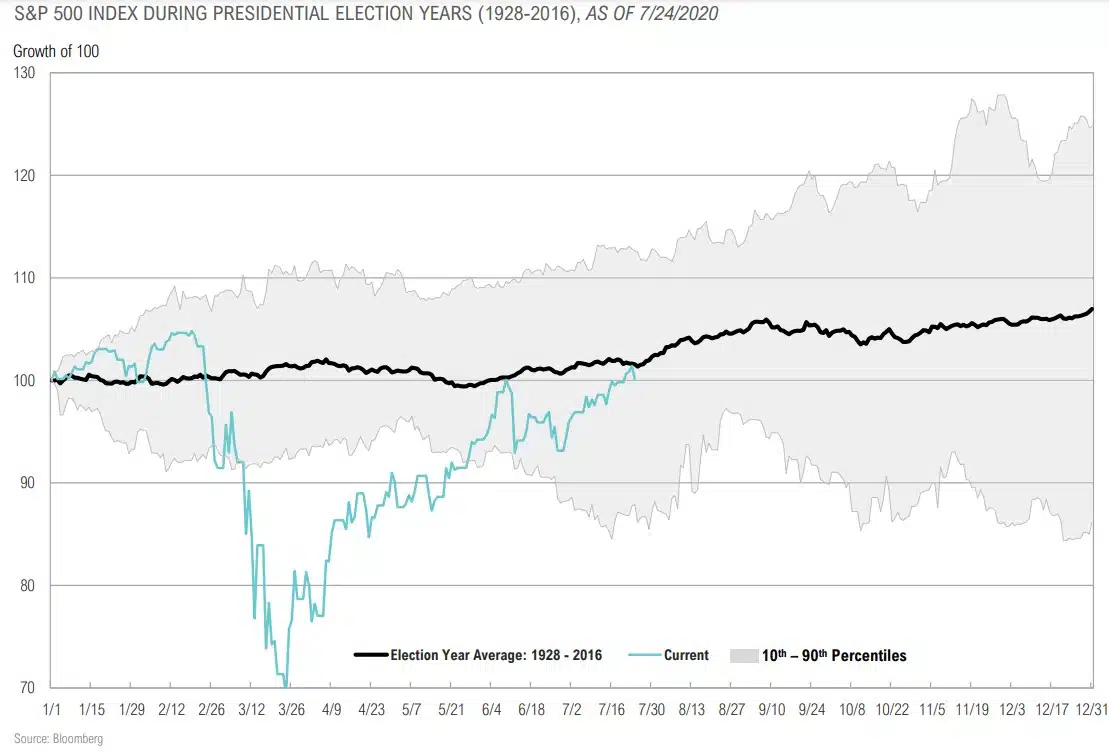

S&P 500 During Presidential Election Years

EQUITY

You know… they’re bolstering the stock market. Ok, there’s a floor to the stock market. Everybody knows it’s not going below a certain place.

