From an economic standpoint, this global conflict has no apparent winners. China, the second largest economy in the world, grew just 0.4% in the second quarter from a year prior, representing its second-lowest quarterly growth rate since at least 1992.3 While export growth remained robust at 4%, import growth slowed to just 1% in July, another sign of weakening domestic demand.23 At least some of China’s current economic pain is self-inflicted, as a draconian “zero-COVID” policy has caused rolling lockdowns, which have impacted city after city. Most recently, Chengdu, a megacity home to 21 million people and 1.7% of China’s GDP, locked down all residents for mass testing on September 1 over the discovery of around 1,000 cases in 10 days.24 This represents the fourth megacity lockdown in 2022, double the amount from a year prior. Shenzen, Zhengzhou, and Shanghai all locked down earlier this year, affecting more than 50 million people.

Market Commentary

Market Commentary – August , 2022

Stalemate

This year has seen a terrible real-world game of chess played by global superpowers with untold human cost, accompanied by plenty of cheating, conspiracies, and back-door dealing

Global Chess

In early September, the world of chess was rocked by World Champion Grand Master Magnus Carlsen’s abrupt withdrawal from a major tournament in St. Louis, following his stunning loss to the American up-and-comer Hans Niemann, which broke Carlsen’s 53- game winning streak.1 After walking away from the $350,000 Sinquefield Cup, Carlsen hinted at foul play by his opponent, and the chess world exploded with allegations of cheating, as well as speculative conspiracy theories.2 For years, pundits and historians have compared war to a game of chess, comparing the intense strategy and sometimes inscrutable moves that characterized each theater. And now there is a new parallel to take into account—the swirl of disinformation and conspiracy theories that plague them both.

This year has seen a terrible real-world game of chess played by global superpowers with untold human cost, accompanied by plenty of cheating, conspiracies, and back-door dealing. Although the consequences of this conflict are global, the epicenter is Europe. Ukraine is resolutely defending itself from an attack from Russia, Russia is dealing with severe sanctions, and western Europe is bracing for a winter cut off from Russian gas and fuel. Economies have been strained to breaking points, and unexpected alliances have been forged as global powers seek to align themselves with trading partners and secure access to the fossil fuels needed to heat homes, power their heavy industries, and maintain economic growth. The prize in this deadly game is fossil fuels, and, unlike Magnus Carlsen, no one can afford to withdraw.

Economies have been strained to breaking points, and unexpected alliances have been forged as global powers seek to align themselves with trading partners and secure access to fossil fuels

Although a continent away, China remains an active participant in the conflict given its financial ties to Russia

Although a continent away, China remains an active participant in the conflict given its financial ties to Russia. With Chinese economic growth lower than at any point in the past three decades (excluding 2020), Chinese president Xi Jinping has been subtly strengthening the Middle Kingdom’s relationship with Russia.3 After the invasion of Ukraine, many nations cut back on Russian oil and gas and implemented other forms of financial restrictions.4 In contrast, China stepped in to fill the void by buying Russian oil at steep discounts, thereby providing Russian energy companies (and the state indirectly) with the much-needed cash flow to keep the Russian economy running.5 As a result, Russian oil revenues have risen 38% from a year earlier due to both higher oil prices and increased volumes from Asian buyers.6 Further distancing themselves from the rest of the world, China has repeatedly ignored President Vladimir Zelenskiy’s requests for direct talks since the Russian invasion. In fact, the Ukrainian President says it’s been over a year since the two last spoke.7 Russia has returned the favor by upping its imports of Chinese goods and renewing its interest in the yuan, causing Russian trading of the yuan to rise by more than 40x since the start of the year.8 Putin has gone as far as reviving a plan to issue yuan-denominated debt and considering a plan to buy as much as $70 billion in yuan and other “friendly” currencies to weaken the surging ruble to make Russian exports more attractive to trading partners.9

