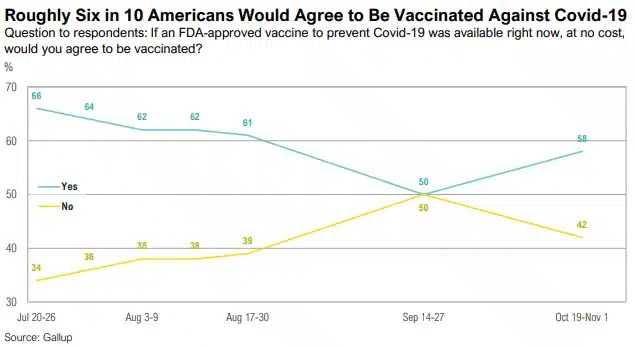

Even amid surging new case numbers and hospitalization data, positive developments have emerged in terms of the pandemic. On November 9, Pfizer and BioNTech announced promising early results from a phase three study of their vaccine candidate, BNT162b2. The initial data suggested the vaccine was 90% effective in reducing COVID19 cases.8 A week later, Moderna announced similarly hopeful results. From a sample of 30,000 study participants, 185 in the placebo group contracted COVID-19, compared to 11 in the group that received the vaccine. Perhaps even more encouraging, none of the vaccinated candidates developed a serious case of COVID-19.9 Two days later, on November 18, Pfizer announced that its vaccine might be even more effective than early results indicated. Of the 44,000 people enrolled in the study, a total of 170 confirmed cases of COVID-19 were evaluated. Of those, just eight came from the vaccinated group, implying an effectiveness of around 95%.10 There are at least two other positive developments. The first is that the number of Americans who are willing to take the vaccine is increasing. According to Gallup data gathered from October 19 to November 1, 58% of Americans would take an FDA-approved vaccine if it were readily available, up from 50% in September.11 Second, distribution of these vaccines has already begun ahead of the expected FDA Emergency Use Approval (EUA) with as many as 40 million expected to be shipped nationally.12

Market Commentary

Policy, Politics, and the Pandemic

Policy, Politics, and the Pandemic

Several clouds that were hanging over the market outlook parted in November, boosting the returns of stocks and high yield bonds and driving down the performance of perceived safe havens like gold.

Overview & Markets

“Markets hate uncertainty” is the clichéd reason for many stock market declines, but the future is always uncertain.1 Stocks have trended higher for decades despite every day being a step into the unknown. The past several weeks have shown us once again that the greater the present angst, the greater the potential for positive surprises—and higher stock prices.

The 14% return of the Russell 3000 Value Index in November marked its best monthly performance since 1979.

Several clouds that were hanging over the market outlook parted in November, boosting the returns of stocks and high yield bonds and driving down the performance of perceived safe havens like gold. In particular, news of an impending vaccine sparked hope for a broader economic recovery and improved returns in parts of the market that had been lagging—especially energy, financials, and smaller companies, which often lack the resources of their larger competitors. When Pfizer and BioNTech announced promising vaccine results on November 9, value stocks, as measured by the Russell 3000 Value Index, outperformed growth stocks (Russell 3000 Growth Index) by an impressive single day spread of 6%. This contributed to the 14% return of the Russell 3000 Value Index in November, marking its best monthly performance on record which goes back to 1979.14 Energy stocks were up 28% (down 31% for the year) while financial stocks rose by 17% (down 5% for the year). Small cap value stocks outperformed large cap growth stocks by 9% (19% vs. 10%). That narrows the massive performance gap on a year-to-date basis. For the year, large cap growth stocks are up 32% while small cap value stocks are down 3%.

Recent polling and prediction market data suggest that the most likely outcome in January will be a Democrat-controlled House of Representatives and a Republican-controlled Senate.

With support from both Wall Street and K Street, Janet Yellen appears likely to become the next Treasury Secretary after Joe Biden announced his intent to nominate the former Federal Reserve Chair.