– Nancy Pelosi, House Speaker, July 21, 2020

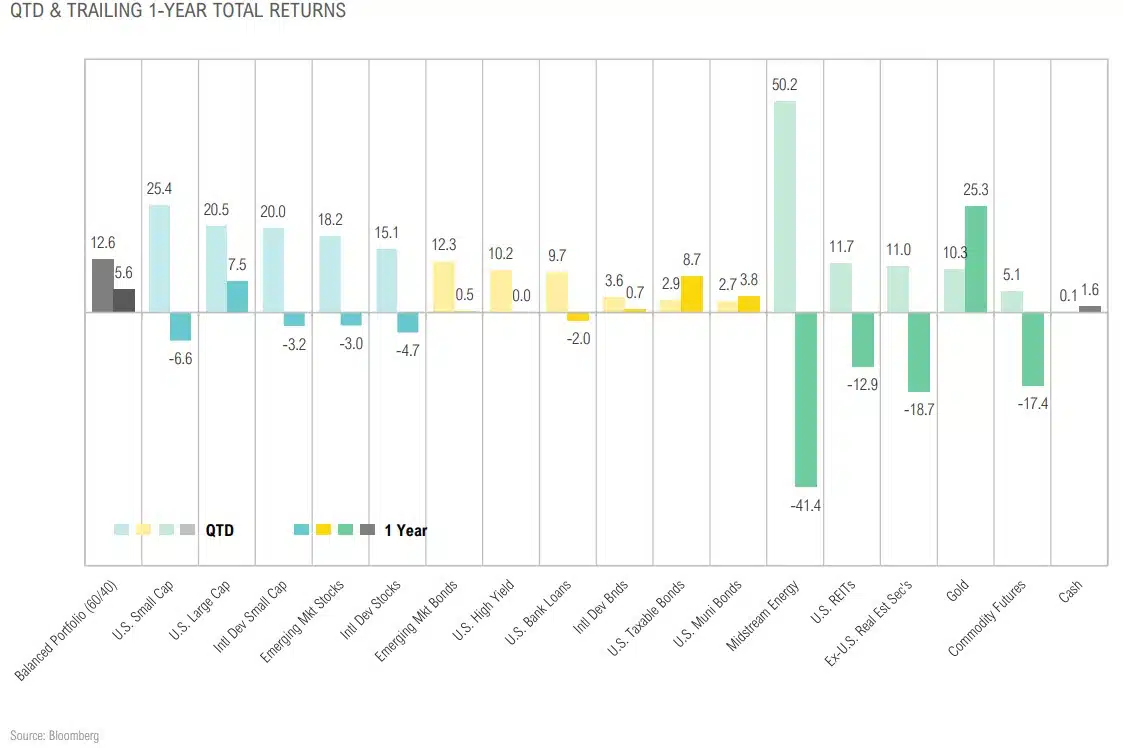

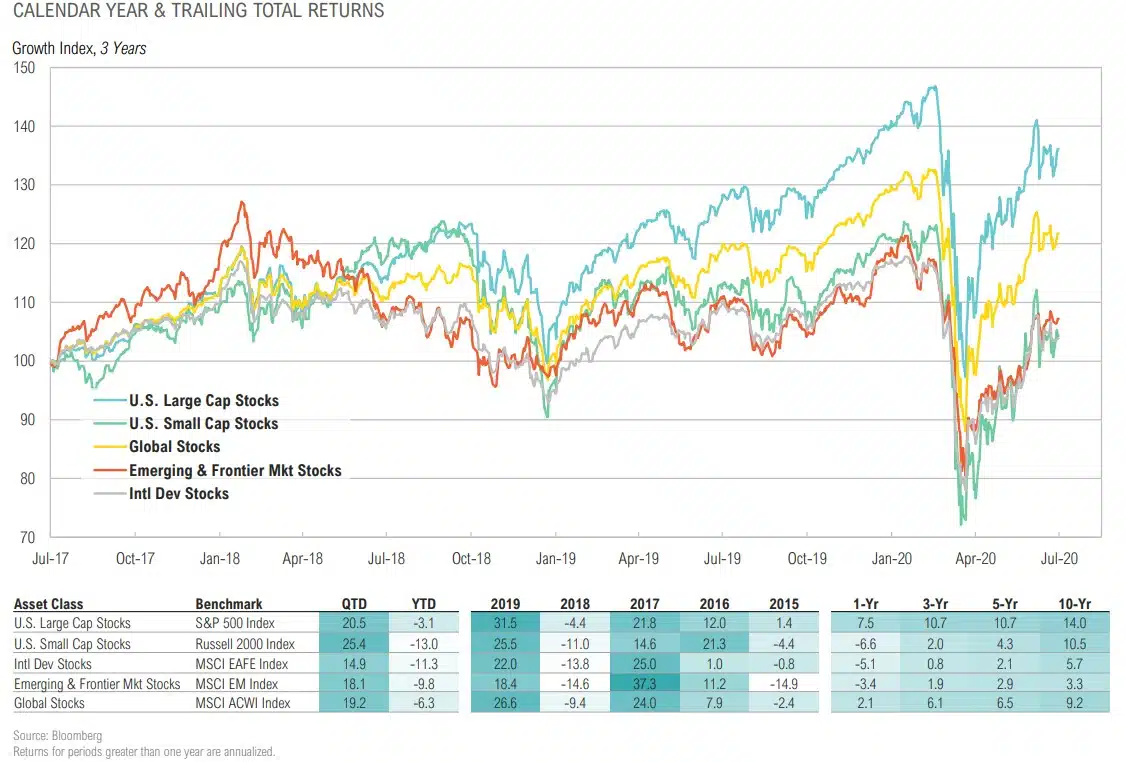

Equity Returns

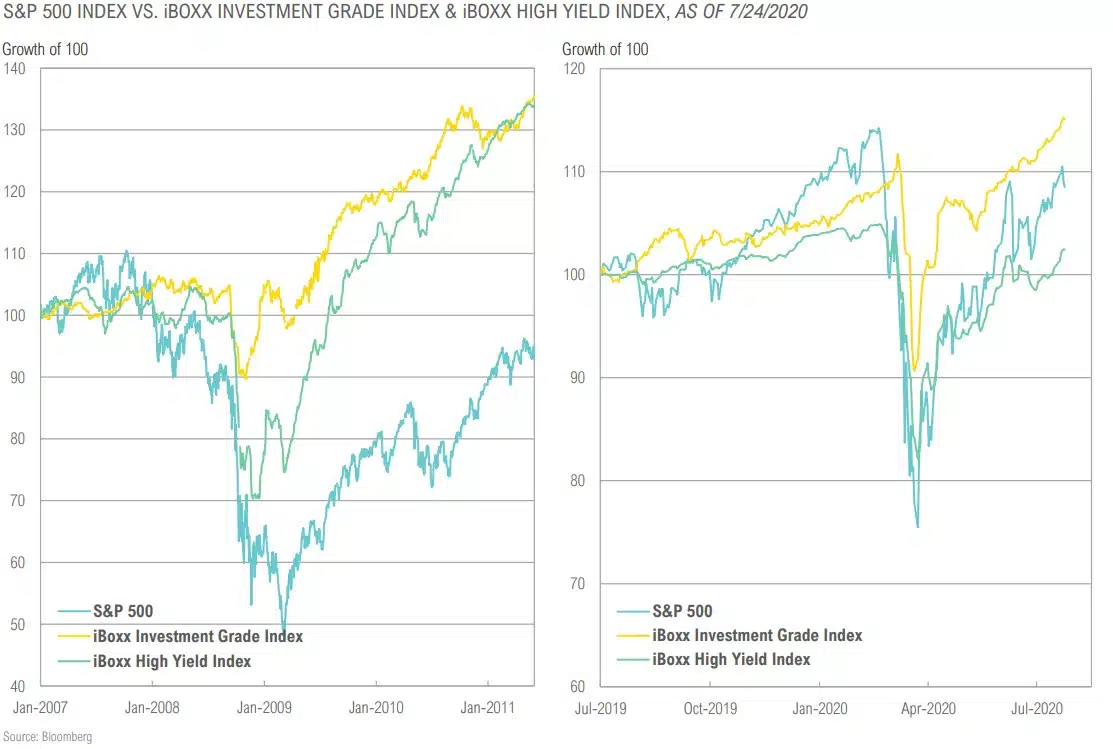

Coronavirus Crisis vs. Major Bear Markets of History

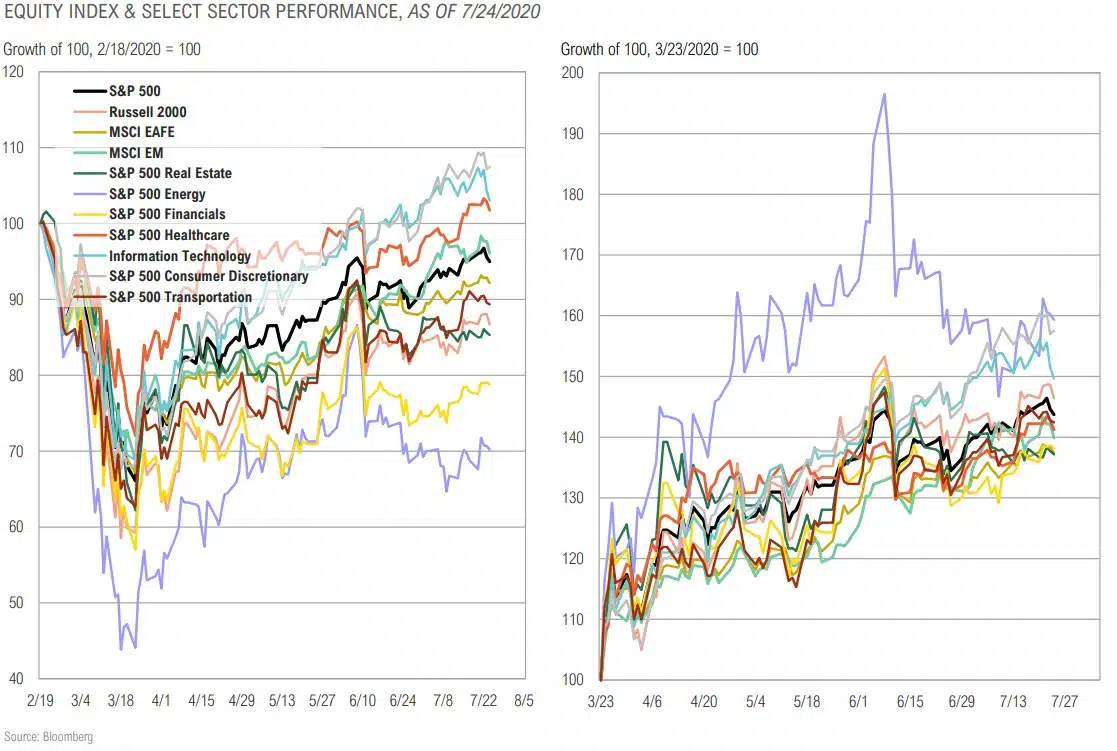

Equity Internals: Decline & Rally

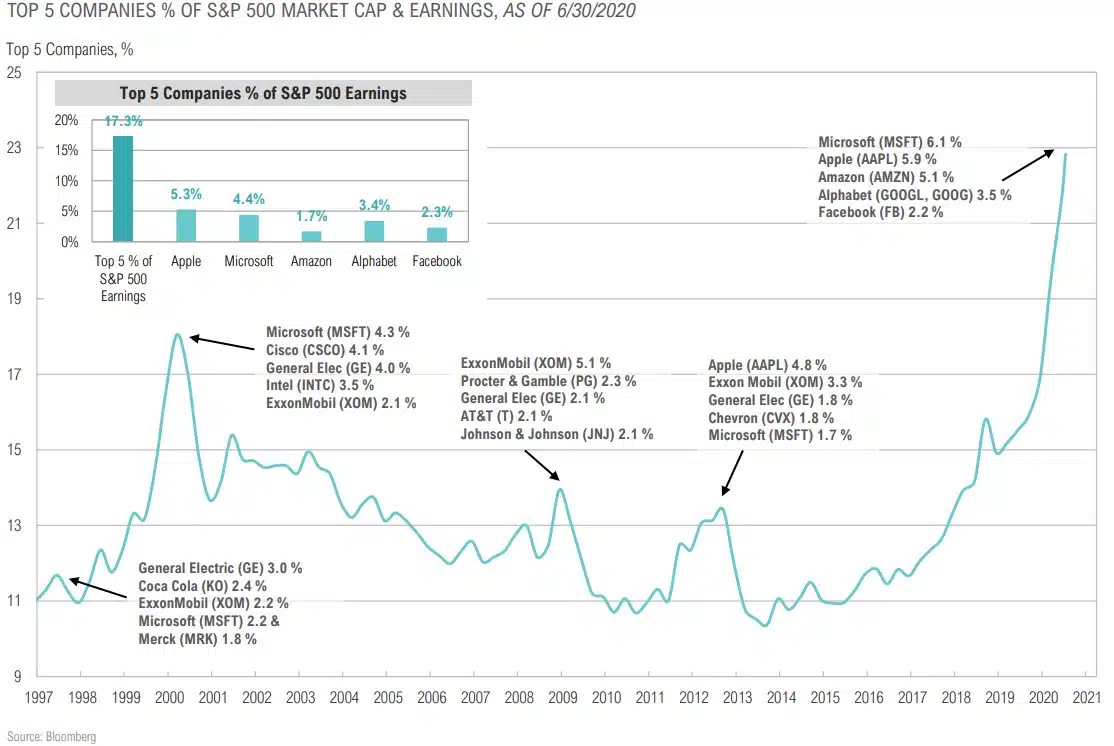

Winner Take All Markets May Be Around for a While