The U.S. has possibly intensified the situation through its recent dealings with Taiwan. Speaker of the U.S. House of Representatives, Nancy Pelosi, visited the self-governing island in early August, representing the first high-ranking U.S. officer to visit since Newt Gingrich in 1997.10 China claims Taiwan as part of its territory and serves as a fundamental part of the ruling communist party’s “One China” ideology. President Xi Jinping responded to Pelosi’s visit with a series of military drills over several days around the island, asserting that China would safeguard its “national sovereignty and territorial integrity” over Taiwan.11 Although Xi eventually ended the drills, he warned repeatedly that the U.S. would pay a “heavy price” if it continued to meddle in Taiwan-China affairs.12 That threat hasn’t deterred the U.S. so far. Since Pelosi’s visit, several other U.S. leaders have made trips to the island, and on September 2, the U.S. approved a $1.1 billion sale of new weapons and military logistics to bolster Taiwan’s defenses.13

As this dangerous game of chess has drawn on, both sides have become more desperate to use their dwindling pieces carefully and pull other players in

As this dangerous game of chess has drawn on, both sides have become more desperate to use their dwindling pieces carefully and pull other players in. In a move that is frustrating to the U.S. administration, Russia continues to strengthen its ties to Saudi Arabia. This alliance is of crucial strategic importance since the two countries are responsible for over 20% of global oil and natural gas production.14,15 It was recently disclosed that Kingdom Holding, one of Saudi Arabia’s highest-profile investors, invested $500 million in Russian state-owned energy companies shortly before the invasion of Ukraine this year, including $364 million in Gazprom.16 The two nations cooperate closely on oil production through the OPEC+ group, collectively producing 44 million barrels of oil/day, 43% of global production.17 The nations in OPEC+ also represent 41% of global natural gas production per year.15 Just days after Russian Deputy Prime Minister Alexander Novak met with Saudi Arabia’s Energy Minister, the group decided to increase production by a lower-than-expected 100,000 barrels per day on August 3.18 Novak was quoted saying despite a recovery in demand, the “cautious decision” by OPEC+ was due to market uncertainties, including growing COVID-19 cases and the destruction of transportation and logistics chains because of sanctions against Russia. In a move that was sure to frustrate Washington further, the group rolled back this increase on September 4.19

As this dangerous game of chess has drawn on, both sides have become more desperate to use their dwindling pieces carefully and pull other players in

To combat OPEC+ production cuts, Biden has used the Strategic Petroleum Reserve (SPR) as a key chess piece, drawing down the reserve by as much as 10 million barrels per week in August.20 All told, Biden has released nearly 200 million barrels of the SPR this year, representing 31% of its total supply. No doubt, this is alleviating the pain of higher energy prices in the short term, but it remains to be seen how this will help in the longer term, specifically where the pain of energy shortages are most acute—in Europe.

On September 2, Russia’s Gazprom PJSC made a last- minute decision not to turn the critical Nord Stream Pipeline back on after three days of maintenance, further restricting painfully constrained supply levels heading into the winter months

If record-high gas prices, which forced plant shutdowns in Germany, and a steady stream of stories of exorbitant energy bills across Europe were not enough, on September 2, Russia’s Gazprom PJSC made a last-minute decision not to turn the critical Nord Stream Pipeline back on after three days of maintenance, further restricting painfully constrained supply levels heading into the winter months.21,22 As of August, Dutch front-month gas, a benchmark for Europe, was up 17-fold from three years prior, which compares to just four times higher for U.S. natural gas. according to prices at Henry Hub.

“…we are strongly committed to bringing inflation back down to our 2 percent goal”