Politics

On November 24, the General Services Administration (GSA) started the mundane, but crucial, process of allocating office space, providing data access, and freeing up transition resources for the incoming Biden administration.2 The following week, President Trump announced that he would accept the results of the election if the electoral college voted to remove him on December 14.3 In Congress, recent polling and prediction market data suggest that the most likely outcome in January will be a Democrat-controlled House of Representatives and a Republican-controlled Senate.4 That said, the Senate runoff races in Georgia are heating up, and ad spending alone is expected to reach as much as $500 million dollars, reflecting the importance of the composition of the Senate.5 Recent data suggest investors should keep these races on their radars.

On November 23, Joe Biden announced his intention to nominate former Federal Reserve Chair Janet Yellen as Treasury Secretary. The decision will require Senate approval, but Yellen has broad support from both Wall Street and K Street.6 Any question about Yellen’s intention to accept the role was laid to rest when she announced on Twitter, “As Treasury Secretary, I will work every day towards rebuilding that dream for all.” Yellen is the first woman selected for the role, a welcome theme that is emerging from the Biden-Harris administration. Her appointment will strengthen the already tight bond between the Federal Reserve and Treasury department during a time of record deficit spending as well as record purchases of Treasury debt by the Fed. The Fed continues to purchase approximately $120 billion worth of Treasury and Agency debt each month and recently became the largest holder of U.S. Treasury debt, now holding over 22%.7

In addition to the announcements of promising vaccine candidates, there have been two other positive developments related to the pandemic:

1) 58% of Americans say they would be willing to be vaccinated against Covid-19.

2) Distribution of vaccines has already begun ahead of the expected FDA EUA.

Pandemic

Even amid surging new case numbers and hospitalization data, positive developments have emerged in terms of the pandemic. On November 9, Pfizer and BioNTech announced promising early results from a phase three study of their vaccine candidate, BNT162b2. The initial data suggested the vaccine was 90% effective in reducing COVID19 cases.8 A week later, Moderna announced similarly hopeful results. From a sample of 30,000 study participants, 185 in the placebo group contracted COVID-19, compared to 11 in the group that received the vaccine. Perhaps even more encouraging, none of the vaccinated candidates developed a serious case of COVID-19.9 Two days later, on November 18, Pfizer announced that its vaccine might be even more effective than early results indicated. Of the 44,000 people enrolled in the study, a total of 170 confirmed cases of COVID-19 were evaluated. Of those, just eight came from the vaccinated group, implying an effectiveness of around 95%.10 There are at least two other positive developments. The first is that the number of Americans who are willing to take the vaccine is increasing. According to Gallup data gathered from October 19 to November 1, 58% of Americans would take an FDA-approved vaccine if it were readily available, up from 50% in September.11 Second, distribution of these vaccines has already begun ahead of the expected FDA Emergency Use Approval (EUA) with as many as 40 million expected to be shipped nationally.12

Several qualitative developments suggest that higher inflation could be on the horizon, including the Fed’s new mandate, Yellen’s appointment to the Treasury, a vaccine, and the market’s tolerance for continued aggressive fiscal and monetary policies.

Looking Forward

After spiking to nearly 103 in March, the U.S. dollar index has declined by almost 12% to just under 91. At the same time, industrial metal copper, often viewed as a proxy for future growth and inflation, has rallied 64% since the pandemic lows in March. Over the same period, the 10-year U.S. Treasury yield has risen from 51 basis points then to 97 basis points today. Taken together, these moves suggest that investors are anticipating higher inflation—and rightfully so. After all, in an August speech, Jerome Powell announced that the Fed itself is targeting higher inflation.13 From our perspective, several qualitative developments suggest that higher inflation could be on the horizon, including the Fed’s new mandate, Yellen’s appointment to the Treasury, a vaccine, and the market’s tolerance for continued aggressive fiscal and monetary policies. While we do not believe inflation will increase suddenly, we are cognizant that it could move higher in a linear fashion from these levels and will continue to diligently monitor the relevant developments.