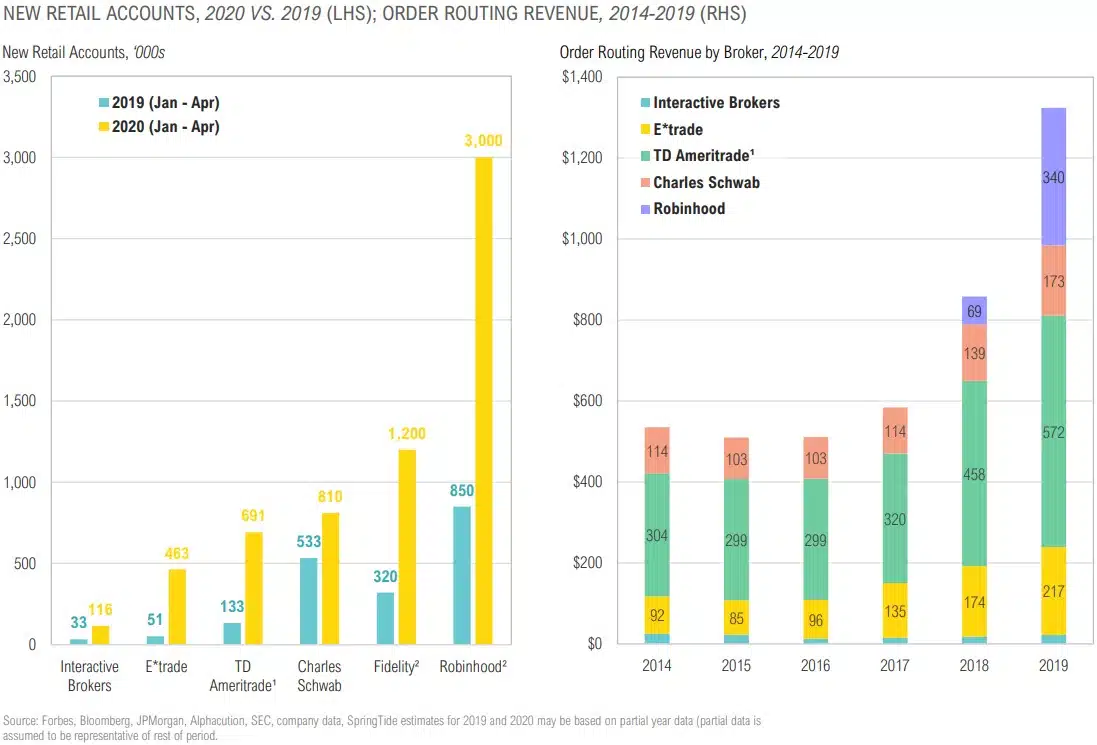

The Rise of Retail Traders

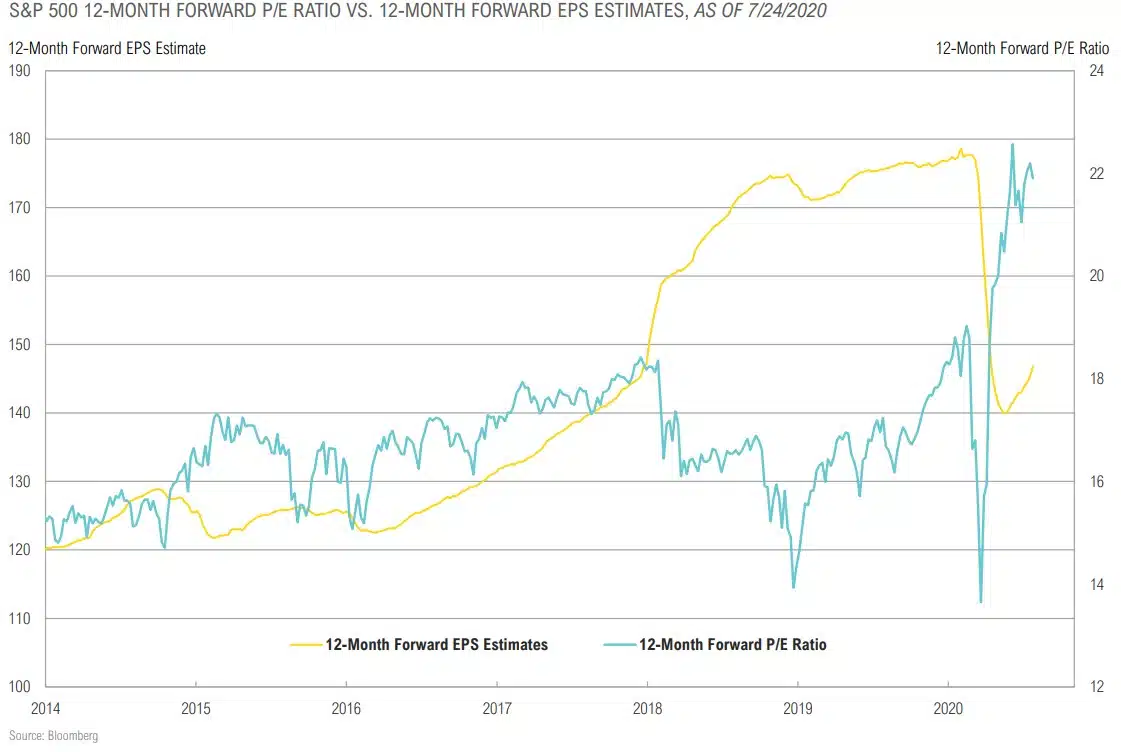

U.S. Corporate Earnings Expectations

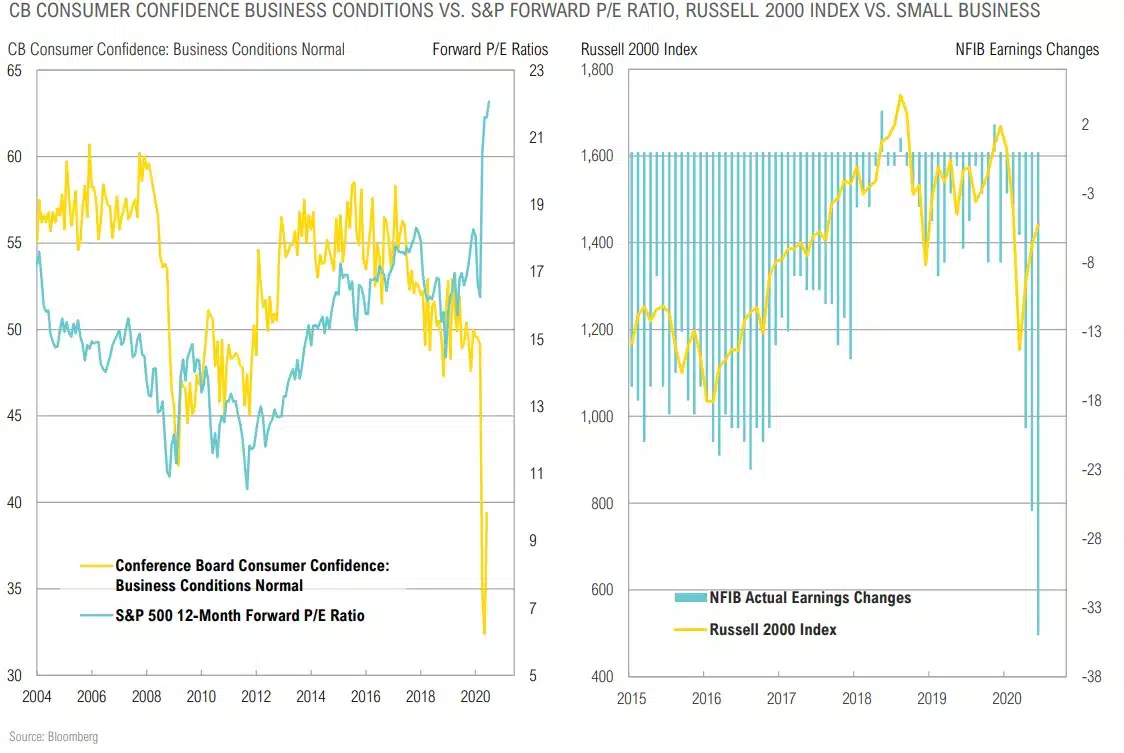

Wall Street vs. Main Street

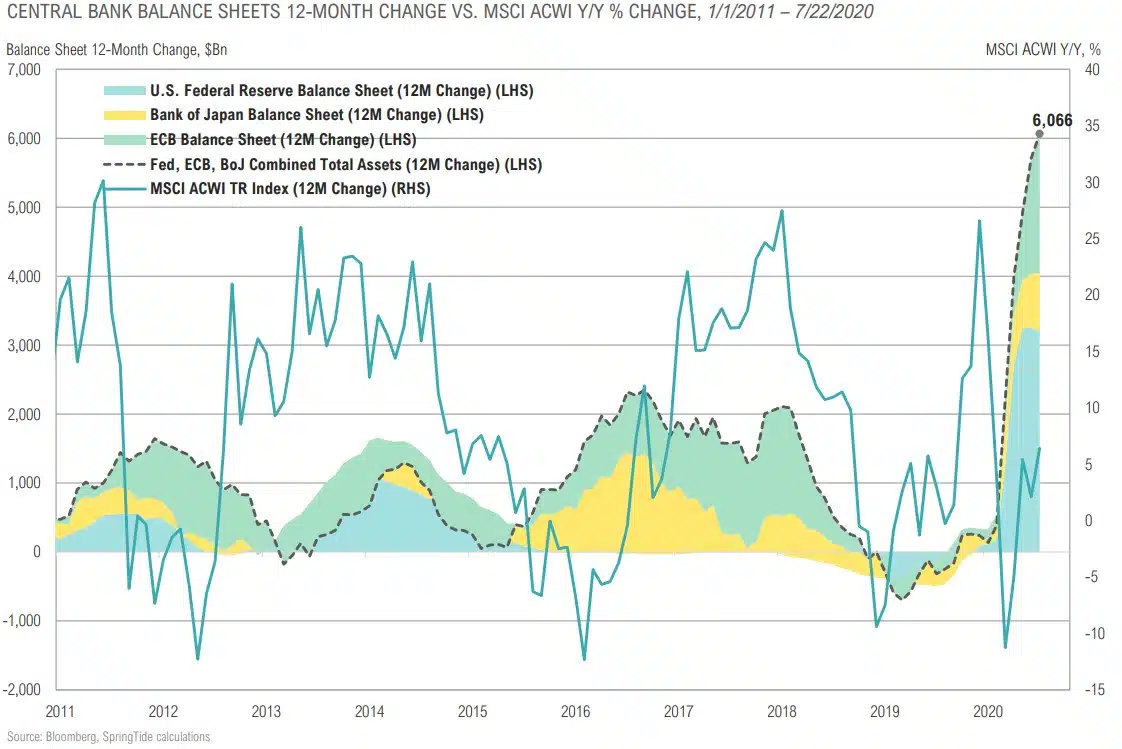

Central Bank “BS” and Global Stocks

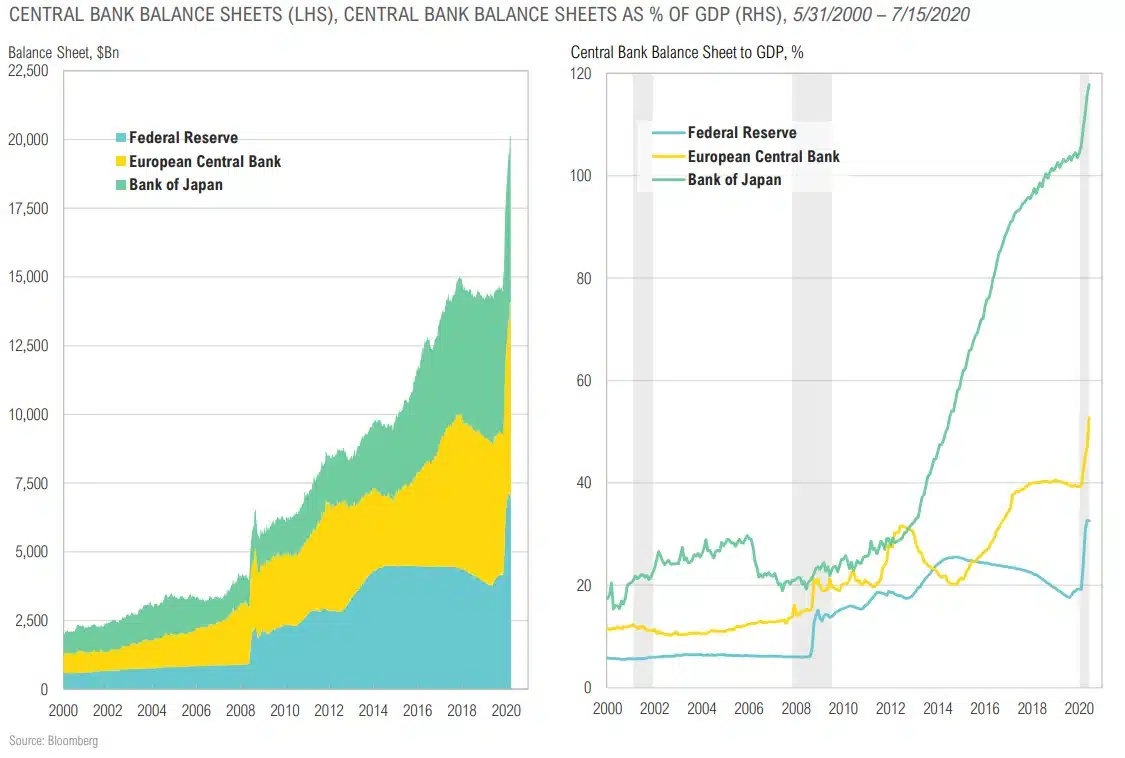

Fed Can Provide More Stimulus Relative to Other Central Banks