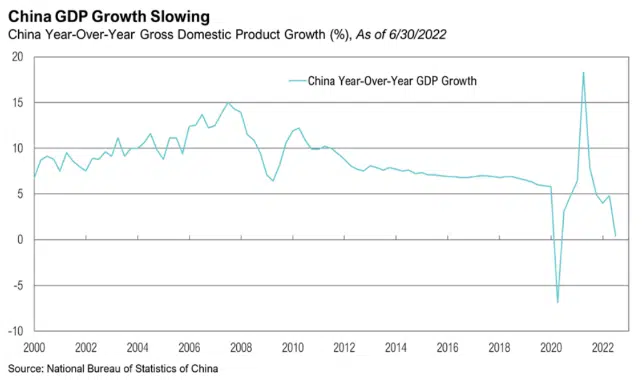

China's Economic Woes

From an economic standpoint, this global conflict has no apparent winners. China, the second largest economy in the world, grew just 0.4% in the second quarter from a year prior, representing its second-lowest quarterly growth rate since at least 1992.3 While export growth remained robust at 4%, import growth slowed to just 1% in July, another sign of weakening domestic demand.23 At least some of China’s current economic pain is self-inflicted, as a draconian “zero-COVID” policy has caused rolling lockdowns, which have impacted city after city. Most recently, Chengdu, a megacity home to 21 million people and 1.7% of China’s GDP, locked down all residents for mass testing on September 1 over the discovery of around 1,000 cases in 10 days.24 This represents the fourth megacity lockdown in 2022, double the amount from a year prior. Shenzen, Zhengzhou, and Shanghai all locked down earlier this year, affecting more than 50 million people.

President Xi and the Chinese Communist Party (CCP) apparently have priorities other than raw economic growth for the time being

President Xi and the Chinese Communist Party (CCP) apparently have priorities other than raw economic growth for the time being. In a high-level meeting of the CCP in late July, the state media said China will “try hard to achieve the best possible results for the economy this year,” dropping any mention of the country’s 5.5% growth target.25 That stance was solidified the following week, when Chinese leaders reiterated “their GDP goal is a guidance, not a hard target” and that there won’t be penalties handed out to state officials for failing to achieve it.26 The only attempt the CCP made to change its zero-COVID policy was a vaccination mandate announced in July. Following public outrage that the mandate illegally limited Chinese freedoms, the government cancelled it just 48 hours after its announcement–a rare concession to public criticism.27

If CCP anti-growth policies remain in place for the foreseeable future, the global economy will certainly feel the impact

If CCP anti-growth policies remain in place for the foreseeable future, the global economy will certainly feel the impact. The most worrisome issue may be the developing Chinese property crisis. Real estate constitutes about one-third of China’s economic activity, and housing accounts for about 70% of household wealth,28 compared to roughly 30% for United States residents,29 which has led some to call the Chinese real estate market the most important sector in the world.30 As a result of government regulation, Chinese homeowners are struggling to pay their mortgages. The situation has gotten to a point where hundreds of thousands of homeowners are banding together and refusing to repay loans on unfinished properties.28 The public outcry has forced the CCP to act to stabilize the housing market, announcing several stimulative measures, including a surprise rate cut in August, a $146 billion policy package including funds for infrastructure projects, and a mandate for banks to lower rates to make mortgages cheaper.31,32 The CCP has even considered a mortgage grace period for homebuyers. However, this action would force banks to forfeit $4.6 billion of interest income.33

With the homeowner being the target of government stimulus, institutional investors and developers have been left to fend for themselves. A third of HSBC’s $12 billion portfolio of Chinese commercial real estate is now considered substandard or impaired.34 Developers’ earnings slumped 87% in the first half of 2022, and the top 100 property developers in China saw their revenues collectively fall 40% from a year earlier.35,36

Housing sector woes are beginning to spill over into the banking sector. Chinese banks saw their bad loans increase to $426 billion in the first half of 2022

Housing sector woes are beginning to spill over into the banking sector. Chinese banks saw their bad loans increase to $426 billion in the first half of 2022.37 Chinese bank exposure to real estate is bigger than that of any other industry, with $5.6 trillion in outstanding mortgages and $1.7 trillion in loans to developers. In particular, the Bank of China holds significantly more than its peers–about 38% of total loans.38 Complicating matters, Chinese regulators will now require companies selling debt offshore to secure permission first before doing so, making it more difficult for developers to get access to much-needed capital to shore up their balance sheets.38 Outside of the housing sector, institutional divestment is beginning to accelerate, especially from overseas. For example, for the new iPhone 14, Apple shortened its production lag time between China- and India-produced phones to just two months.39 Jeep shut down its only factory in China because local politicians kept meddling in the market.40 Domestic tech giant Alibaba saw its net income drop 50% from a year prior and reduced its headcount for the first time since 2016, cutting 10,000 jobs or 4% of its workforce.41

The European Central Bank was forced to hike interest rates by 75 basis points, its biggest hike ever

Markets

If there is a silver lining to the strained geopolitical environment, it is the increase in the perceived value of the greenback, which is on a historic run. Through August, the U.S. Dollar Index, which measures the value of the dollar compared to a basket of developed market currencies, is up 14.5%. For perspective, if the dollar were to end the year at current levels, it would mark its best annual return since 1983. Emerging market currencies have fared poorly, if not as bad as their developed peers, down 6.9% year-to-date relative to the dollar as measured by the Deutsche Bank EM FX Equally Weighted Spot Index, an equal-weighted basket of 21 emerging market currencies. Poor foreign exchange performance has been the reason why. Despite less technology exposure, both the MSCI EAFE and MSCI Emerging Market Indexes have underperformed their U.S. counterparts this year. In local currency terms, both indexes have outperformed the U.S. year to date.