Performance Disclosures

All market pricing and performance data from Bloomberg, unless otherwise cited. Asset class and sector performance are gross of fees unless otherwise indicated.

Citations

Share it :

Disclaimer

Magnus Financial Group LLC (“Magnus”) did not produce and bears no responsibility for any part of this report whatsoever, including but not limited to any microeconomic views, inaccuracies or any errors or omissions. Research and data used in the presentation have come from third-party sources that Magnus has not independently verified presentation and the opinions expressed are not by Magnus or its employees and are current only as of the time made and are subject to change without notice.

This report may include estimates, projections or other forward-looking statements, however, due to numerous factors, actual events may differ substantially from those presented. The graphs and tables making up this report have been based on unaudited, third-party data and performance information provided to us by one or more commercial databases. Except for the historical information contained in this report, certain matters are forward looking statements or projections that are dependent upon risks and uncertainties, including but not limited to factors and considerations such as general market volatility, global economic risk, geopolitical risk, currency risk and other country-specific factors, fiscal and monetary policy, the level of interest rates, security-specific risks, and historical market segment or sector performance relationships as they relate to the business and economic cycle.

Additionally, please be aware that past performance is not a guide to the future performance of any manager or strategy, and that the performance results and historical information provided displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Therefore, it should not be inferred that these results are indicative of the future performance of any strategy, index, fund, manager or group of managers. Index benchmarks contained in this report are provided so that performance can be compared with the performance of well-known and widely recognized indices. Index results assume the re-investment of all dividends and interest and do not reflect any management fees, transaction costs or expenses.

The information provided is not intended to be, and should not be construed as, investment, legal or tax advice nor should such information contained herein be construed as a recommendation or advice to purchase or sell any security, investment, or portfolio allocation. An investor should consult with their financial advisor to determine the appropriate investment strategies and investment vehicles. Investment decisions should be made based on the investor’s specific financial needs and objectives, goals, time horizon and risk tolerance. This presentation makes no implied or express recommendations concerning the way any client’s accounts should or would be handled, as appropriate investment decisions depend upon the client’s specific investment objectives.

Investment advisory services offered through Magnus; securities offered through third party custodial relationships. More information about Magnus can be found on its Form ADV at www.adviserinfo.sec.gov.

Terms of Use

Definitions

Asset class performance was measured using the following benchmarks: U.S. Large Cap Stocks: S&P 500 TR Index; U.S. Small & Micro Cap: Russell 2000 TR Index; Intl Dev Large Cap Stocks: MSCI EAFE GR Index; Emerging & Frontier Market Stocks: MSCI Emerging Markets GR Index; U.S. Intermediate-Term Muni Bonds: Bloomberg Barclays 1-10 (1-12 Yr) Muni Bond TR Index; U.S. Intermediate-Term Bonds: Bloomberg Barclays U.S. Aggregate Bond TR Index; U.S. High Yield Bonds: Bloomberg Barclays U.S. Corporate High Yield TR Index; U.S. Bank Loans: S&P/LSTA U.S. Leveraged Loan Index; Intl Developed Bonds: Bloomberg Barclays Global Aggregate ex-U.S. Index; Emerging & Frontier Market Bonds: JPMorgan EMBI Global Diversified TR Index; U.S. REITs: MSCI U.S. REIT GR Index, Ex U.S. Real Estate Securities: S&P Global Ex-U.S. Property TR Index; Commodity Futures: Bloomberg Commodity TR Index; Midstream Energy: Alerian MLP TR Index; Gold: LBMA Gold Price, U.S. 60/40: 60% S&P 500 TR Index; 40% Bloomberg Barclays U.S. Aggregate Bond TR Index; Global 60/40: 60% MSCI ACWI GR Index; 40% Bloomberg Barclays Global Aggregate Bond TR Index.