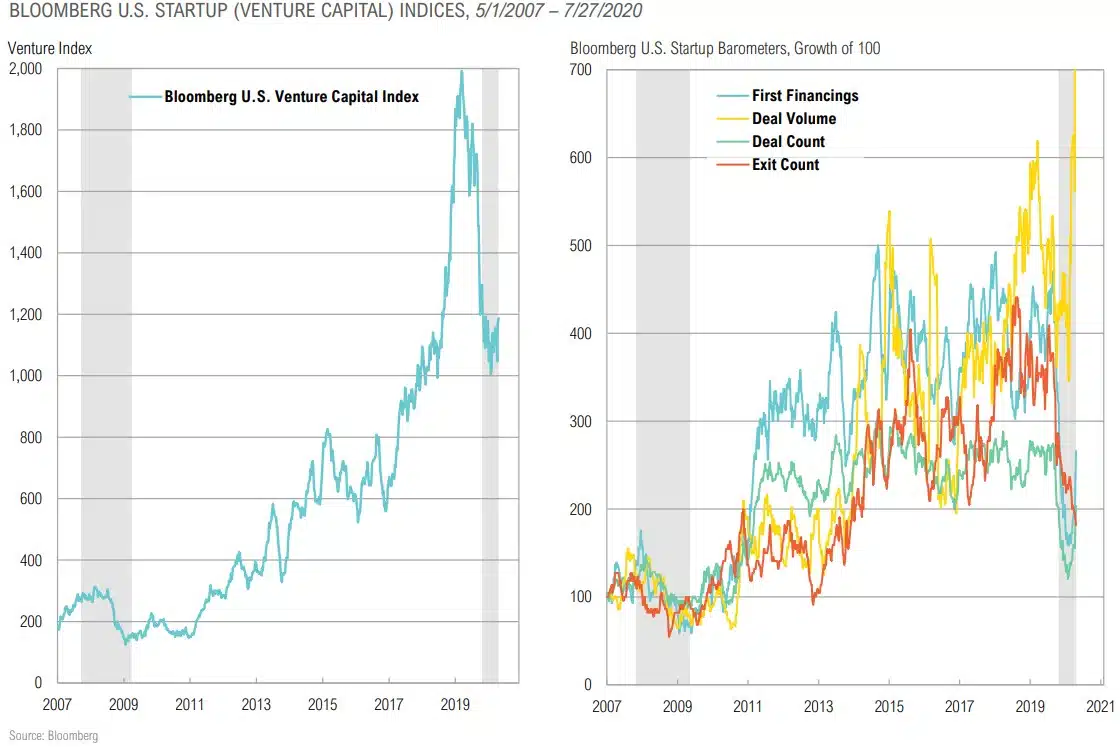

Venture Activity Cut in Half From Peak

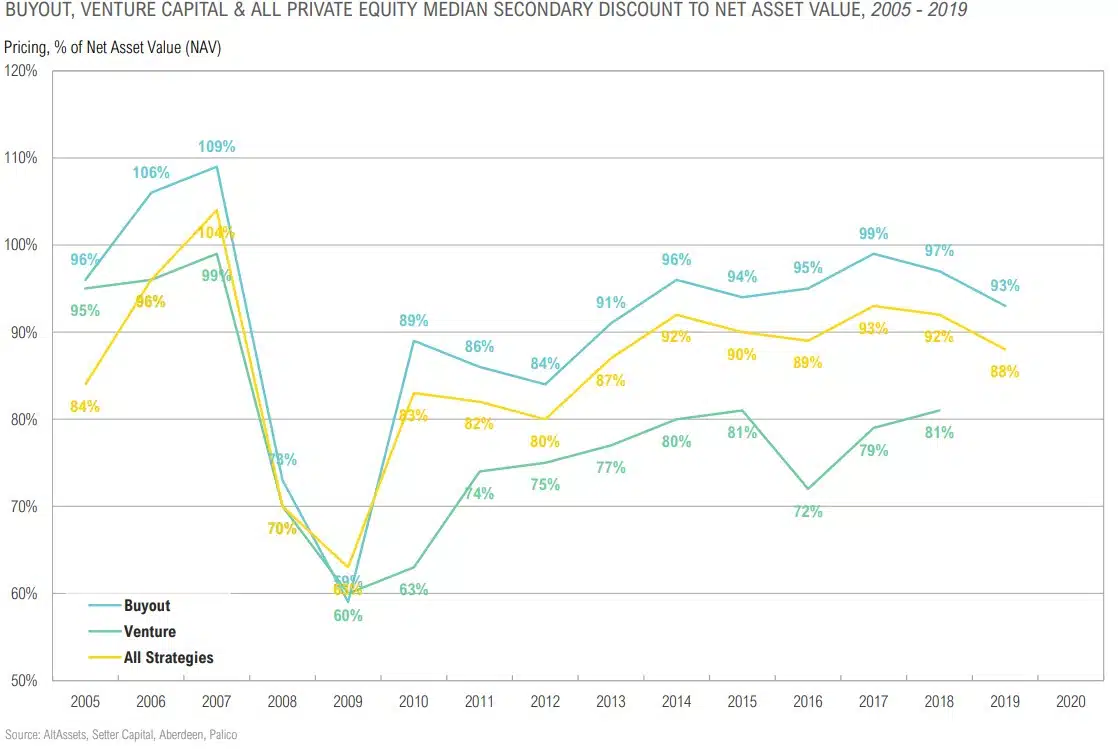

Buyout & Venture Secondaries Should Get Interesting

FIXED INCOME & CREDIT

Post-GFC experience shows that low interest rates don’t trickle down. They inflate financial assets primarily owned by the rich. The idea is to increase borrowing, but the last thing we need is more debt.