Weaker foreign currencies make imports by these countries more expensive and exacerbates inflation in their domestic economies. In Europe, the European Central Bank was forced to hike interest rates by 75 basis points, its biggest hike ever, amidst an energy crisis and a potential recession due to high energy prices, which are priced in U.S. dollars. Many emerging market countries price their bonds in U.S. dollar terms, meaning that when the dollar appreciates, it makes it more difficult for them to pay their obligations to investors. Lastly, the dollar rally is creating problems for the countries that peg their local currency to the dollar. While China no longer employs a strict peg, the PBOC has generally kept the local currency trading between $6 and $7 since 2010. In 2022, the yuan has depreciated 7.9% against the dollar and trades in the upper end of that range at $6.90 as of the end of August. While a weaker yuan boosts the demand for Chinese exports, depreciation may act as a catalyst for further capital outflows. As a result, the PBOC set its strongest yuan fix against the dollar since 2019 in an effort to strengthen the currency.

The S&P 500 gave back some of its July rally, falling 4.1% over the month. From a style perspective, value stocks outperformed growth stocks and real estate had a difficult month

The S&P 500 gave back some of its July rally, falling 4.1% over the month. From a style perspective, value stocks outperformed growth stocks, as the Russell 1000 Value Index fell 3.0% while the Russell 1000 Growth Index fell 4.7%. Small cap stocks beat large cap stocks by 2%, returning -2.1% as proxied by the Russell 2000 Index. Within real assets, midstream energy was once again a top performer for the month, returning 4.0%. Year to date, the industry has returned 28.7%, outperforming the S&P 500 by 44.8%. Real estate had a difficult month, returning -6.0% proxied by the MSCI U.S. REIT Index, as mortgage rates continued their rapid ascent. The average 30-year fixed rate mortgage hit 6.1% on September 8, its highest level since November 2008.

U.S. fixed income gave back all its July gains with the Bloomberg U.S. Aggregate Bond Index down 2.8% as yields reversed course and moved higher once again. The 10-year U.S. treasury rate rose 48 basis points to 3.15%, and the 2-year rate rose 56 basis points to 3.45%. The yield curve remains deeply inverted with the spread between these two rates sitting at -30 basis points. The 2-year is now at a 15-year high, last seeing these levels in August 2007. U.S. high yield credit spreads were just 20 basis points higher at 5.0% but were volatile throughout the month, tightening to as low as 4.2% before widening once again. The Bloomberg U.S. Corporate High Yield Bond Index fell 2.3% as a result. Bank loans were one of the few asset classes in positive territory for the month, gaining 1.5% as their floating-rate structure acts as a hedge in rising rate environments.

Given the geopolitical and inflation backdrop, we still believe it is premature to signal the all-clear and aggressively deploy capital into risky assets—especially as each rate hike increases the hurdle rate for all investments and makes lower risk substitutes more attractive

Looking Forward

The year has been dogged by central banks’ erroneous belief—a failed gambit in chess parlance that inflation was transitory, and the pain of this miscalculation has since been further exacerbated by a series of geopolitical shocks. For the first six months of the year, the growing awareness of stubbornly high inflation drove almost all asset prices lower. After some of the worst investor sentiment readings in decades, hopes for a Fed pivot propelled a powerful rally in mid-June that saw the S&P 500, which was down 24% at its low, retrace more than half of that decline, an unusually large number. This rally eased credit spreads and brightened financial conditions, pulling inflation expectations higher with it—the opposite of the Fed’s desired outcome. In response, Fed Chairman Powell delivered a blunt confirmation at Jackson Hole that the priority would be to slow demand in order to curtail inflation, even if that resulted in economic pain. Markets initially declined rapidly on these comments, but as of September 12 have rebounded modestly. Given the current landscape, we believe that, if inflation does not ease rapidly, it will be challenging for the Fed to prevent a recession.