– Sheila Bair, Former Chair of the FDIC, June 12, 2020

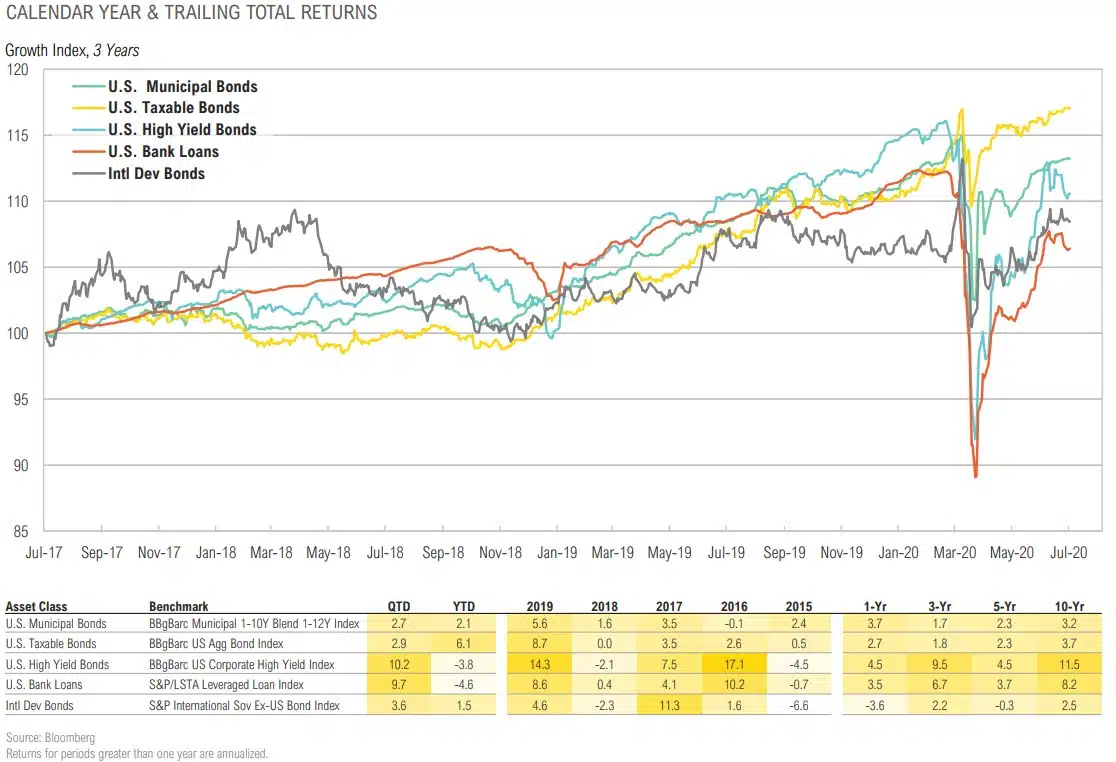

Fixed Income & Credit Returns

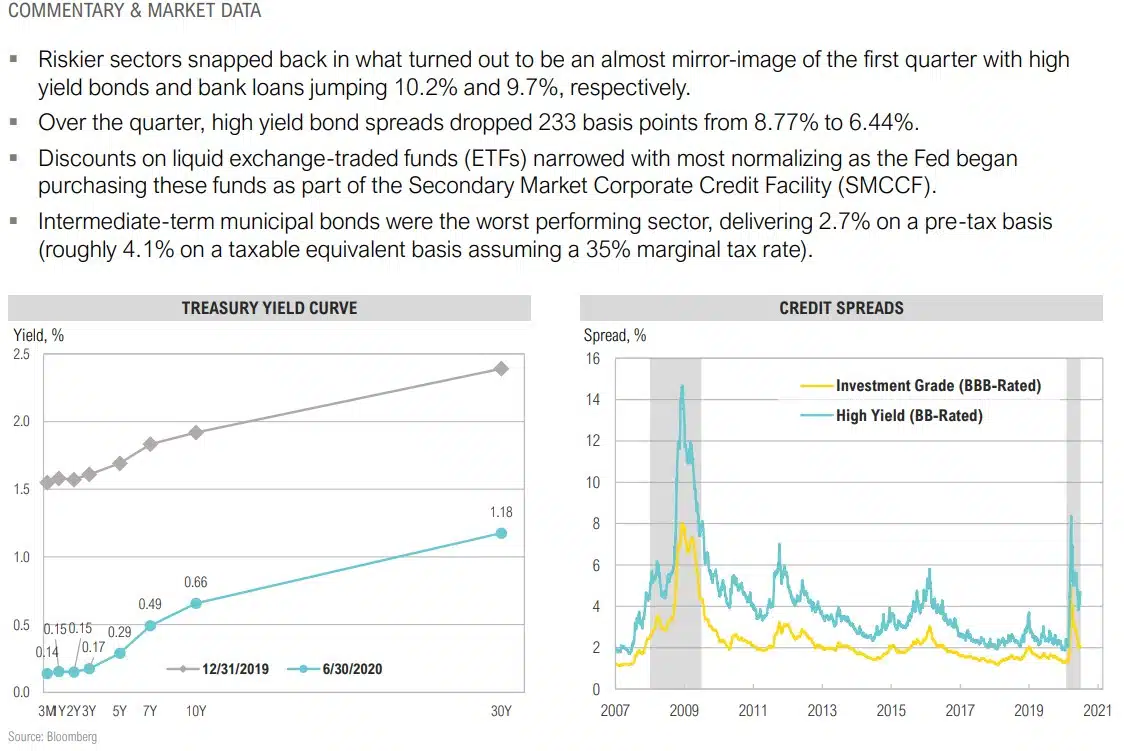

Fixed Income & Credit Review

Fed Purchases of Corporate Bonds

Watch Credit to Lead Equities On the Way Out

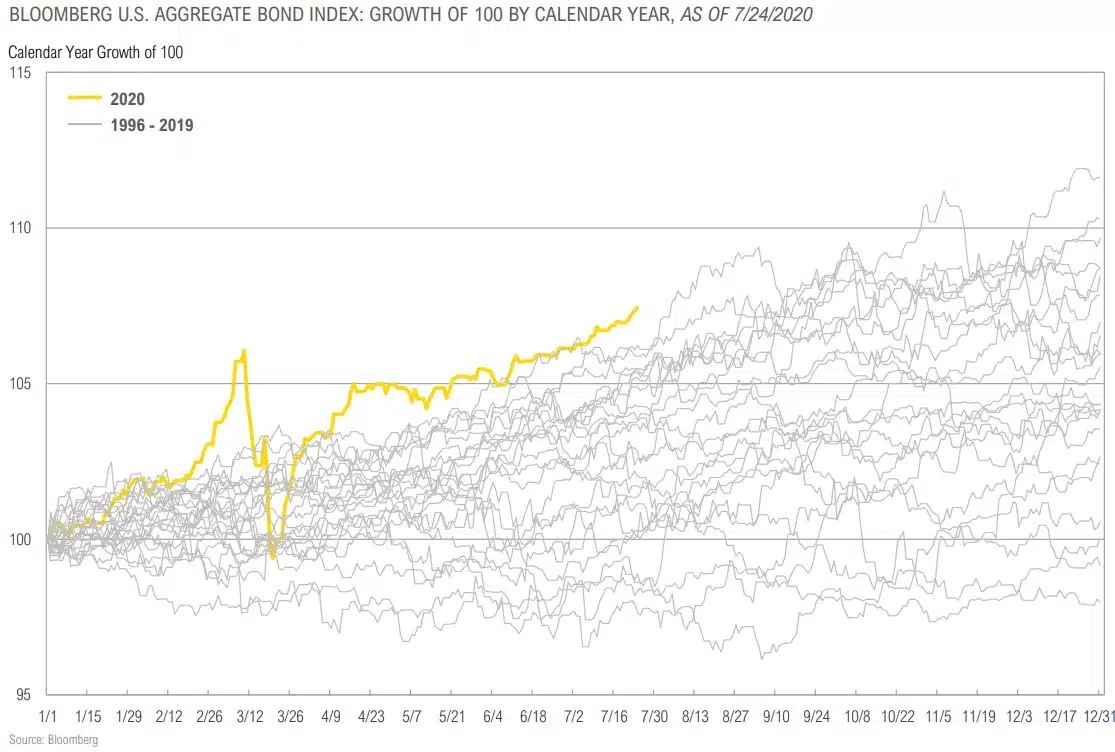

A Record Year for U.S. Core Bonds

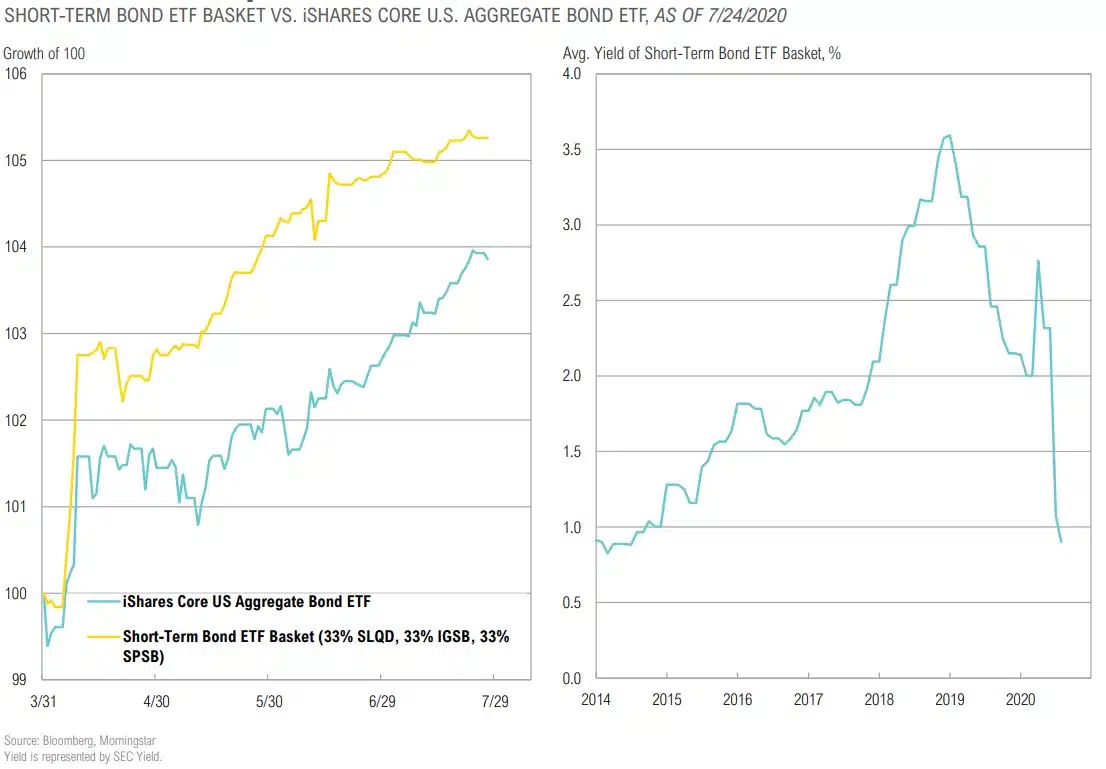

Short-Term Corporate Bond ETF Basket vs. U.S. Core Bonds

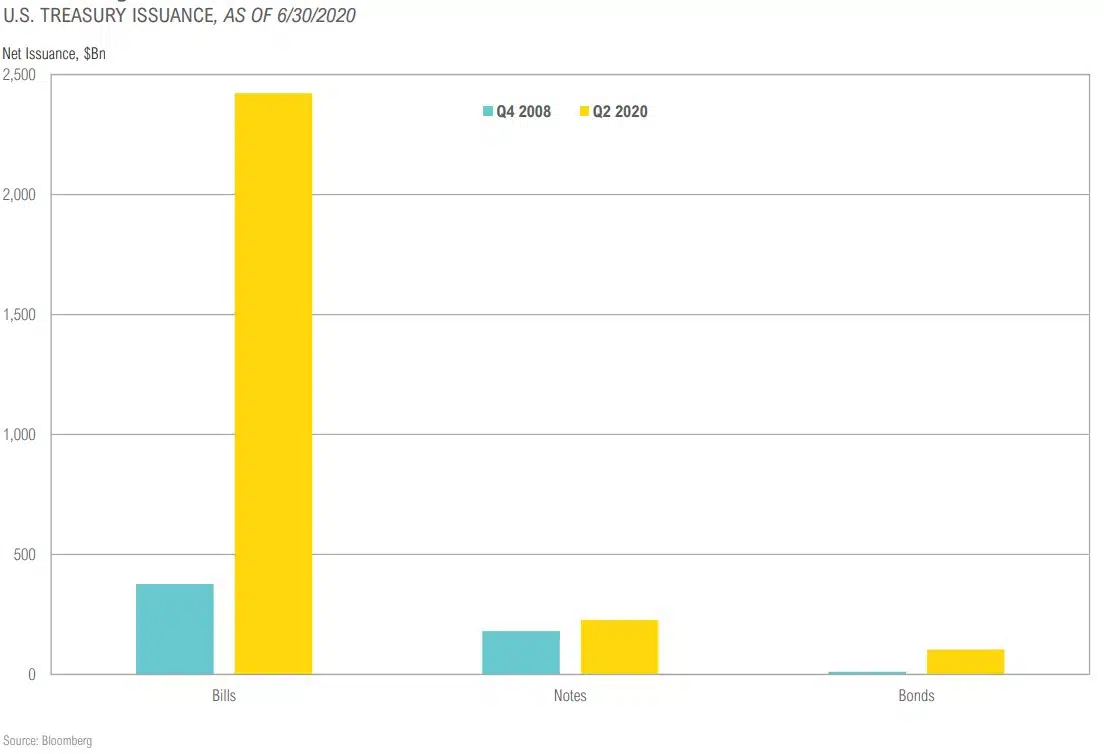

Treasury Issuance Has Been Concentrated in Shorter Duration Bills

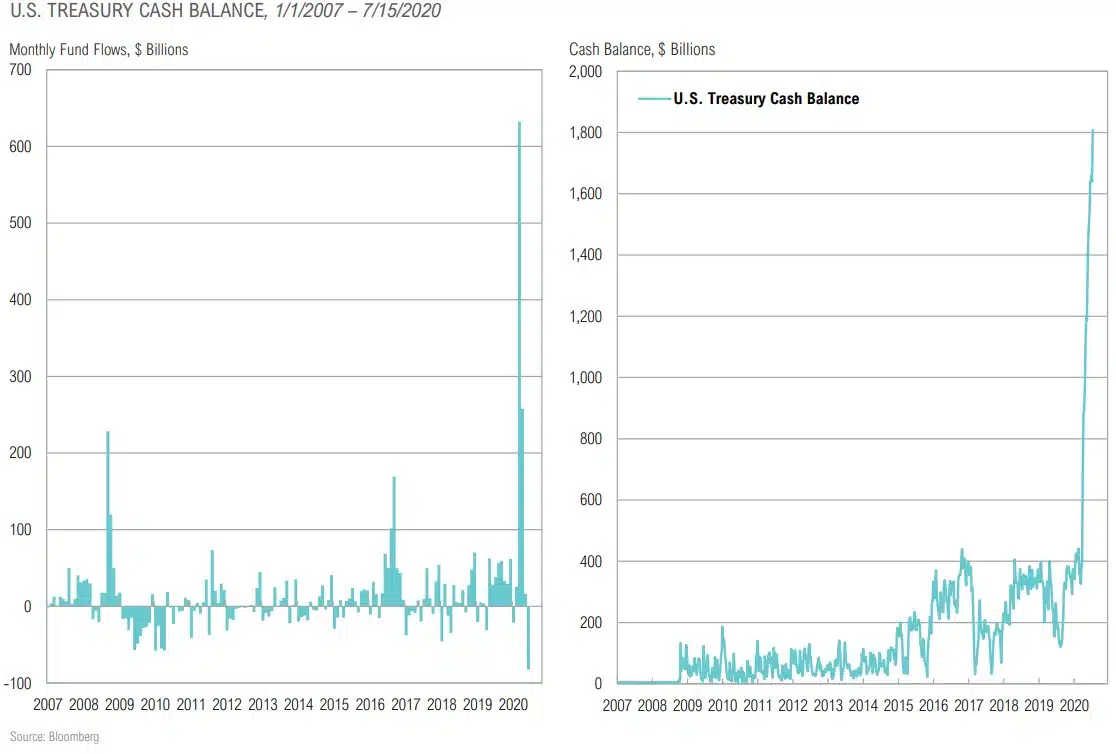

Buyers Have Enabled U.S. Treasury to Build Enormous Cash Reserve

Negative Real Yields Across the Curve

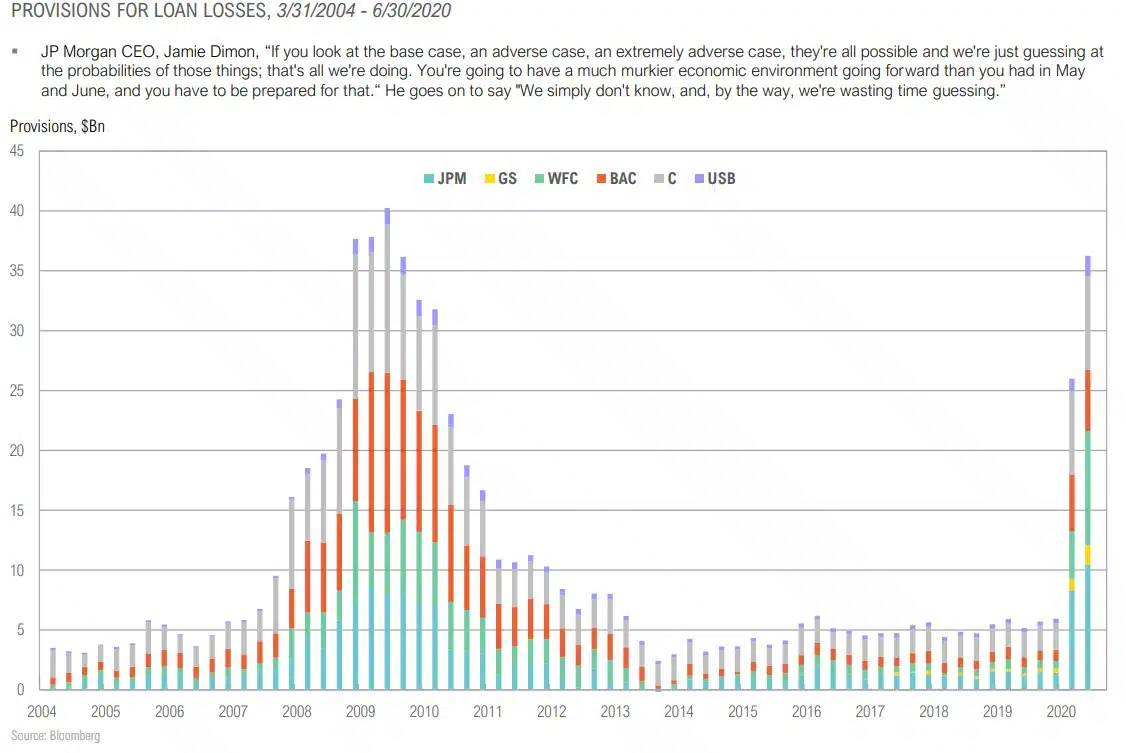

U.S. Bank Provisions for Loan Losses Jump

REAL ASSETS

“Possibly without serious vetting and a conscious decision to adopt it, Modern Monetary Theory is here. Whether we like it or not, we’ll get to see its impact much quicker than I had thought. (And remember, 100% of the “top scholars” polled by The University of Chicago Booth School of Business disagreed with some of MMT’s claims).”

– Howard Marks, Oaktree Chairman, March 2020

“You can’t continue to run deficits, sell debt or print money rather than be productive and sustain that over a period of time.”– Ray Dalio, Bridgewater Associates Co-Founder, July 2020

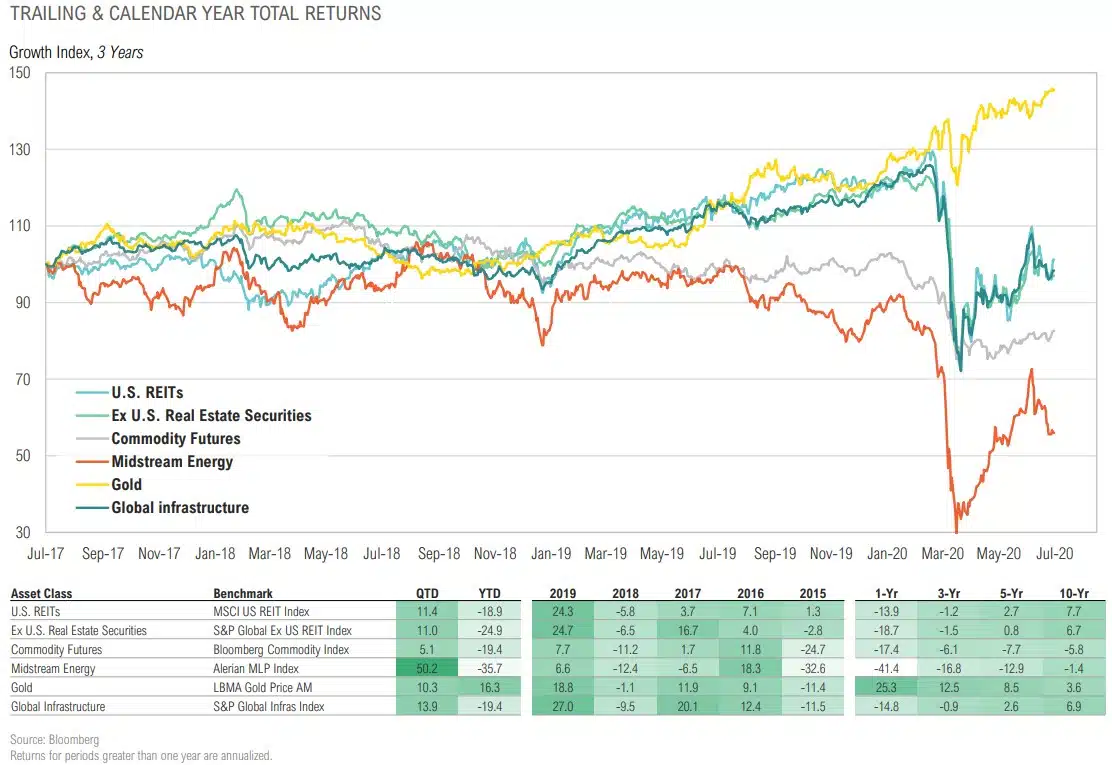

Real Asset Returns

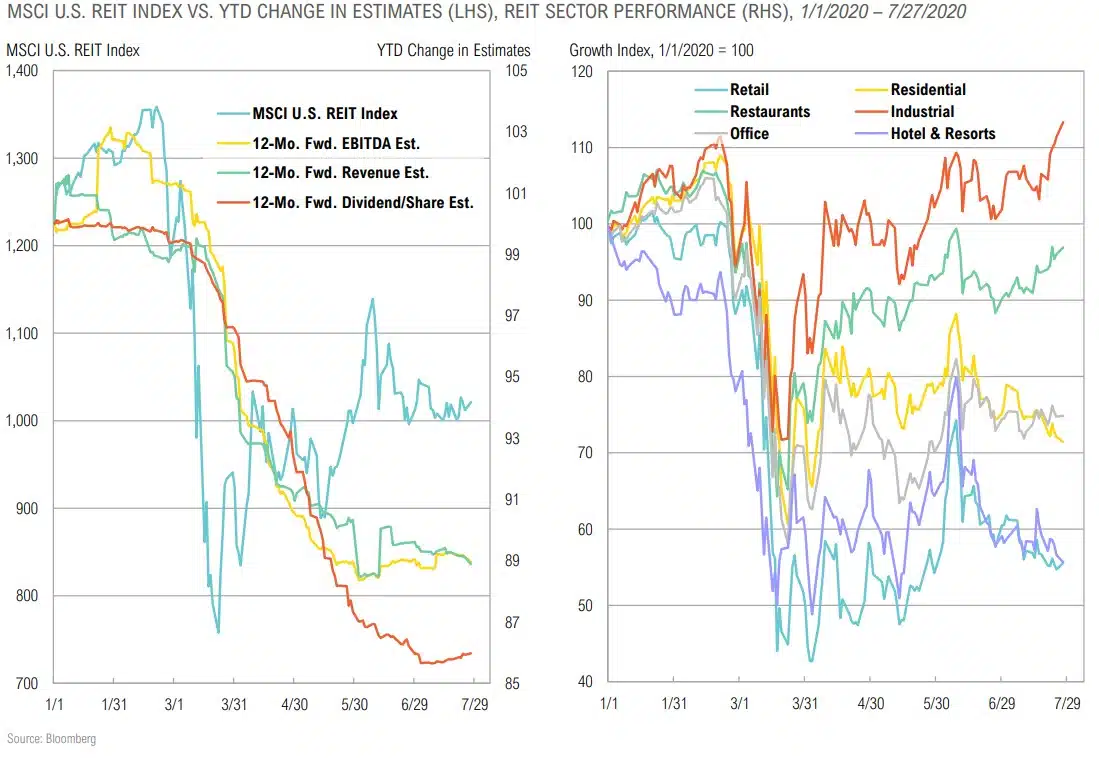

Retail, Hotel & Resort and Office REITs Remain Challenged

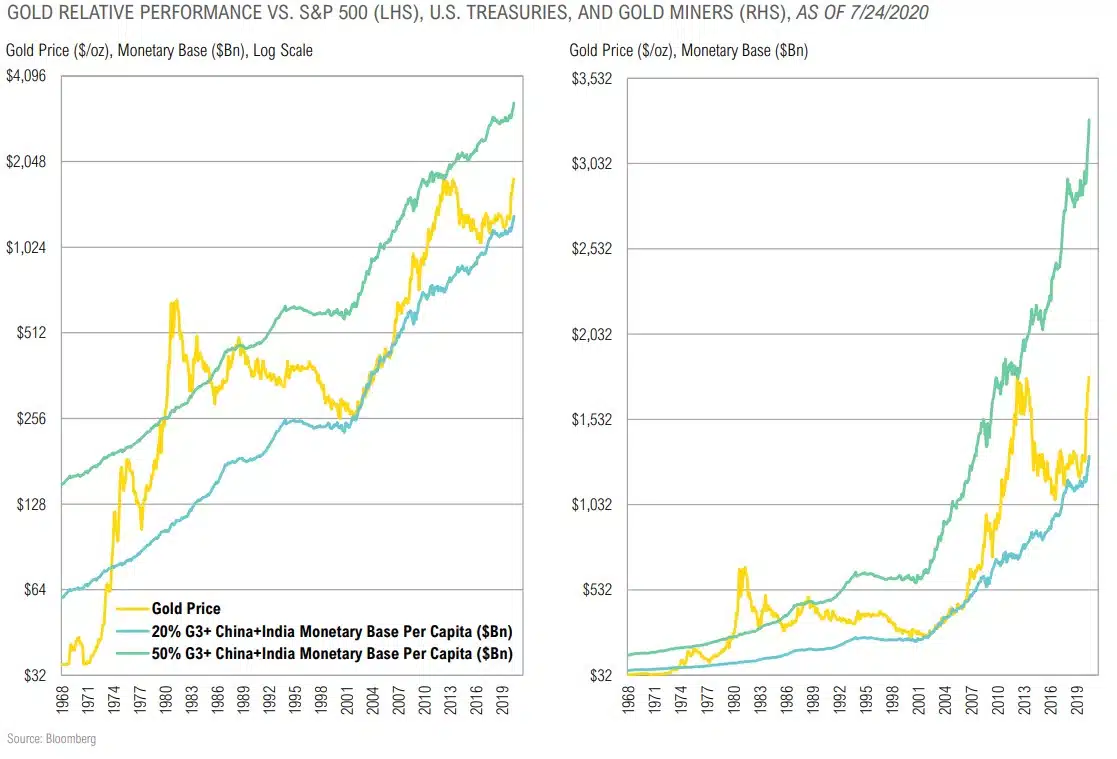

Gold Increasingly Viewed as an Alternative Safe Haven

Gold Trying to Keep Up With Exploding Money Supply

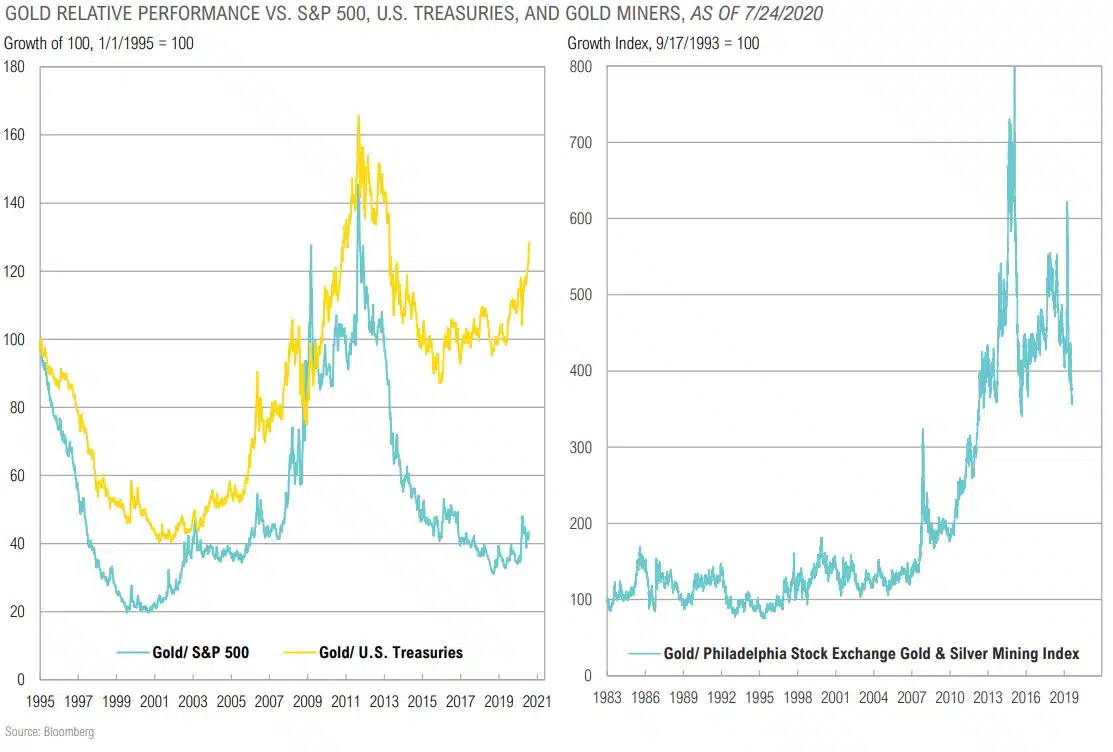

Gold has Room to Run vs. Core Stocks & Bonds… & Miners Have Room to Run vs. Physical