As complex as the investing backdrop is in the U.S., it is far trickier abroad. Other economies are fighting similar challenges as the U.S., but without the luxury of energy or food security. In Europe, exorbitant energy prices are weighing heavily on economic activity, and there is considerable concern about what will transpire if the war is not resolved before the winter.

Performance Disclosures

All market pricing and performance data from Bloomberg, unless otherwise cited. Asset class and sector performance are gross of fees unless otherwise indicated.

Citations

Share it :

Disclaimer

Magnus Financial Group LLC (“Magnus”) did not produce and bears no responsibility for any part of this report whatsoever, including but not limited to any microeconomic views, inaccuracies or any errors or omissions. Research and data used in the presentation have come from third-party sources that Magnus has not independently verified presentation and the opinions expressed are not by Magnus or its employees and are current only as of the time made and are subject to change without notice.

This report may include estimates, projections or other forward-looking statements, however, due to numerous factors, actual events may differ substantially from those presented. The graphs and tables making up this report have been based on unaudited, third-party data and performance information provided to us by one or more commercial databases. Except for the historical information contained in this report, certain matters are forward looking statements or projections that are dependent upon risks and uncertainties, including but not limited to factors and considerations such as general market volatility, global economic risk, geopolitical risk, currency risk and other country-specific factors, fiscal and monetary policy, the level of interest rates, security-specific risks, and historical market segment or sector performance relationships as they relate to the business and economic cycle.

Additionally, please be aware that past performance is not a guide to the future performance of any manager or strategy, and that the performance results and historical information provided displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Therefore, it should not be inferred that these results are indicative of the future performance of any strategy, index, fund, manager or group of managers. Index benchmarks contained in this report are provided so that performance can be compared with the performance of well-known and widely recognized indices. Index results assume the re-investment of all dividends and interest and do not reflect any management fees, transaction costs or expenses.

The information provided is not intended to be, and should not be construed as, investment, legal or tax advice nor should such information contained herein be construed as a recommendation or advice to purchase or sell any security, investment, or portfolio allocation. An investor should consult with their financial advisor to determine the appropriate investment strategies and investment vehicles. Investment decisions should be made based on the investor’s specific financial needs and objectives, goals, time horizon and risk tolerance. This presentation makes no implied or express recommendations concerning the way any client’s accounts should or would be handled, as appropriate investment decisions depend upon the client’s specific investment objectives.

Investment advisory services offered through Magnus; securities offered through third party custodial relationships. More information about Magnus can be found on its Form ADV at www.adviserinfo.sec.gov.

Terms of Use

Definitions

Asset class performance was measured using the following benchmarks: U.S. Large Cap Stocks: S&P 500 TR Index; U.S. Small & Micro Cap: Russell 2000 TR Index; Intl Dev Large Cap Stocks: MSCI EAFE GR Index; Emerging & Frontier Market Stocks: MSCI Emerging Markets GR Index; U.S. Intermediate-Term Muni Bonds: Bloomberg Barclays 1-10 (1-12 Yr) Muni Bond TR Index; U.S. Intermediate-Term Bonds: Bloomberg Barclays U.S. Aggregate Bond TR Index; U.S. High Yield Bonds: Bloomberg Barclays U.S. Corporate High Yield TR Index; U.S. Bank Loans: S&P/LSTA U.S. Leveraged Loan Index; Intl Developed Bonds: Bloomberg Barclays Global Aggregate ex-U.S. Index; Emerging & Frontier Market Bonds: JPMorgan EMBI Global Diversified TR Index; U.S. REITs: MSCI U.S. REIT GR Index, Ex U.S. Real Estate Securities: S&P Global Ex-U.S. Property TR Index; Commodity Futures: Bloomberg Commodity TR Index; Midstream Energy: Alerian MLP TR Index; Gold: LBMA Gold Price, U.S. 60/40: 60% S&P 500 TR Index; 40% Bloomberg Barclays U.S. Aggregate Bond TR Index; Global 60/40: 60% MSCI ACWI GR Index; 40% Bloomberg Barclays Global Aggregate Bond TR Index.