The Next Bubble? Gold Miners vs. Technology Stocks

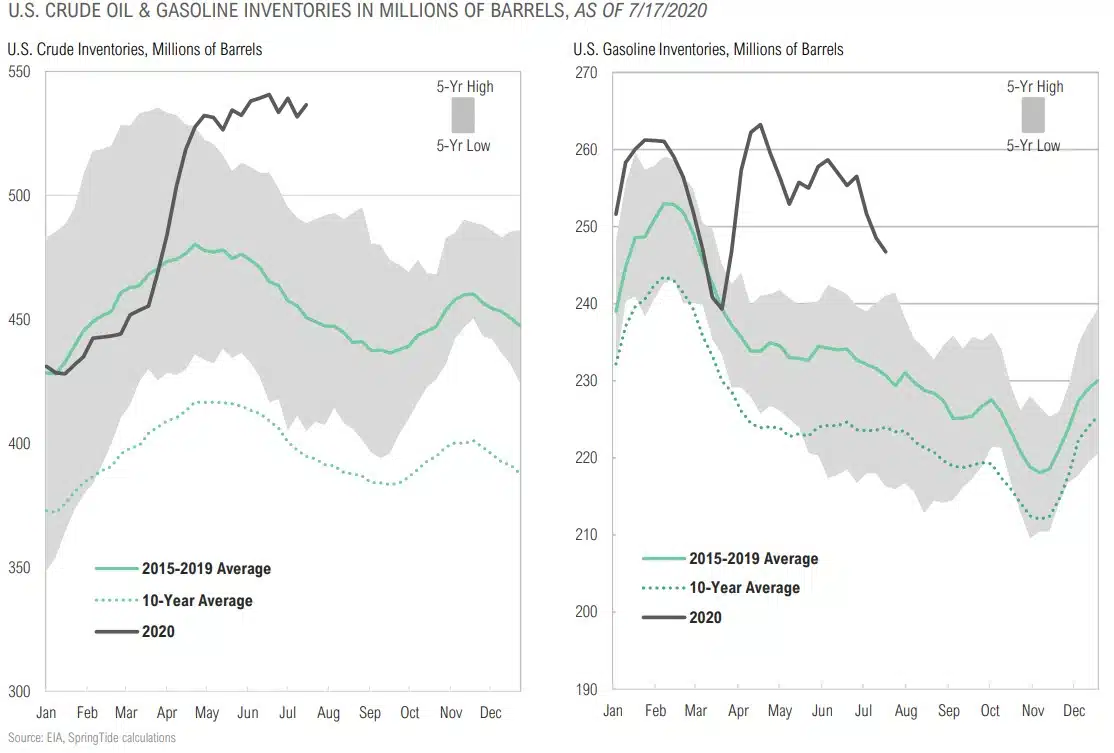

U.S. Crude Oil & Gasoline Inventories Remain Elevated

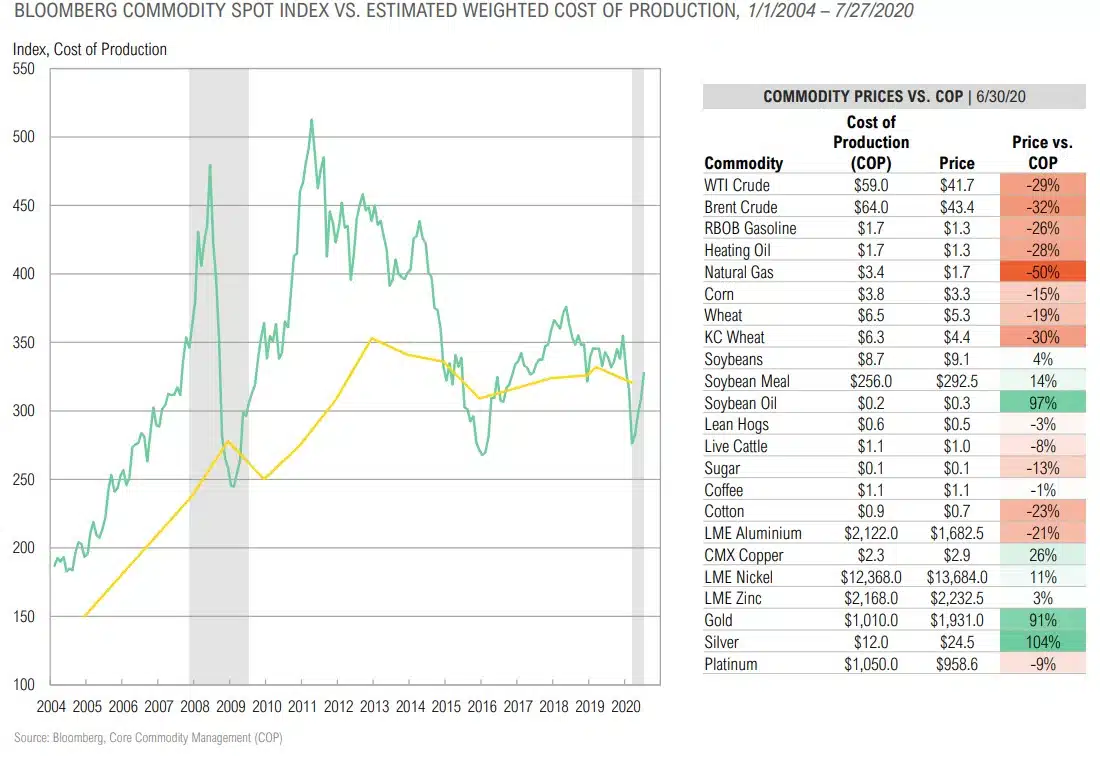

Commodities Back to Marginal Cost of Production

OPPORTUNISTIC

“In some respects it’s different because of the Fed and the liquidity they’ve introduced and the inflation for financial assets that comes with that. But on a bigger picture, it’s so similar [to the Tech Bubble]. Everybody is a genius in a bull market, everybody is making money right now because you’ve got the Fed put and that brings people in who otherwise wouldn’t participate.”

– Mark Cuban, Entrepreneur & Investor, July 2020

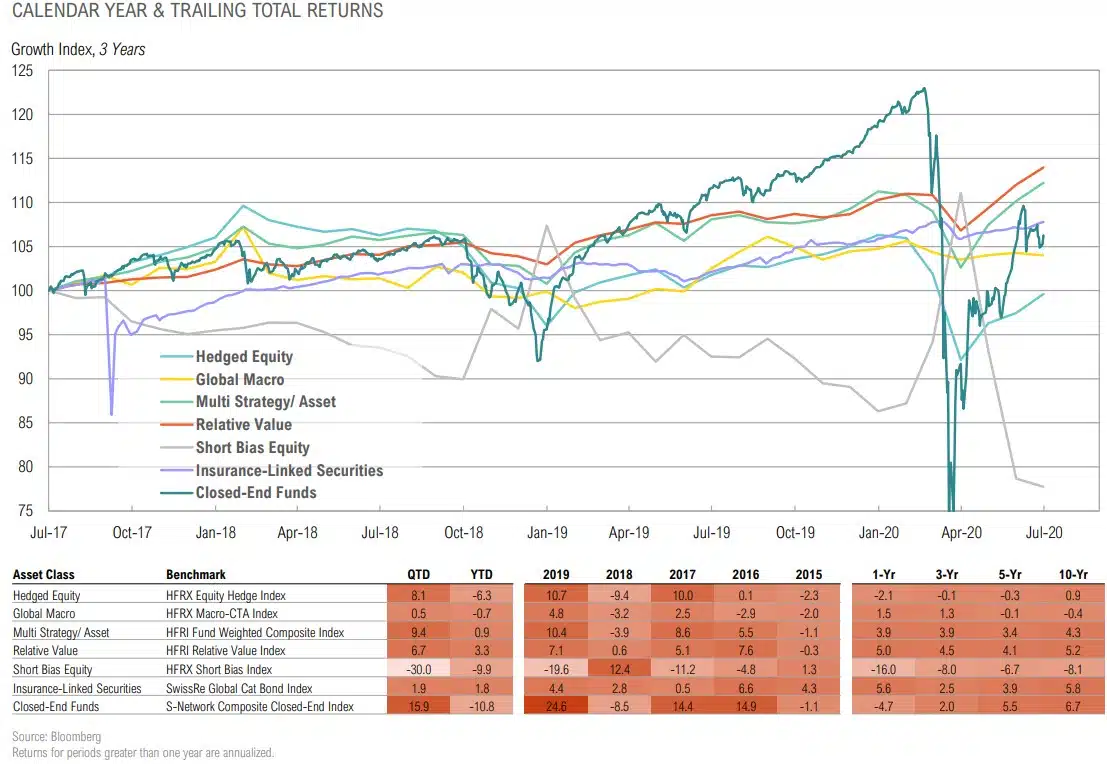

Opportunistic Strategy Returns

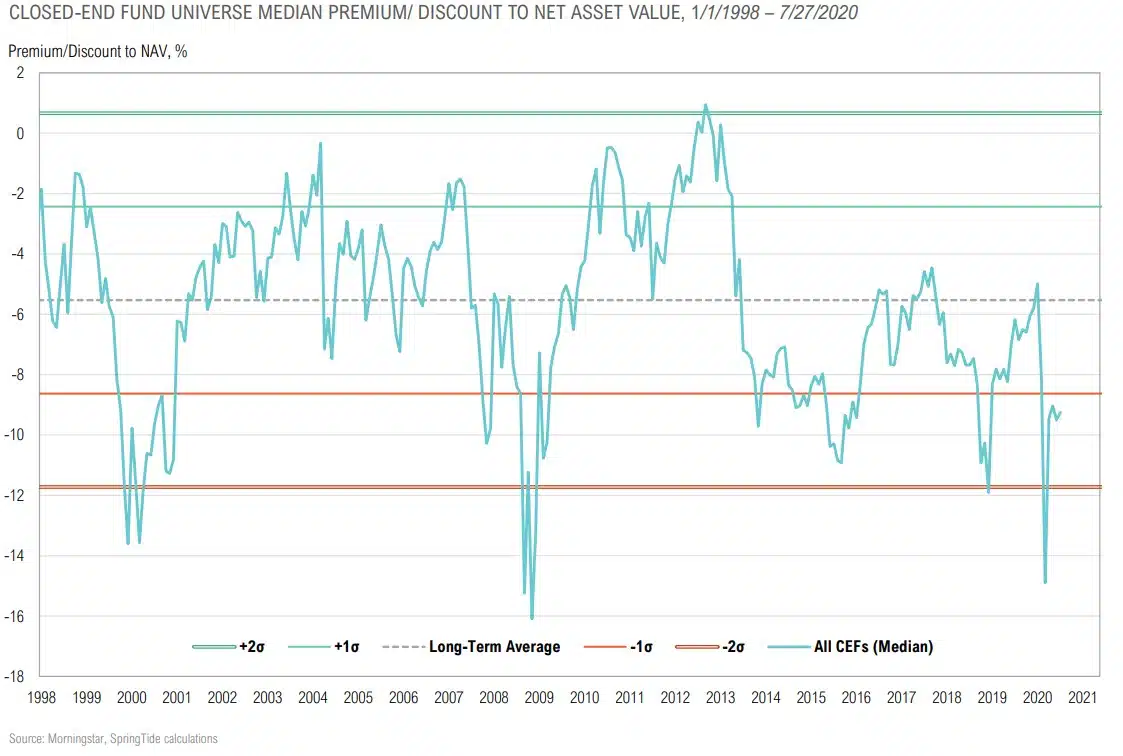

Closed-End Fund Discounts Got as Wide as the Financial Crisis

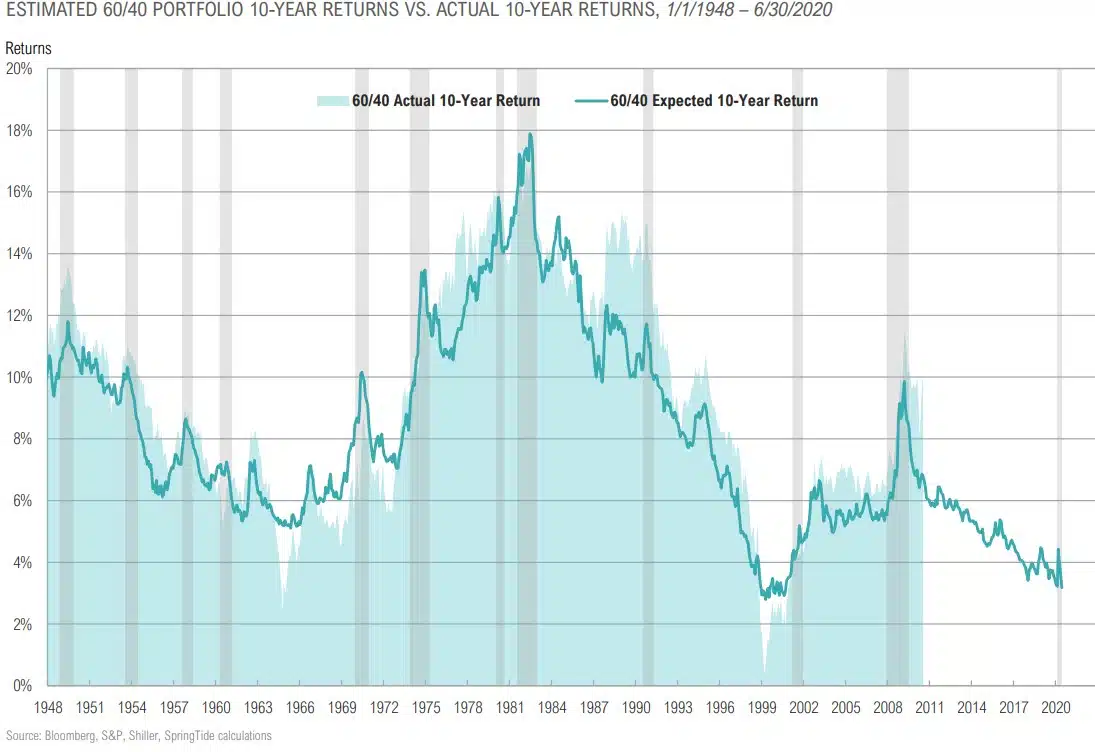

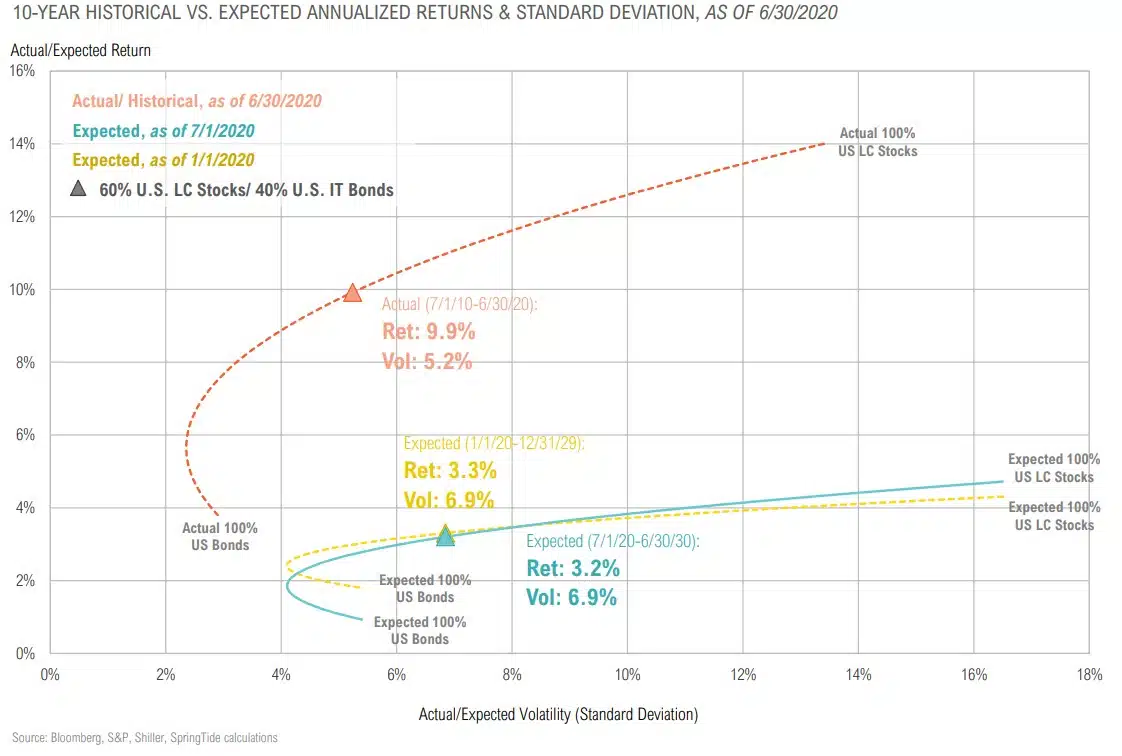

Expected Returns for a 60/40 Remain Low

ASSET ALLOCATION

“Over the last two centuries, the fraction of inflation’s long-run variation explained by long-run money growth has been very high, and relatively stable, in the United States, the United Kingdom and several other countries.”

– Luca Benati, European Central Bank, March 2009

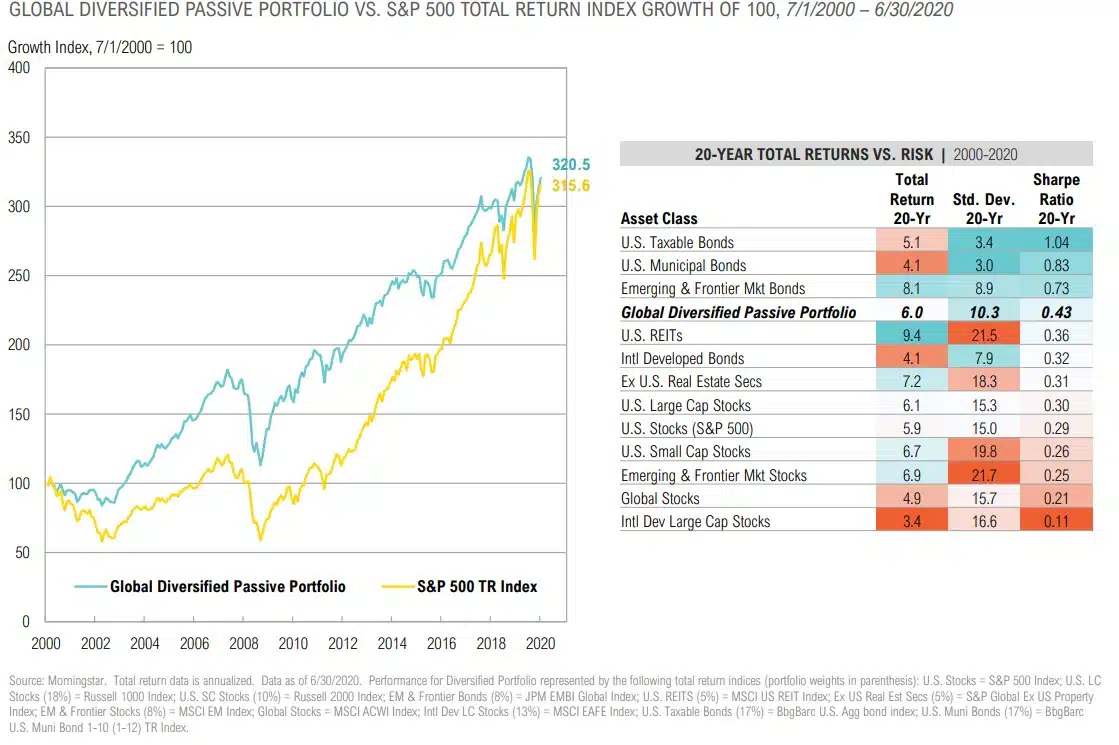

Source: ECB working Paper No. 1027, March 2009: https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1027.pdfDiversification Still Works Over the Long-Term

60/40 Expected Returns

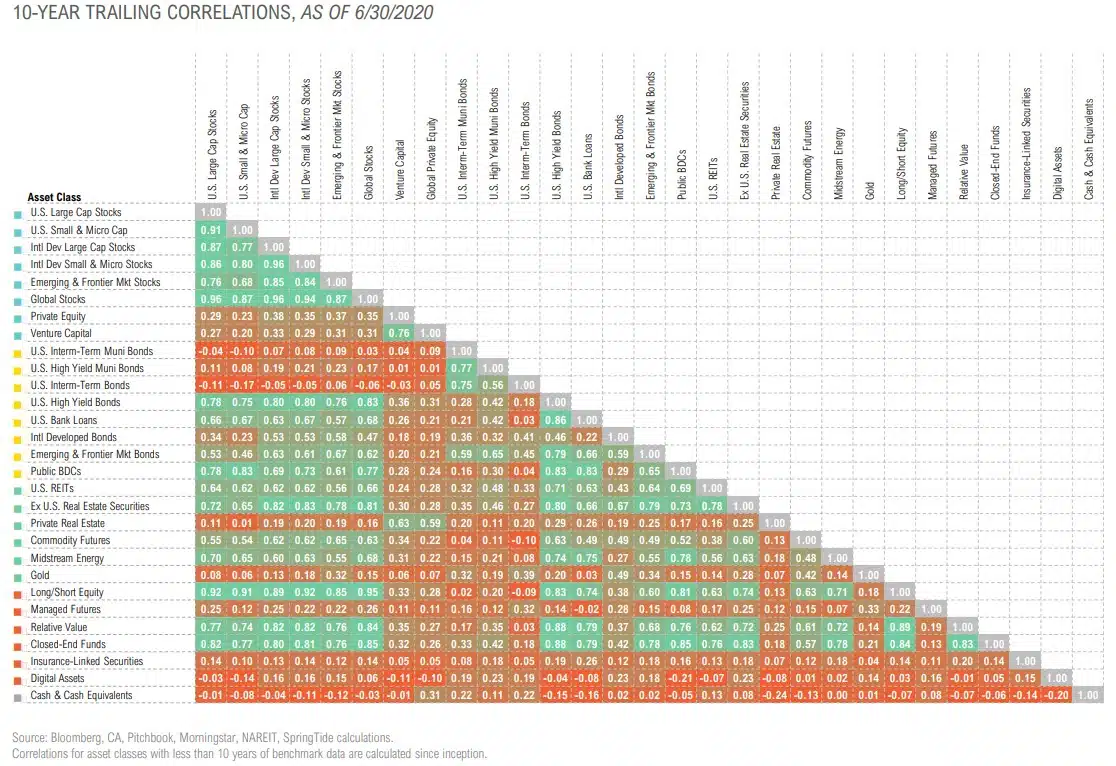

Asset Class Correlations